Quantity has a quality all its own…

That line is (dubiously) attributed to Joseph Stalin, who is supposed to have said it during years of war on the Eastern front. During the Second World War, Russia may not have had robust manufacturing infrastructure. But it did have another asset – soldiers, lots of them. That turned out to be enough.

In business, we’d know this idea as “scale.” Sometimes, just being the largest dog on the block affords certain advantages. And it’s one of the of several wide moat advantages we look for in the companies we recommend.

Scale often means bargaining power with suppliers and distributors, just ask Coca-Cola (KO). The company’s scale is so large that it can basically dictate terms to distributors. And the distributors have no choice but to accept it.

Scale also means access to capital and at better rates. A company like Apple (AAPL) might be an example of this. Browsing the AAPL corporate bonds this morning, I found one issued in May of this year, set to mature in 2035, carrying a coupon of 4.75%. At the time of issuance, the U.S. 10-Year Treasury yielded about 4.5%. In other words, the market believes Apple is nearly as credit worthy as the U.S. government. Some might even argue it’s more so.

And for real estate investment trusts (“REITs”), scale means diversified, and more reliable, rental income. It also means a lower cost of capital, which allows the business to endure even through challenging environments (more on that below).

But size isn’t a guarantee of success. I learned that the hard way.

In an August article, I detailed "How I Lost $1 Million in the Pizza Business.”

Despite having no business experience in the food industry, I envied my friends who were franchisees. And so, I ended up opening a Papa John’s (PZZA) location in one of the shopping centers I owned.

I then quickly opened another. And another. In no time at all, I had eight, a number that left me “overwhelmed by the challenges of hiring – and training – managers. Dealing with ingredient logistics while controlling costs was another headache. And dealing with the (mostly teenage) employees was a nightmare.”

Scale can be an incredible advantage. It just depends on who’s managing the assets.

And there’s one more thing to consider…

The “Bigger Is Always Better” Mantra Leads to Bubbles

As I explained in yesterday’s article, the artificial intelligence ("AI") situation is looking like a bubble more and more. I quoted Fortune 500 Digest as noting how:

AI startups are under a lot of pressure to prove they can scale quickly. That’s because some truly have grown at an unprecedented rate, thanks to market conditions that VC firm Andreessen Horowitz has dubbed “the great expansion.”

The hottest startup metric for flaunting fast growth is ARR (annual recurring revenue). But some founders are getting creative about how they’re accounting for ARR as they attempt to raise new rounds of financing.

One VC told Fortune‘s Allie Garfinkle that what he’s seeing more closely resembles “vibe revenue” than truly recurring deals.

Nor is it just startups that are getting greedy. The Wall Street Journal wrote recently that it’s “time to stress-test everything,” including Big Tech companies.

“Oracle announced a $300 billion deal for data centers with OpenAI – money it doesn’t have,” it points out. “This was followed by Nvidia’s $100 billion investment… in Open AI,” despite only having $56 billion in cash on hand.

The big news yesterday was that Advanced Micro Devices (AMD) is now joining the deal-making spree. The rival to Nvidia (NVDA) inked a deal with OpenAI, the company behind ChatGPT. AMD will sell about $78 billion worth of chips to OpenAI over several years. For its part, OpenAI received warrants that will vest over several years contingent upon certain milestones. If fully vested, the warrants would equate to about 160 million shares, or approximately 10% of AMD.

The AI ecosystem is big… and it’s only getting bigger.

I don’t have a crystal ball. Nobody knows where those efforts will end up. But I can tell you where similar expansionary efforts have.

Take General Electric (GE), once the world’s largest company. It was so focused on getting bigger that it forgot everything else. The result is that a company mostly known for lightbulbs, home appliances, and jet engines had business segments for financing, oil and gas, and health care.

But GE was eventually forced to admit that its ambition for more scale had outpaced its ability to manage these assets. It went through a years-long period of spin-offs and divestitures.

The result was that this once-massive business now exists as three separate public companies.

That’s what happens when management prioritizes growth above all else.

Everything falls apart.

It might take years for the inevitable to happen. It might even take decades, as was the case with GE. But it’s going to happen eventually.

Two REITs That Do Scale the Right Way and Wrong Way

Years ago, I learned how to evaluate intelligent investments from my good friend Chuck Carnavelle. (See our YouTube episode with Chuck as our guest here.) He told me that during the telecom, automobile, and computer price wars of the past, individual company’s profit margins predicted how they would fare.

While scale advantage can certainly be part of a “wide moat” blueprint, it’s not the most essential ingredient. As Chuck taught me, corporate profits matter more.

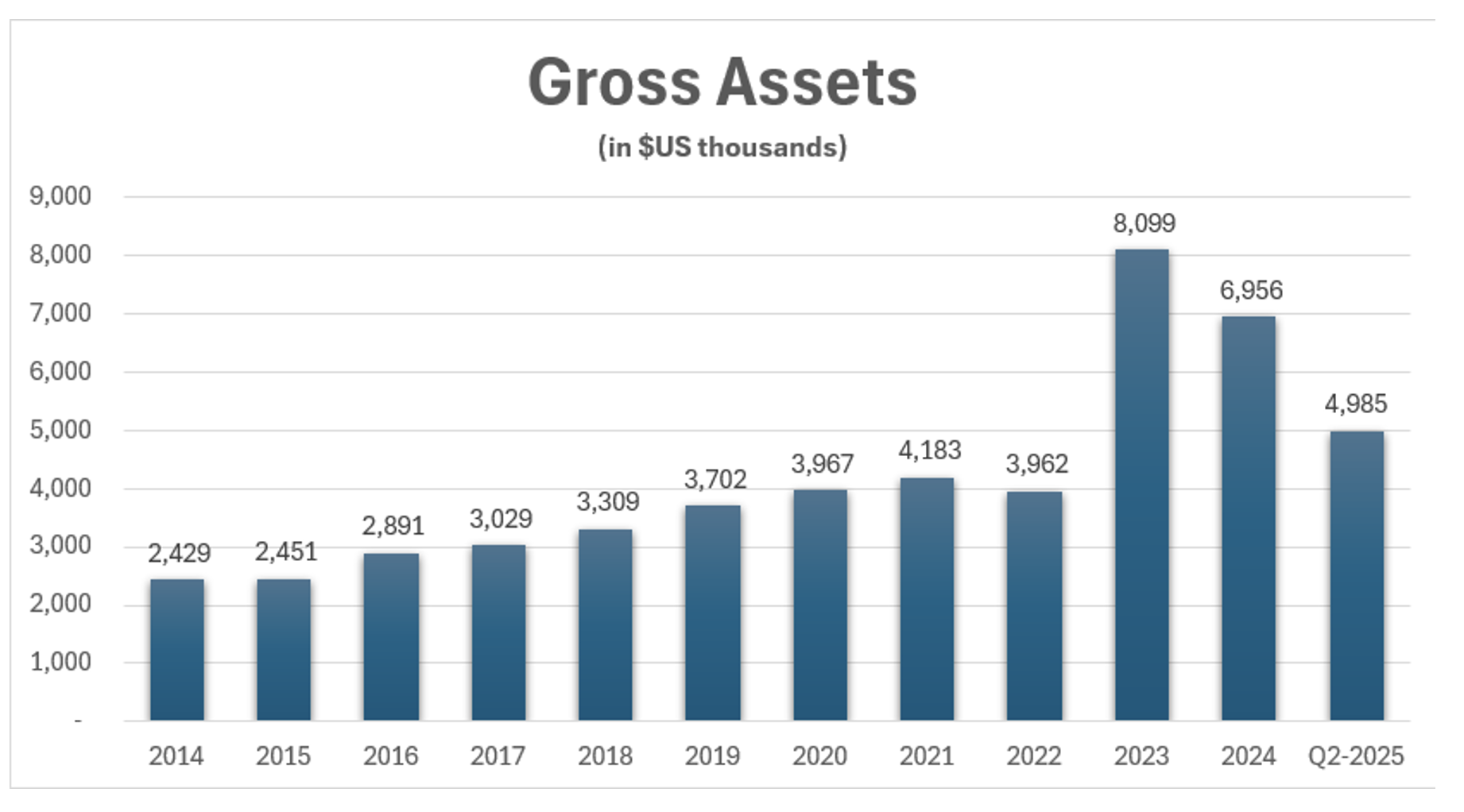

Consider Global Net Lease (GNL), a net-lease REIT that we follow. As shown below, it grew its assets by an impressive 17% compound annual growth rate (“CAGR”) from 2014 to 2023.

{kind=link}

Source: Wide Moat Research

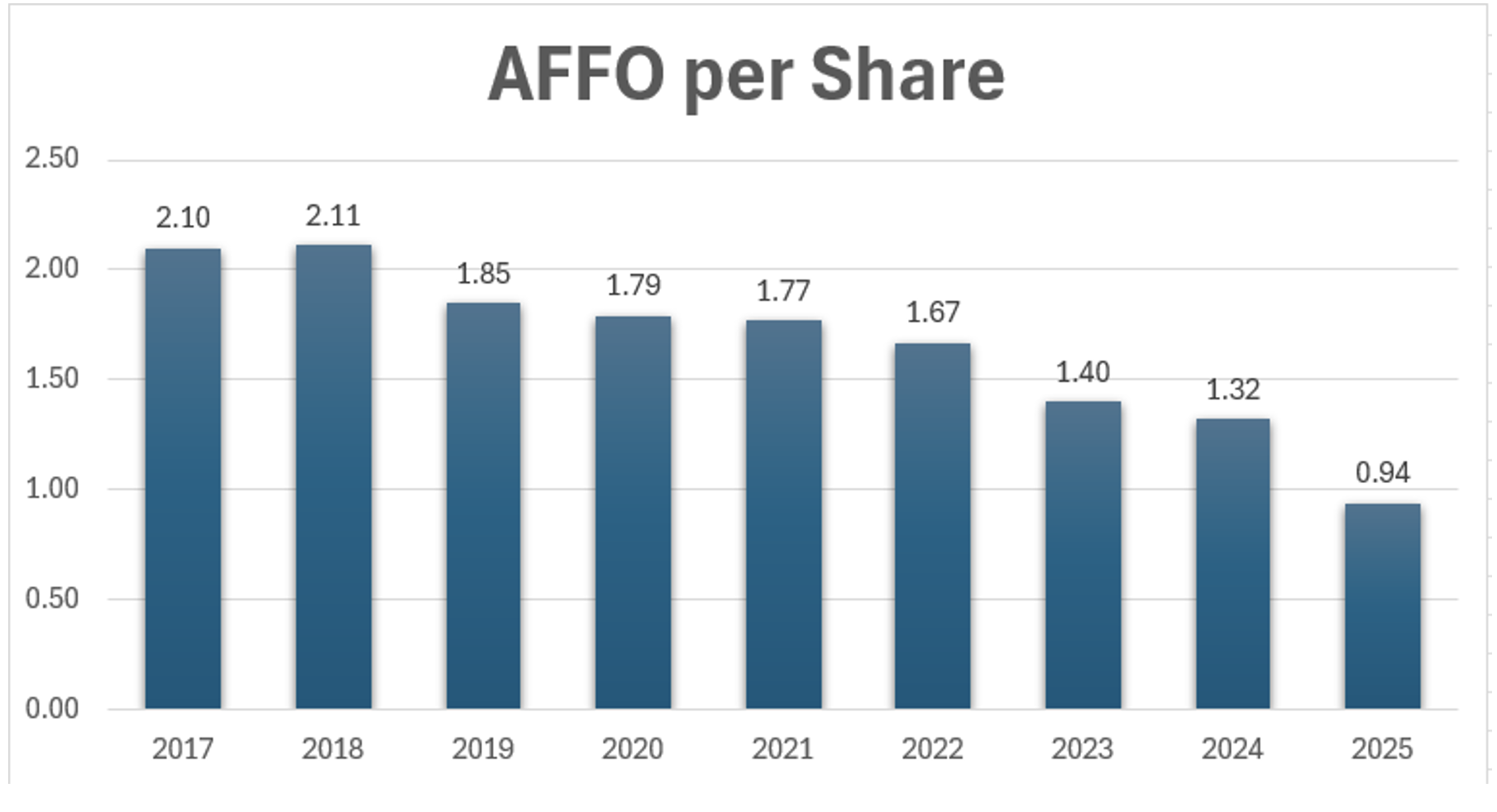

However, that’s not the whole story, as evidenced by its earnings, or adjusted funds from operates (“AFFO”), per share:

{kind=link}

Source: Wide Moat Research

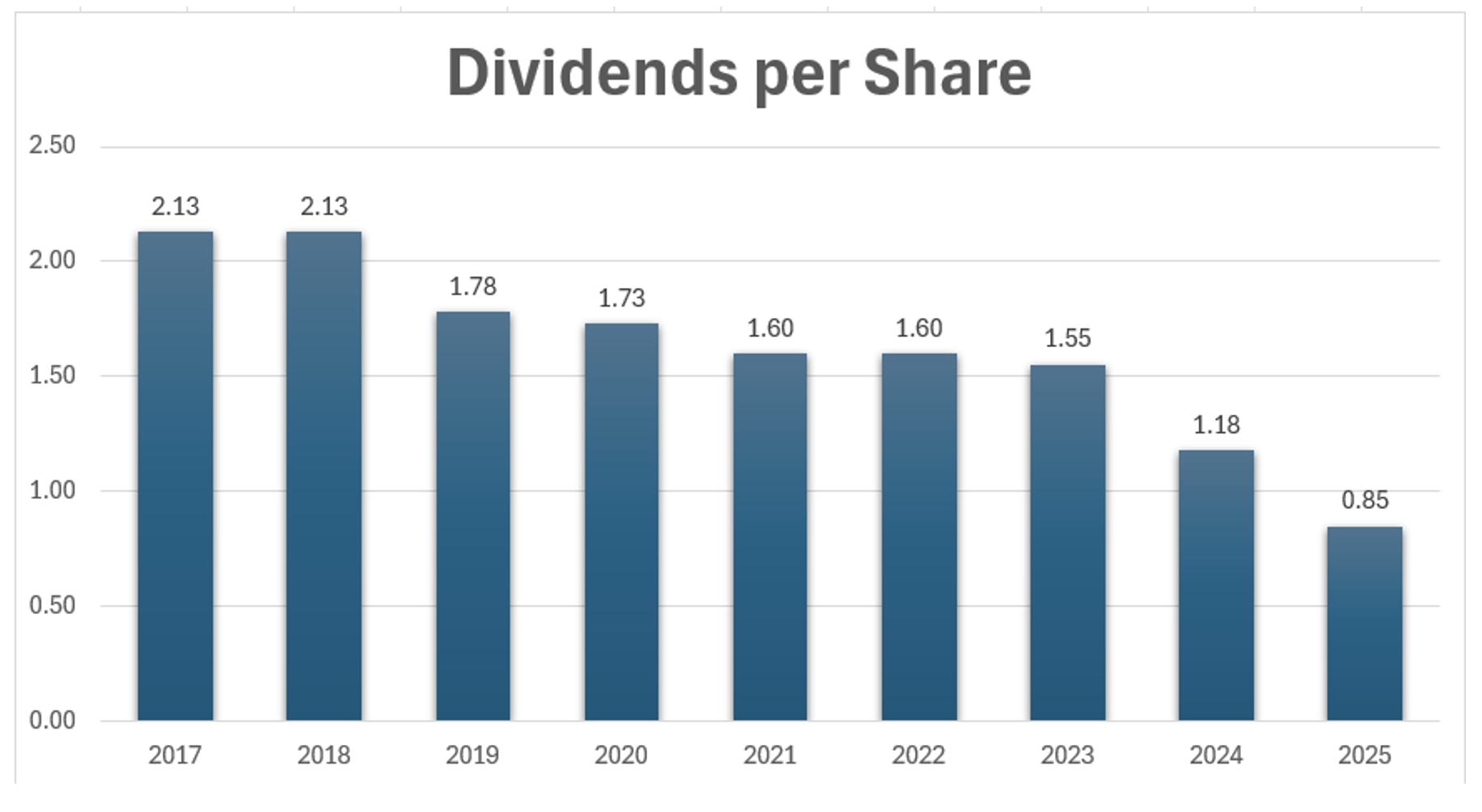

This is what I call a value destroyer, which is why GNL is such a chronic dividend cutter.

{kind=link}

Source: Wide Moat Research

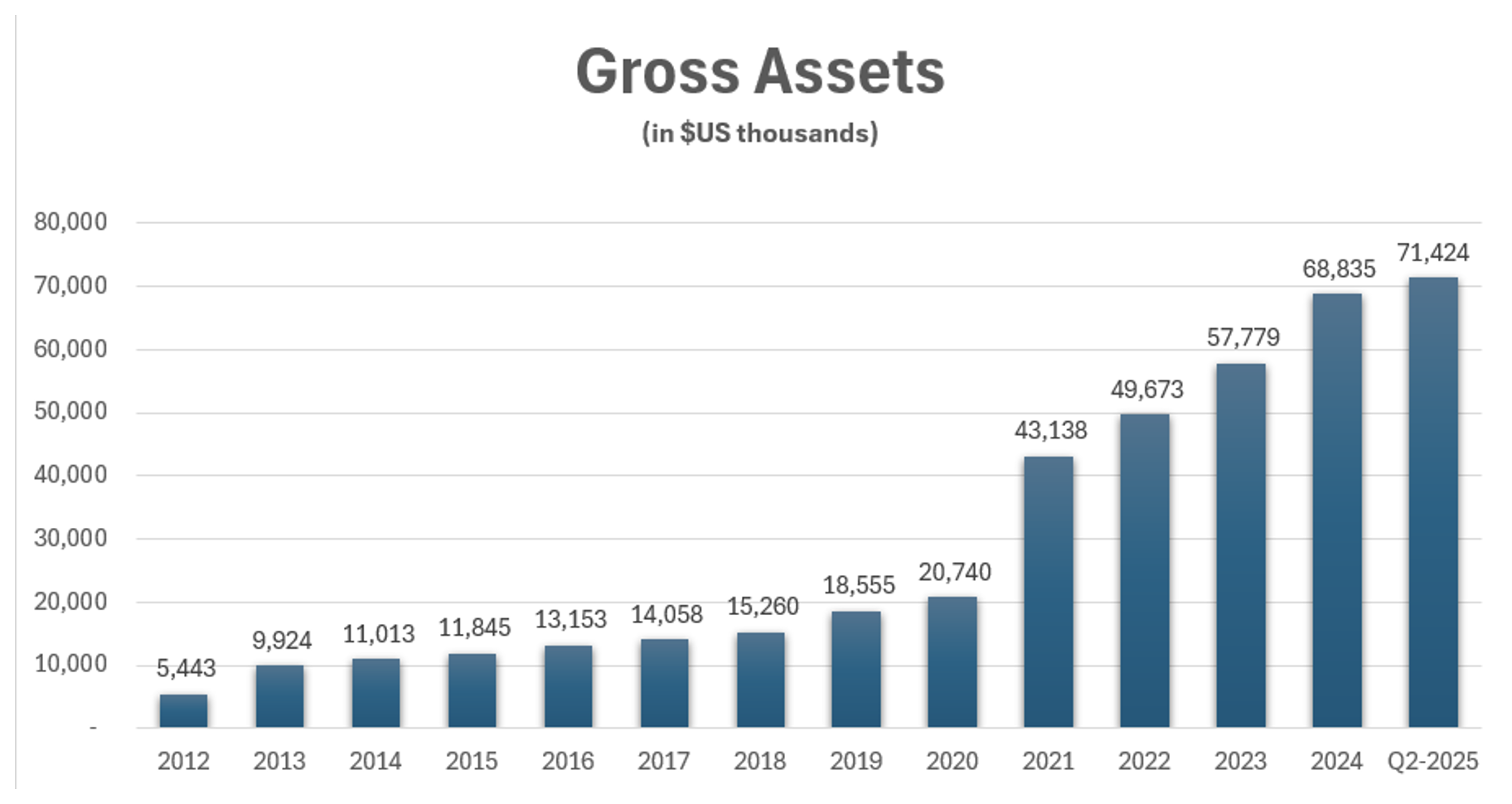

If you want a textbook example of scale done right, look no further at GNL’s bigger (and better) net-lease competitor, Realty Income (O). Here’s a snapshot of its gross assets:

{kind=link}

Source: Wide Moat Research

As you can see, Realty Income has grown its assets every year. It has even used the post-COVID era to buy up two competitors, Vereit and Spirit Realty.

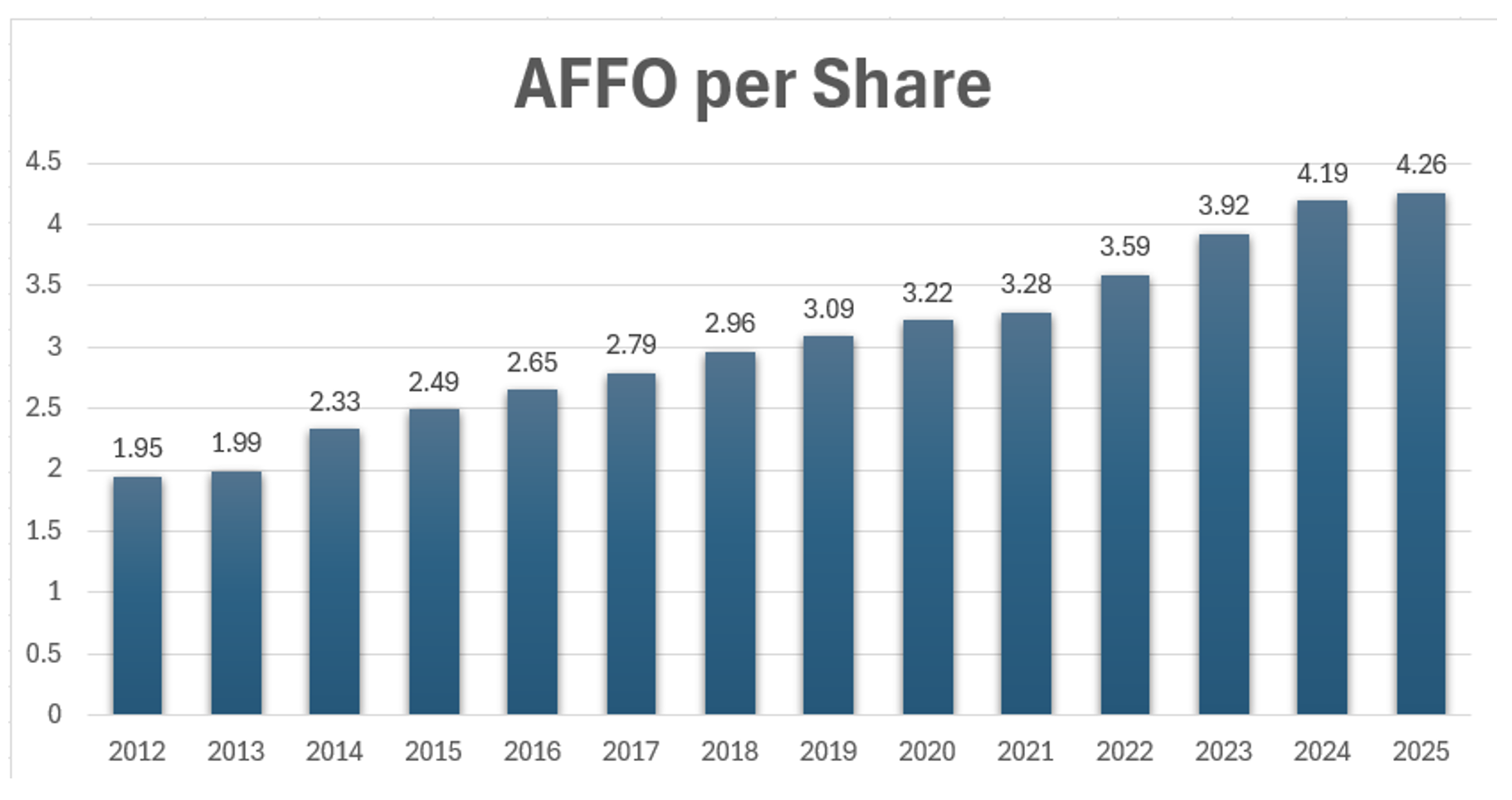

As a result, its CAGR since 2012 has been an impressive 25%. Better yet, it’s generated positive AFFO per share growth in every year, even during the shutdowns when its gym and theater tenants couldn’t operate.

{kind=link}

Source: Wide Moat Research

That’s why it continues to grow its dividend every single year, decade after decade.

{kind=link}

Source: Realty Income

That’s the true mark of scale done right. When it’s smart and sustainable – when growth plans are built on both intelligence and integrity – it’s worth investing in.

That’s when bigger is better.

Happy SWAN (sleep well at night) investing!

Regards,

Brad Thomas

Editor, Wide Moat Daily

|