On Monday, I published a critique of Warren Buffett’s decision to buy into homebuilders earlier this year. That is to say, his holding company, Berkshire Hathaway (BRK-A)(BRK-B), bought shares of Lennar (LEN) and D.R. Horton (DHI).

I respect the man and his business. I don’t know a single investor who doesn’t. But I do think he might have been a bit premature investing in the sector.

As I wrote, “Between high list prices, high mortgage prices (even if they did drop this month), and how debt-ridden consumers are… there’s not much incentive for people to buy a home these days.”

The past eight months have not been easy for homebuilders…

Of course, with all his billions, Buffett can afford to be a bit early. And after holding on to an increasing pile of cash for several years (nearly $350 billion as I write)… it does seem as if Berkshire Hathaway believes an economic upturn is on its way.

You don’t invest in homebuilders – a sector sensitive to economic cycles – otherwise. Nor do you buy into billboards, as Berkshire did last quarter – 1,169,507 shares of Lamar Advertising (LAMR), to be precise, for $142 million.

Lamar is a real estate investment trust, or REIT. And as I wrote on August 14:

These companies, which own real estate-specific assets, are legally exempt from paying corporate income taxes. In return, they pay out at least 90% of their annual taxable income to shareholders in the form of dividends.

The right REITs – and there are many of them – offer consistently rising dividend payouts and share price appreciation at the same time.

REITs fall into different subdivisions, such as residential, retail, office, lodging, industrial, and data centers. And some of those subdivisions offer more reliable rewards than others.

Billboard REITs like Lamar, for instance, are much more economically sensitive… which makes Berkshire Hathaway buying shares all the more interesting.

What Investors Need to Know About Billboard REITs

In my book REITs for Dummies, I cover every single REIT subdivision, or sector. Their strong points, their weak spots, their potential – I delve into it all.

When it comes to billboards, they’re regulated by the Highway Beautification Act of 1965. The law set standards for signage near major highways. But it also limited expansion. From my book:

Since 1965, this has been an intensely regulated industry that makes it exceptionally complicated to expand. The majority of signage found along federal highways was grandfathered into that onerous legislation.

In other words, what exists now has largely existed for decades – almost as long as REITs themselves have been around. Any new construction permits are very difficult to come by.

This creates an almost impenetrable moat for billboards. That’s why only two such REITs exist, Lamar and Outfront Media (OUT), with the smaller non-REIT Clear Channel (CCO) operating as well.

On the downside, this legislation means:

Even upgrading or improving existing signs can be difficult. It’s true that digital billboards have been increasingly dotting the national landscape. Yet there are far fewer out there than there could be due to the legal demands around establishing them. Some cities require landlords to remove two or three existing billboards for every digital asset implemented.

Another issue is how very economically sensitive they are. Billboard REITs get almost guaranteed revenue from restaurants like McDonald’s (MCD) and Chick-fil-A along major highways, it’s true.

But that only takes up so much space. And other companies aren’t nearly so quick to advertise during downturns.

As such, the billboard business can easily underwhelm during periods of stagnant or negative economic growth.

That’s why it’s a good omen that the “Oracle of Omaha” (or at least his company) decided now is the time to invest in them. It suggests the Berkshire analysts believe brighter days are right around the corner.

It’s just a matter of determining how close that corner is.

And since we’re on the topic of billboard REITs, it’s worth taking a look at the two players…

A Tale of Two Billboard REITs

Lamar Outdoor, based in Louisiana, is the oldest of the two billboard REITs. Founded in 1902, it’s one of the world’s largest advertising companies with 363,000 displays across the U.S. and Canada:

-

159,000 billboards

-

5,000 digital billboards

-

138,200 logo signs

-

47,500 transit ads

As with most billboard setups, it doesn’t actually own the land its billboards stand on. Instead, it leases those properties from companies and individuals – like me. I rent land to Lamar in the Greenville-Spartanburg, South Carolina area, where it has around 1.1% exposure.

Outfront Media, meanwhile, is based in New York. Originally called CBS Outdoor Americas, it was spun into a REIT in July 2014 and now operates about 19,600 displays.

These are spread across 120 U.S. markets, including all 25 of the largest. Its top locations are high-profile sites in and around New York’s Grand Central Station and Times Square, various locations along L.A.’s Sunset Boulevard, and the Bay Bridge in San Francisco.

OUT also focuses on delivering mass and targeted audiences to customers.

{kind=link}

Source: Wide Moat Research

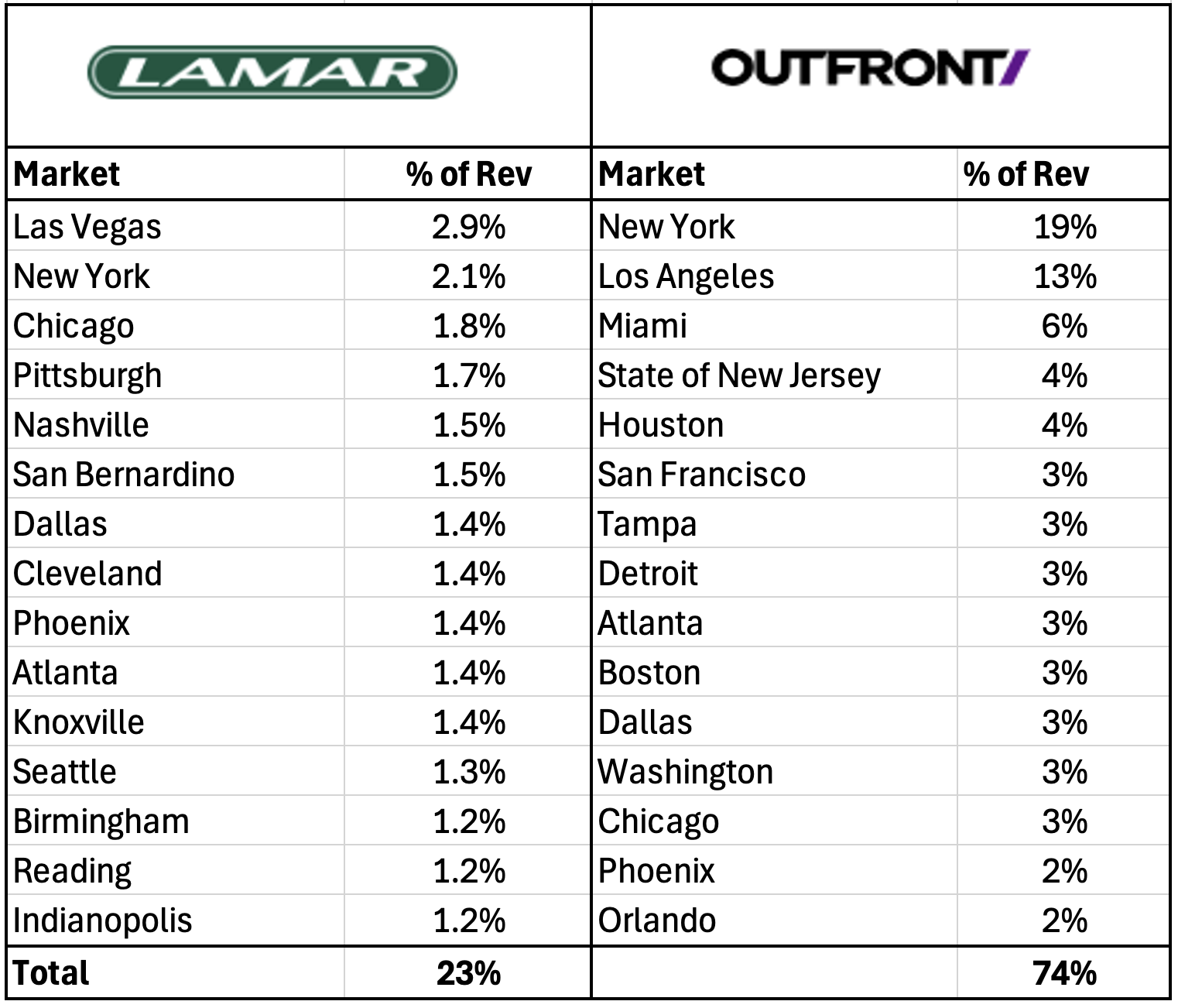

Even so, Lamar’s platform is much more diversified geographically, with 23% of its revenue derived from its top 15 markets. Outfront has outsized risk with its concentration in New York City and Los Angeles.

As my regular readers know, I’ve become much more skeptical of New York real estate after COVID… and even more so now with the possibility of a socialist mayor.

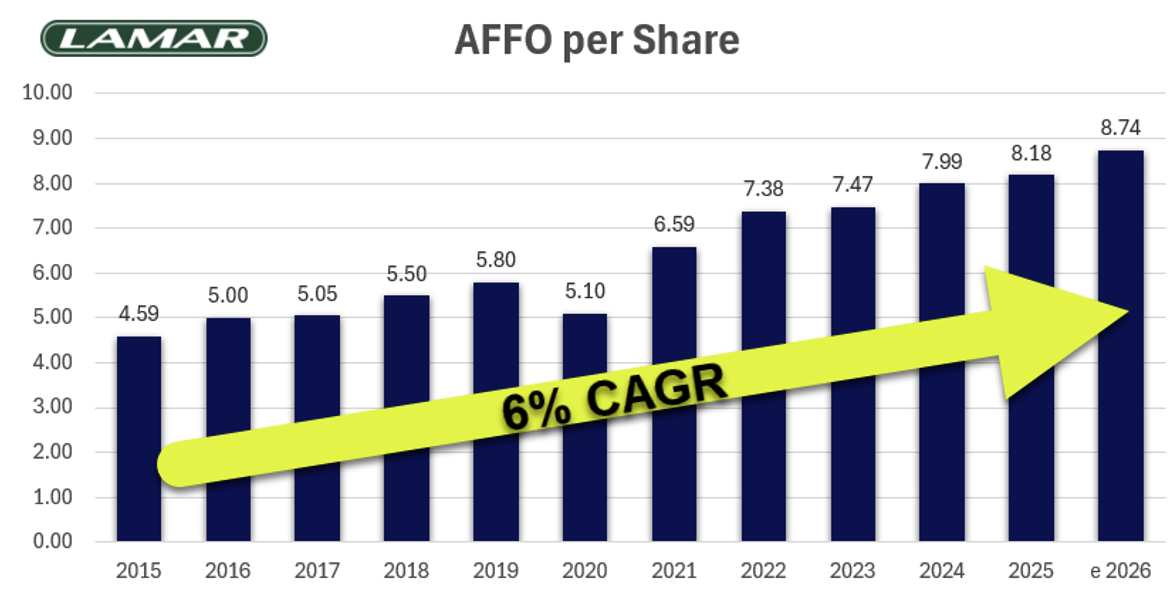

In terms of fundamentals, Lamar also has a much lower risk profile. Earnings have grown by around a 6% compound annual growth rate (“CAGR”) since 2015, even including a modest pullback during COVID.

{kind=link}

Source: Wide Moat Research

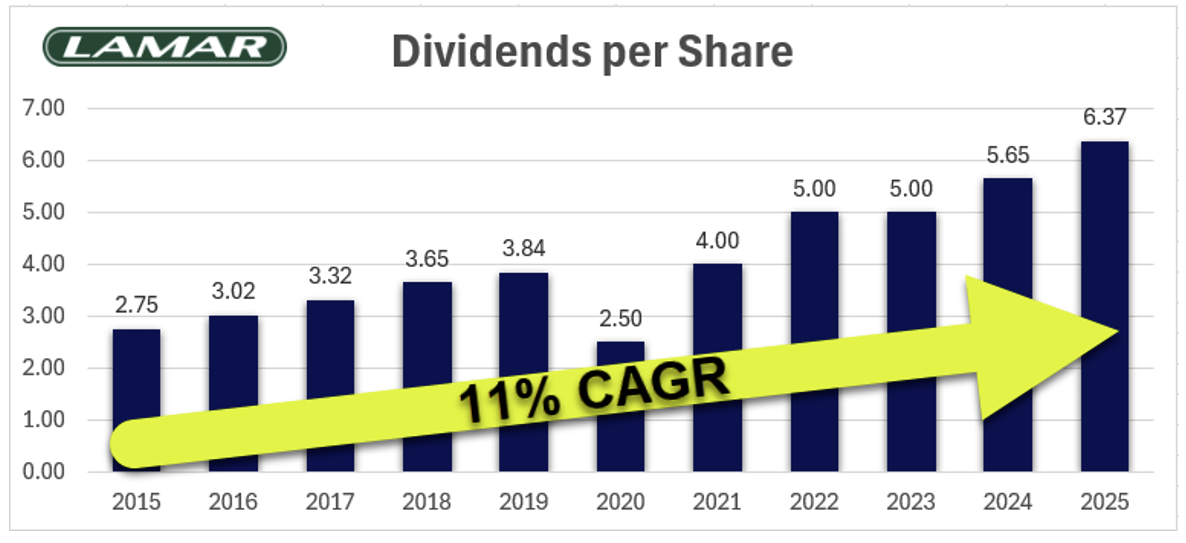

Lamar’s dividend record is another solid indicator. While it was forced to lower its dividend during the shutdowns, it has grown the dividend at an 11% CAGR since 2015. Plus, it enjoys a healthy payout ratio of 78% in terms of adjusted funds from operations (or AFFO, a REIT alternative to earnings).

{kind=link}

Source: Wide Moat Research

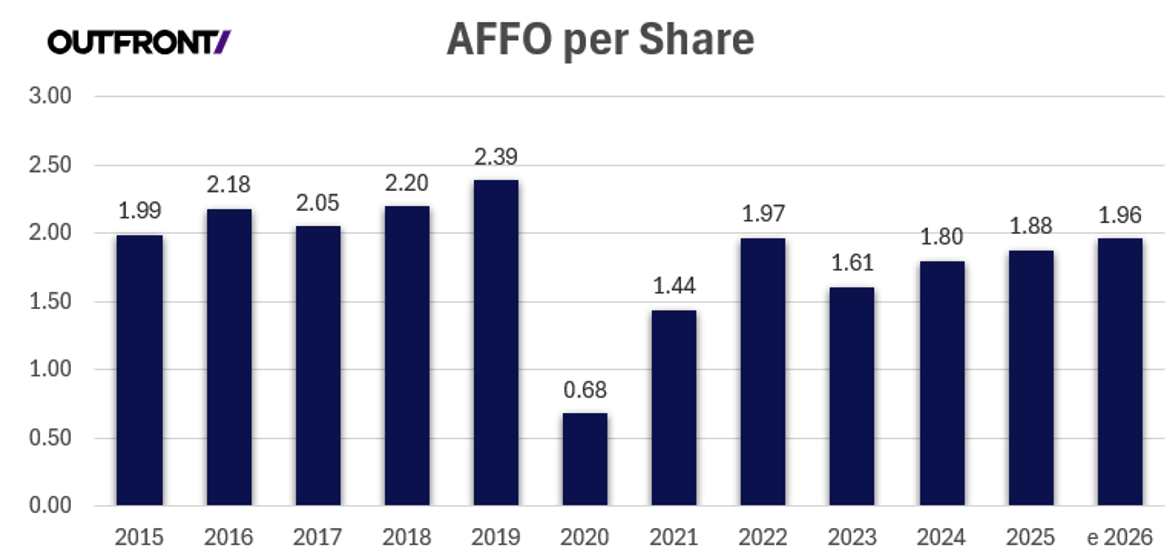

As you can see below, Outfront has a lumpy earnings profile in comparison and still hasn’t returned to pre-COVID levels.

{kind=link}

Source: Wide Moat Research

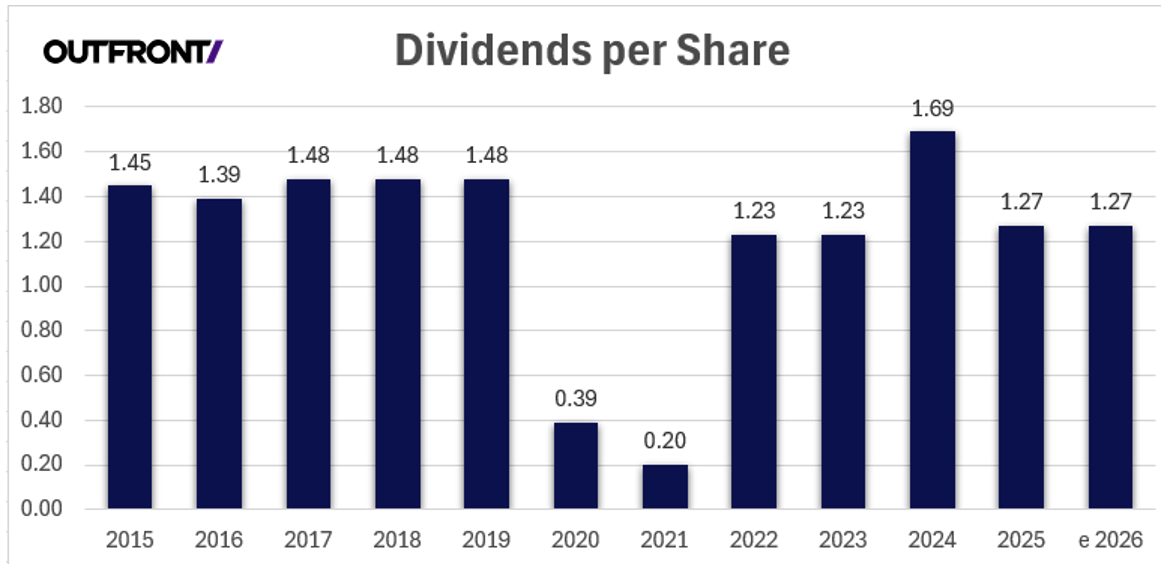

It’s the same story for the dividends. While Outfront was able to pay a modest dividend during the shutdowns, it still hasn’t recovered. And its AFFO-per-share payout ratio is around 67%. That’s less than Lamar’s. But with such unpredictable AFFO growth, I suspect Outfront management is hesitant to grow the dividend, as the next chart will show.

{kind=link}

Source: Wide Moat Research

Even More Reasons to Like Lamar Over Outfront

There’s also the fact that Lamar has a much better balance sheet than Outfront Media.

It currently boasts total leverage of 2.95 times net debt to earnings before interest, taxes, depreciation, and amortization (“EBITDA”). That’s its lowest level ever, and its secured debt leverage sits at just 0.95 times.

Lamar aims to keep total leverage at or below 3 times, with secured leverage at or below 1 times net debt to EBITDA.

Outfront, however, is junk rated by Standard and Poor’s at B+. It has a total net leverage of 4.8 times and $600 million of liquidity, $30 million of which is in cash.

In terms of valuation, it’s true that Outfront is cheaper, trading at 10.1 times instead of its normal multiple of 11.6 times. And its dividend yield is a tempting 6.4%.

{kind=link}

Source: FAST Graphs

However, it’s clear Buffett made a much better bet with Lamar, which is now trading at 15.2 times, slightly above its normal 14.6 times. Of course, Berkshire didn’t purchase shares today. It would have taken some time to build that position. Assuming Berkshire purchased shares around April, they would have bought below that historical multiple. And shares would have returned around 12% so far.

{kind=link}

Source: FAST Graphs

Regardless, I’m happy to see Buffett back in REIT-dom. To my knowledge, the last purchase Berkshire Hathaway made within the sector was in January 2017, when it bought a $377 million stake in the now privately owned Store Capital.

Maybe this is the start of a beautiful new beginning? In which case, there are many other quality REITs I could suggest. I’ll cover that in a future Wide Moat Daily article.

Stay tuned!

Regards,

Brad Thomas

Editor, Wide Moat Daily

|