Editor’s Note: Within the next two weeks, you’ll begin receiving your regular Wide Moat Daily e-mails from:

widemoatresearch@mail.beehiiv.com

widemoatdaily@mail.widemoatresearch.com

You can view instructions on how to whitelist those addresses by clicking here.

I built for a number of retail chains back when I was a commercial real estate (CRE) developer. And being very selective about who I worked with, most of those contracts worked out well for me.

But some, like Sally Beauty Holdings (SBH), were absolute gems I’ll always appreciate.

That was the definite case with Sally. Sweet but simple, it paid its rent on time, brought traffic into any shopping center I put it in, and never gave me headaches as a landlord.

Sally Beauty was such a great tenant, in fact, that it taught me a valuable lesson: Sometimes the most attractive businesses aren’t the flashiest ones.

They’re companies with loyal customers, disciplined capital allocation, and strong margins.

All these years later, Sally still stands out as an attractive investment – especially considering where it’s trading at today. The same applies to Ulta Beauty (ULTA), a store you no doubt know of… but probably never considered investing in.

{kind=link}

There’s real appeal in these businesses once you get to know them though. I’d even say their financial figures are outright lovely to look at.

Sally Beauty Holdings on full display

Sally Beauty Holdings was founded in New Orleans in 1964 as part of Alberto-Culver. Its purpose: to distribute professional-grade beauty products.

While it built quite the reputation serving salon professionals, it also did well with individual, do-it-yourself (DIY) customers. So well, in fact, that the whole kit and caboodle spun off as its own public company in 2006.

Today, it still operates through those two successful primary segments:

-

Sally Beauty Supply for retail and prosumer customers

-

Beauty Systems Group for salon professionals.

The results of that focus might not blow the market away Big Tech-style. But Sally still manages to more than hold its own. Better yet, it does so consistently.

In the company’s most recent quarter:

-

Gross margins were approximately 51%.

-

Earnings per share (EPS) grew 12% to $0.48.

-

Operating cash flow was $93 million.

Free cash flow, meanwhile, came in at $57 million – which management wisely used to pay down $20 million in debt and repurchase $21 million in stock.

With sensible leadership like that in place, it should come as no surprise that Sally Beauty’s balance sheet remains solid. The company has $157 million in cash and no borrowings under its revolver.

Now, S&P Global Ratings does give it a credit rating of “BB,” which is below investment grade. But it’s also firmly within the upper tier of high-yield assessments.

This suggests that while Sally does carry leverage, it still remains financially stable with solid access to capital markets. Put that together with the level of cash flow it’s generating and how it’s actively deleveraging, and I firmly believe its rating can improve from here.

That upside can then quietly build in shareholders’ favor… even in the face of competition like Ulta Beauty.

Ulta Beauty: A Best-in-Class Retailer

Ulta Beauty was founded in 1990, much later than Sally. But Richard E. George, a former Osco drug executive, saw an opportunity to reinvent the beauty shopping experience.

So he did.

Back then, beauty retail was fairly fragmented. Department stores sold prestige cosmetics. Drugstores sold mass products. And salons operated on their own.

Customers would therefore have to go to three different places for three similar sorts of products… until Ulta put everything under one roof.

This one-stop beauty shop company went public in 2007 and steadily expanded across the U.S. It benefits from a highly scalable big-box format that’s still working well today with its exceptionally loyal ecosystem.

Over the years, Ulta began implementing a rewards program that now drives the vast majority of sales. This also gives it unmatched insights into customer behavior.

All told, it’s safe to say George didn’t just add to the beauty category; he redefined it altogether.

The company continues to invest heavily in innovation, including through its digital capabilities, loyalty program, supply chain, and brand selection. Those moves are literally paying off, and the stock has responded accordingly, recognizing that Ulta isn’t just a retailer.

It’s a platform – one I’m not convinced has hit its full potential just yet.

For instance, Ulta is doing too good a job navigating the “masstige” category, which puts premium products at more affordable prices for the masses. Plus, its (more than) 46 million loyalty program members produce about 95% of its sales, creating quite the powerful moat.

The beautiful wide-moat takeaway

Beauty is a resilient category because it’s built on repetition. Consumers don’t buy products in this category just once.

They find a brand they like, and they keep coming back for more.

This gives Ulta Beauty investable amounts of scale and brand power, and Sally Beauty attractive margins and cash flow. And I’m a personal fan of both combinations.

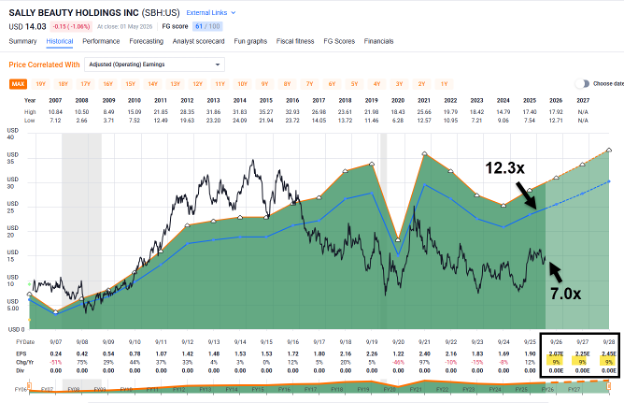

As shown below, Sally’s earnings fell significantly during the Covid era from $2.26 per share to $1.22. But it’s finally on track to hit its former glory by year-end 2027.

{kind=link}

Source: FAST Graphs

Analysts expect 9% growth this year, 2027, and 2028. That’s quite the nice amount that should show up in its share price as time goes on.

SBH is currently trading at 7x… well below its normal multiple of 12.3x. And while I’m not betting on it hitting that high again any time soon, 9x sounds more than reasonable.

If that happens, SBH could generate outside returns of about 30%.

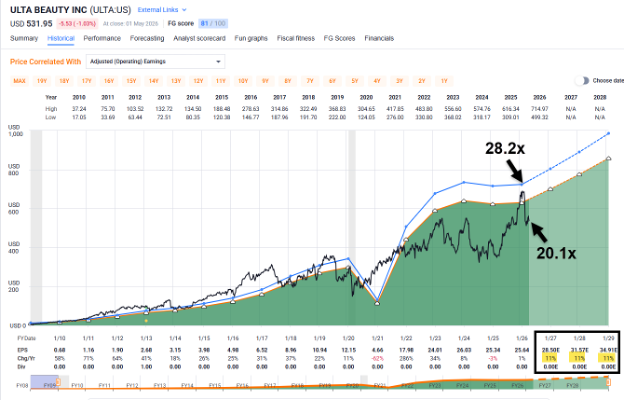

Ulta, for its part, did see earnings take a modest dip last year. But EPS should grow more than 10% in fiscal-year 2026. And it’s trading at 20.1x versus its normal 28.2x – opening up a nice little bargain possibility.

Shares went as high as 23x back in December; and if they can just climb back, we’d be looking at annual returns of 30%. Or higher.

{kind=link}

Source: FAST Graphs

Neither of these beauty brands pay dividends, unlike Wide Moat Research’s normal recommendations. However, I think they’re worth considering anyway.

Their consistent demand, quiet though it may be, is too compelling to ignore. Regardless of what you may think of their overall unnecessary products, both Sally and Ulta have the kind of “inner beauty” strong portfolios are made of.

Regards,

Brad Thomas

Editor, The Wide Moat Daily

|