Imagine you lead BlackRock (BLK), a Wall Street titan with $11.5 trillion in assets under management. Dictators of average-sized countries envy you. Nothing is out of your reach. Every legal, banking, and research capability is at your fingertips. You are on top of the world.

As CEO, you personally led the $12 billion acquisition of HPS Investment Partners that closed in July. This deal cemented BlackRock as a top player in private credit – Wall Street’s fastest growing cash cow – and your legacy.

But your untouchable firm is about to learn a very expensive lesson: There is no substitute for old-fashioned due diligence.

In today’s edition of the Wide Moat Daily, I’ll explain how BlackRock, the world’s largest asset manager, was just shocked by a $500 million loss and a sobering hit to something much more valuable – their reputation.

But to make sense of what just happened to BlackRock, we need to take a step back and understand the private credit markets and how BLK fits within the ecosystem.

Wall Street’s Darling

Whether through publicly traded business development companies (“BDCs”) or popular private credit investments offered by the likes of Blackstone (BX), KKR (KKR), and Apollo Global Management (APO), an increasing number of investors depend on the private credit sector for income.

It’s easy to see why. Many of the largest BDCs currently offer 9% to 11% dividend yields and not only maintained, but increased distributions during COVID-19. That compares with nearly 200 listed U.S. stocks that cut dividends in 2020, including Boeing (BA) and Walt Disney (DIS).

Most private credit investments, including BDCs, generated attractive yields when interest rates were low, and they did the same more recently when they were much higher.

So, what’s the issue? And how did BlackRock find itself on the wrong end of a $500 million tab?

To start, let’s get a good grasp on what private credit is and why it’s so critical to our modern economy. I’ll set the stage with two charts you shouldn’t forget.

{kind=link}

Source: Statista

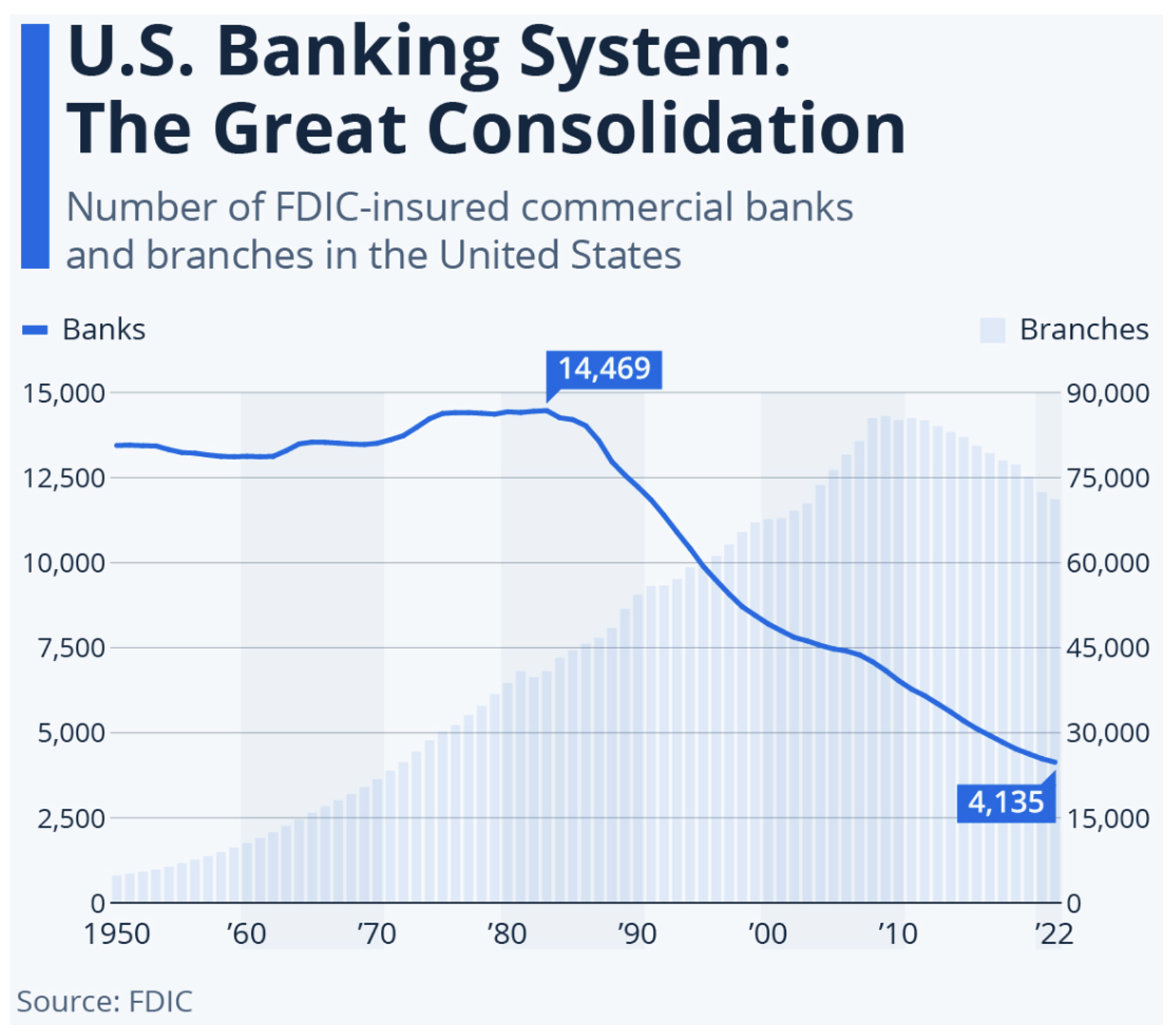

The banking crises of the 1980s, 1990s, and eventually 2008/2009 put downward pressure on the number of banks in the U.S. Increased regulatory and compliance costs also encouraged bank mergers.

The result is a nearly 70% decline in the number of U.S. banks since the 1980s. For context, over that same period the U.S. economy has grown from $2.2 trillion in 1985 to $29.2 trillion last year, or a more than 1,200% increase.

Not only that, but the Dodd Frank Act of 2011 severely punished big banks, making it nearly impossible to loan to small businesses or private companies of any size. Yet, it’s exactly those small and non-listed companies generating most of the economic growth and hiring. If the banks are shrinking in number and running away from the most robust part of the U.S. economy, who is filling the gap?

{kind=link}

Source: BNY

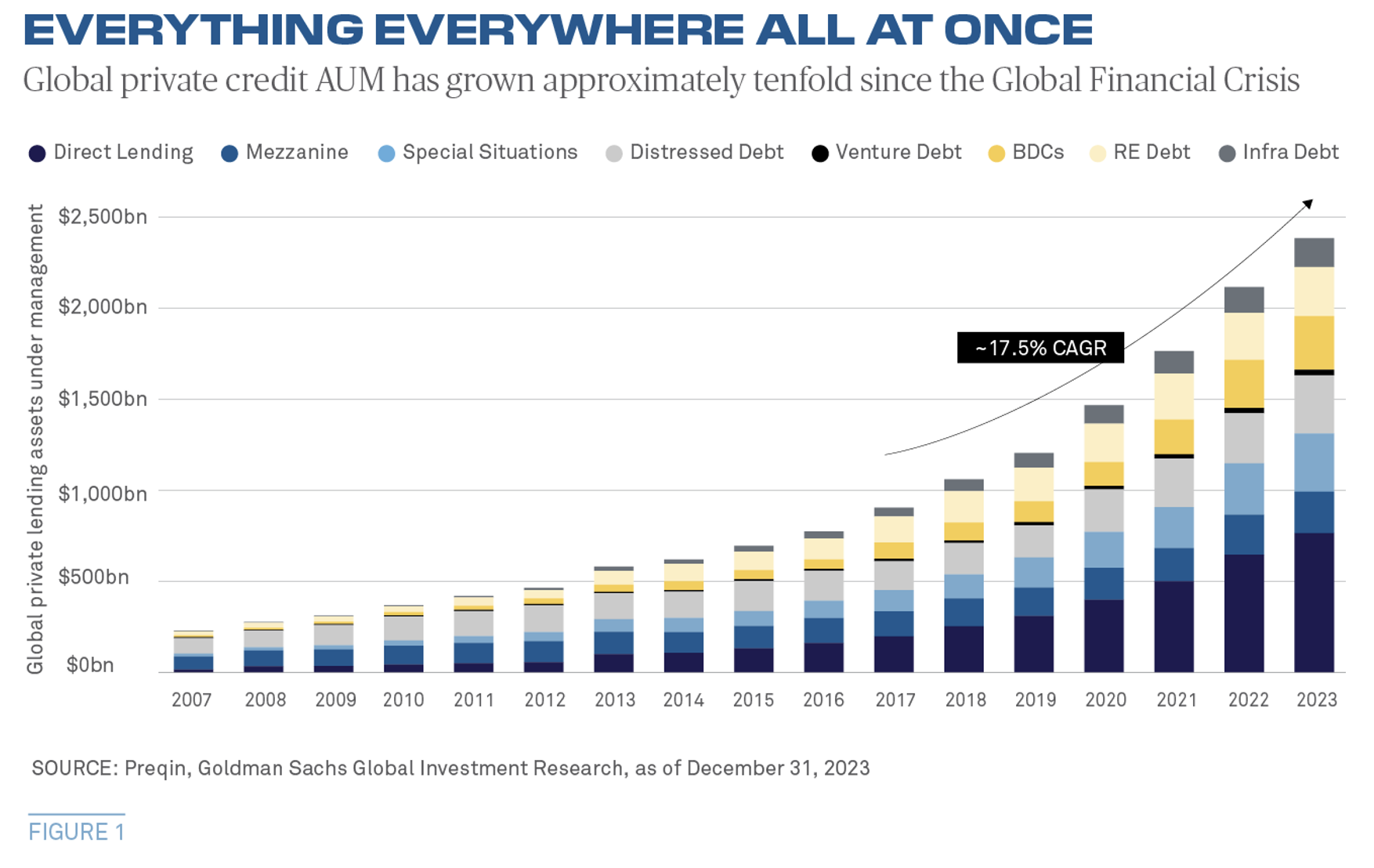

Private credit is. The above chart shows the incredible story of private credit growing from a rounding error 20 years ago to about $2.5 trillion in assets today. This is the engine powering millions of businesses all over the country.

And generally speaking, it has worked out great for investors, as the yields mentioned above show.

But success comes with a cost. One BlackRock just learned the hard way.

The Cockroach Rule

Jamie Diamond, CEO of JPMorgan Chase (JPM), recently issued a warning about the industry: “When you see one cockroach, there are probably more.” As a veteran of private credit due diligence, I can tell you Dimon is right.

As an institutional due diligence officer leading teams at some of the largest broker/dealers in the country, I analyzed many of the private credit funds that are now the giants of the industry.

What separates the good from the great was what we call their underwriting. That’s the legwork of making phone calls, scrutinizing volumes of financial documents, double-checking customer agreements, and structuring the loan so that "heads you win, tails you break even." That’s the genius of private credit in a nutshell. It was my job to make sure the private credit manager was doing theirs.

And that’s where BlackRock failed.

My best guess is BlackRock’s acquisition team saw HPS’s $148 billion private credit platform and took for granted that they were still doing the old-school due diligence necessary for success. They weren’t, at least not all the time.

Starting in the third quarter 2020, HPS began lending to one company owned by Bankin Brahmbhatt, an India-born, U.S.-based telecom entrepreneur. These weren’t small loans. By August 2024, the balance was $430 million.

HPS likely felt good about it for two reasons. First, BNP Paribas SA also loaned to Brahmbhatt’s telecom group. They must have double-checked things, right? And more importantly, the loans were secured by contracts with huge telecommunications companies. At least, that’s what they thought.

Two years of e-mail correspondence, all the contracts, and financials provided by Brahmbhatt to support the contracts were fake. And what real money existed was quietly transferred offshore back to India.

It was fraud, pure and simple.

Here’s the crazy part: HPS (and subsequently BlackRock) could have avoided being defrauded out of $500 million very easily.

Make a phone call!

Not a single person at HPS ever bothered to call the clients to verify they had a relationship with Brahmbhatt’s companies. This signals layers of missteps by HPS. All private credit managers must verify collateral using third parties. There should also be continual monitoring and verification of the key parts of the business. Multiple teams at HPS didn’t do their job, and odds are it wasn’t isolated, hence the “cockroach rule.”

Is the Sky Falling or Is This an Isolated Incident?

With HPS and BlackRock in the news, it’s tempting to panic. I’ll give you my no-nonsense take as someone who has studied and worked with many of the largest and smallest private credit shops.

Diversification is non-negotiable. Blackstone’s very popular private credit vehicle nicknamed BCRED has about 500 portfolio companies in 50 different sectors. One look at those stats and you might think a single investment in BCRED is as diversified as the S&P 500. In some ways that’s true, but in one critical way it’s not: Blackstone still originated all the loans.

If that team gets lazy or starts making the same mistakes as HPS did, you’ll regret going all-in on that one fund. But there are still tons of great options out there, so I suggest investing in several. Since there are many publicly traded options, you don’t have to worry about making large investment minimums, either.

Second, many private credit managers have long and esteemed track records that can’t be argued. Sixth Street Specialty Lending (TSLX), for example, has among the lowest loan losses in the entire industry. It’s a smaller company founded in 2009, and management has a lot of skin in the game via insider ownership.

Ares Capital Corp (ARCC) is one of the largest BDCs and has beaten the S&P 500 since its inception in 2004. It just reported strong earnings on October 28 with a record backlog in lucrative loan opportunities.

Yet both ARCC and TSLX are attractively valued because of the drama in private credit. They are also both publicly traded companies and have been for over 10 years.

History has shown that publicly traded companies tend to have better transparency and financial reporting than private companies. Those are just a couple of the reasons why I think strategic exposure to publicly traded BDCs is the best way to profit from private credit.

My Readers Already Know This

In our High-Yield Advisor service, we specialize in finding outside-the-box income opportunities with yields that often exceed 10%. BDCs are one of my favorite asset classes.

We locked in a 40.8% total return on Golub Capital BDC (GBDC), 34.2% on Ares Capital Corp (ARCC), and 37.4% on Blackstone Secured Lending (BXSL).

And as I write, some of our BDC recommendations are yielding between 11% and 17%, thanks largely to the uncertainty in this market right now.

BlackRock learned a hard lesson – no doubt. But that’s not enough to condemn the entire private credit market. There’s still plenty of reputable options for income-oriented investors.

I think we are on the precipice of another bull market in BDCs you don’t want to miss. Just be sure to know which BDCs are still doing their homework…

Regards,

Stephen Hester

Chief Analyst, Wide Moat Research

P.S. If you’re at all interested in joining us at High-Yield Advisor to learn about which BDCs we’re recommending now, the best way to do that is to contact our customer support team. Simply call or e-mail them and ask for more details on High-Yield Advisor from Wide Moat Research. Their contact information is right here.

|