Editor’s Note: After two decades managing hundreds of millions for Wall Street legends like Steve Cohen, Leon Cooperman, and David Einhorn, Gabe Marshank is stepping forward to reveal how he finds the kinds of stocks that can soar 5 times… 10 times… even 25 times or more.

On Wednesday, he is putting his ideas to the ultimate test in a live, unscripted “Shark Tank” style showdown with some of the most respected investors in our industry.

The event is completely free to attend. And when you tune in, Gabe will also share his new favorite idea – a breakthrough play in quantum computing. Get all the details for yourself right here.

It’s the time of the year when we purposefully try to scare ourselves – haunted houses, horror movies, scary costumes.

But please promise me you’ll keep those scares out of your investment pursuits…

I understand the rush that can come from buying risky stocks with high-reward appeal. If they pan out, you just cheated financial “death” – not to mention how you’re richer as a result.

The key word being “if.”

But they usually don’t pan out. If an investment opportunity looks like a sucker’s play and walks like a sucker’s play… then chances are, you’re the sucker.

Last week, I wrote “Trick or Treat, My Favorite REITs,” and profiled a few of my favorite real estate investment trusts (“REITs”) on the market today. If those investments were the “treats,” the three REITs below are the “tricks.”

My advice: Make sure they don’t end up in your portfolio.

Spooky REIT No. 1

Sachem Capital (SACH) is a small-cap commercial mortgage REIT with a market cap of $52 million. It originates, services, and manages a portfolio of short-term first-mortgage loans.

And it boasts an 18.1% dividend yield, which is far too high.

The REIT has $556 million in total assets, including 226 loans in 15 states, with an average portfolio yield of 13%. Almost 60% of those loans are considered residential, 28% are commercial, 6.1% are allocated to land, and another 6.6% to mixed-use properties.

As of the second quarter of 2025, Sachem had about a $119.6 million gross unpaid principal balance of nonperforming loans. That’s up from $107.6 million in the first quarter of this year.

It also had enhanced exposure to one customer in South Florida that’s going through bankruptcy. We’re talking about $50.4 million, or 13.1% of its loan portfolio.

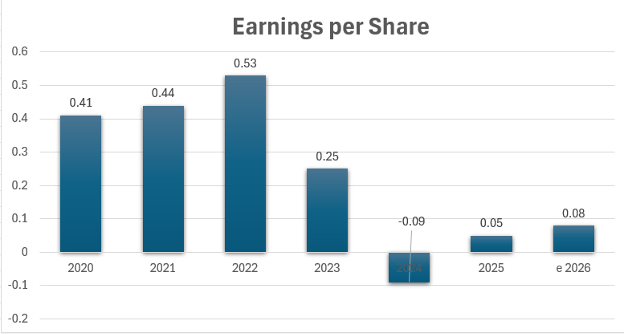

As seen below, Sachem has been struggling for a while now as its earnings per share (“EPS”) have deteriorated since 2023. In the second quarter, it even generated net income of just $0.8 million, or $0.02 per share.

{kind=link}

Source: Wide Moat Research

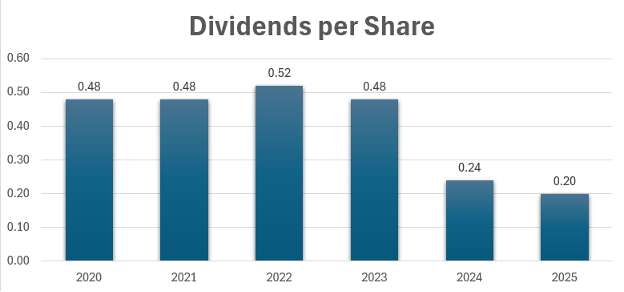

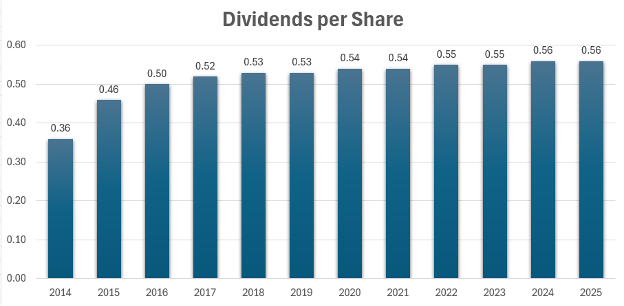

It should come as no surprise, then, that Sachem was forced to cut its dividend both this year and last.

{kind=link}

Source: Wide Moat Research

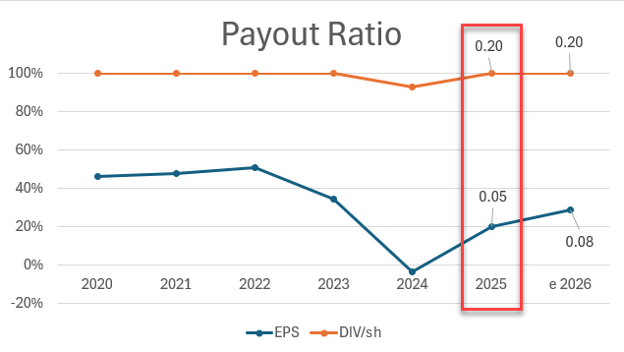

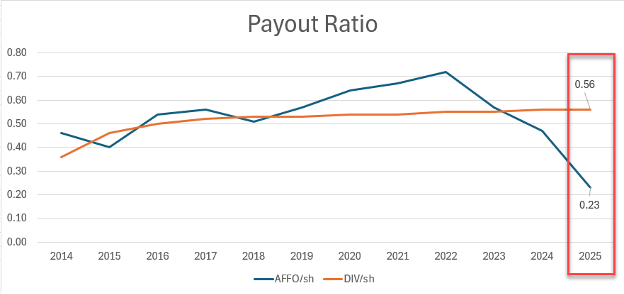

In fact, the company has never been able to cover its dividend very well. As seen below, its current $0.20 per share payout isn’t sustainable. And I suspect it will have to cut it again soon enough.

{kind=link}

Source: Wide Moat Research

Spooky REIT No. 2

Gladstone Land (LAND) is a farming REIT that owns 150 farms with approximately 103,000 total acres in 15 states. It also holds more than 55,000 acre-feet of water assets in California.

The company is primarily focused on specialty crops, including fruits, vegetables, and nuts, which sounds like a good business premise. I like the farming-REIT idea in general and have even recommended Gladstone Land in the past.

However, I’ve always noted how it’s externally managed by the Gladstone Companies, an SEC-registered investment adviser with more than $4 billion of assets under management and more than 70 professionals. That kind of power structure can be problematic all by itself…

And it doesn’t help that President Donald Trump’s tariffs have negatively affected commodity produce. As a result, Gladstone has modified a number of its leases from flat rents to participation rents.

CEO David Gladstone recently explained that the REIT has “moved from being a leaser and more of an operator or a grower of sorts because we’re taking some of our payment for the lease in part of the crop that is being grown.”

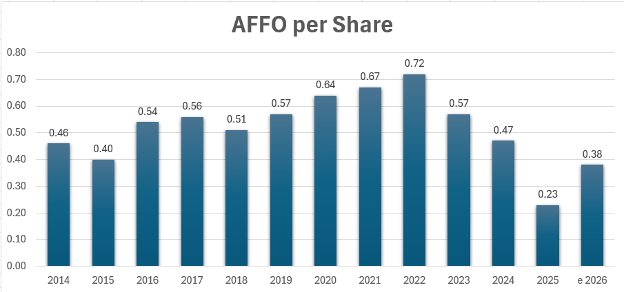

In the second quarter of 2025, the company recorded a net loss of about $7.9 million and a net loss to common shareholders of $13.9 million, or $0.38 per share. Adjusted funds from operations (“AFFO”), meanwhile, was at negative $3.4 million, or negative $0.10 per share, compared with a positive $3.7 million, or $0.10 per share, in the second quarter of 2024.

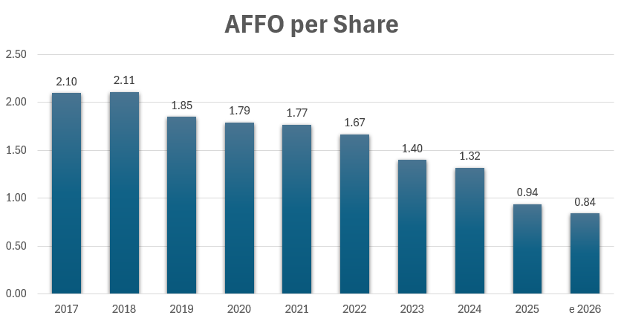

As you can see, AFFO per share has fallen from an all-time high of $0.72 in 2022 to $0.23 in 2025.

{kind=link}

Source: Wide Moat Research

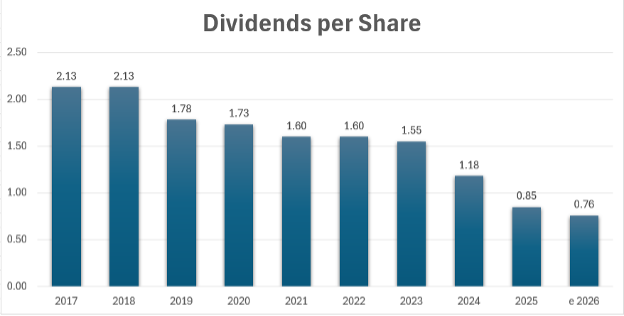

Given this earnings decline, it seems likely that Gladstone Land will be forced to cut its dividend… even though that hasn’t happened since 2013.

{kind=link}

Source: Wide Moat Research

Here’s a snapshot of the company’s payout ratio in case you’re not convinced:

{kind=link}

Source: Wide Moat Research

Spooky REIT No. 3

Global Net Lease (GNL), a net-lease REIT, owns 911 properties with a gross asset value of around $7 billion.

Its 44-million-square-foot portfolio is diversified with 200 industrial properties, 647 retail properties, and 64 single-tenant office properties. These are 98% leased with a weighted-average lease term of 6.2 years.

On the surface, GNL, with its 9.9% dividend yield, appears to be stable. Its broad customer and market diversification seems to give it the kind of stable revenue sources that net-lease investors enjoy.

However, earnings in the form of AFFO per share have declined since its IPO in 2015.

{kind=link}

Source: Wide Moat Research

It has also been a chronic dividend-cutter ever since:

{kind=link}

Source: Wide Moat Research

That’s not what I would call a “sleep well at night” REIT.

Global Net Lease’s payout ratio sits at an elevated 90%, leaving it on our dividend watch list.

{kind=link}

Source: Wide Moat Research

Who knows? Maybe it can escape having to slash its dividend. But that’s not a chance I want to take.

I’d much rather get my thrills somewhere else that doesn’t put my profits at risk.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Check out the Wide Moat Show on YouTube this week, where I will be discussing “Trick or Treat, My Three Favorite REITs.”

|