When Warren Buffett speaks, most intelligent investors listen.

A stock-picking genius, his Berkshire Hathaway (BRK-A)(BRK-B) has made shareholders a fortune over the decades. The primary class is up over 51,000% since going public in 1980.

Like most people, I respect Warren Buffett. I even named Wide Moat Research after a concept he popularized – the idea of investing in businesses with “wide moats.”

But Buffett doesn’t have a crystal ball – something he acknowledges as well. He’s been frank about his past mistakes, and I’ve never heard him ask anyone to blindly follow him.

Buffett also knows he has different advantages and disadvantages than the average investor. Being a market mover, for instance, he can’t really buy up smaller-cap companies. He’d move their prices too much by just getting involved.

Keep all that in mind as you digest the recent news that Berkshire bought into two U.S. homebuilders: Lennar (LEN) and D.R. Horton (DHI) earlier this year – a sector I’ve repeatedly said over the past eight months that I’m avoiding.

As I wrote on July 31, the U.S. housing market remains “a mess.” The spring season – “typically the busiest time to buy and sell a home – was the worst it has been in over a decade.”

Between high list prices, high mortgage prices (even if they did drop this month), and how debt-ridden consumers are… there’s not much incentive for people to buy a home these days. Which means there’s not much room for homebuilders to profit.

Even so, considering the Buffett news, I went and crunched their numbers over the weekend. And here’s what I found…

Digesting Homebuilders’ Latest Earnings

Let’s begin with the Buffett picks: Lennar and D.R. Horton.

Lennar, for its part, generated operating earnings of $157 million in its latest quarter. And that is up from $146 million in the second quarter of 2024.

That was mainly due to its mortgage business, not its home sales. But a profit is a profit, and a gain is a gain. So, let’s recognize the win for what it is.

On the downside, it missed earnings estimates of $1.94 per share by four cents. That was especially surprising considering how it beat in the first quarter at $2.14 per share compared with the expected $1.74.

Looking forward, Lennar’s third-quarter average sales price should be about $380,000 to $385,000. And its gross margin should be approximately 18%.

But one way or the other, it’s not trading at a bargain right now. As you can see below, it’s actually overpriced at 13 times versus its normal 10.3 times multiple.

{kind=link}

Source: FAST Graphs

Buffett may have announced the position recently, but Berkshire was undoubtedly building the position over the past several months. So, perhaps he got a better average entry. But for any investors looking to follow along, I’d be careful at these levels.

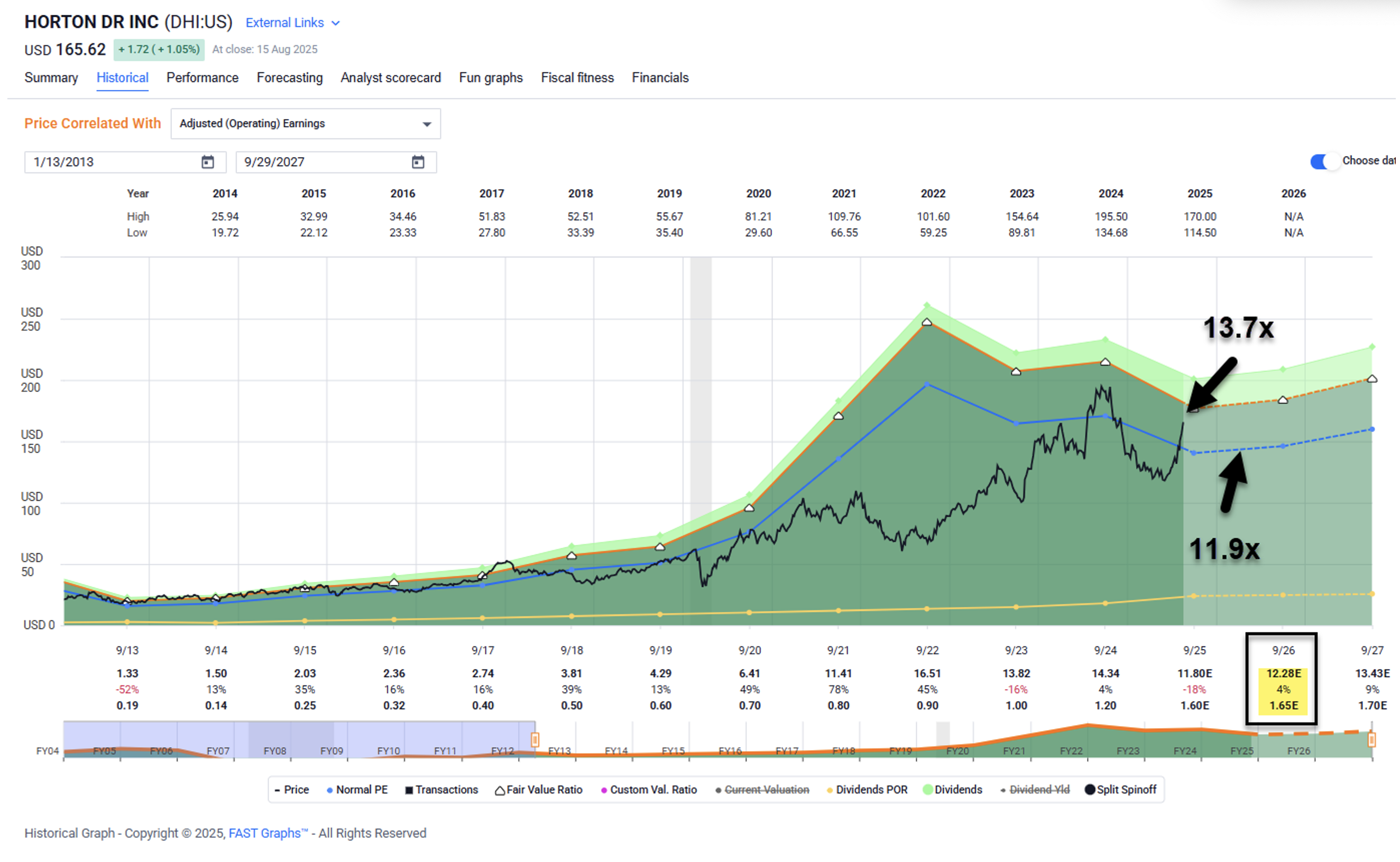

It’s a similar story with D.R. Horton.

The company delivered solid results last quarter. It generated earnings per share of $3.36 compared with $4.10 in the first quarter, and pretax income was $1.4 billion.

The homebuilder closed on 23,160 homes, which was down from 24,155 homes in the prior quarter. But that was still above its guidance range, and those sales came with a gross margin of 21.8% – which was also better than expected.

Once again though, I have to consider this investment from a value investor’s lens. Shares are trading at 13.7 times, which is over 200 basis points above D.R.’s normal valuation.

{kind=link}

Source: FAST Graphs

Analysts are also forecasting only modest consolidated revenue growth of 4% in 2026.

Now, let’s have a look at a few names Buffett didn’t invest in.

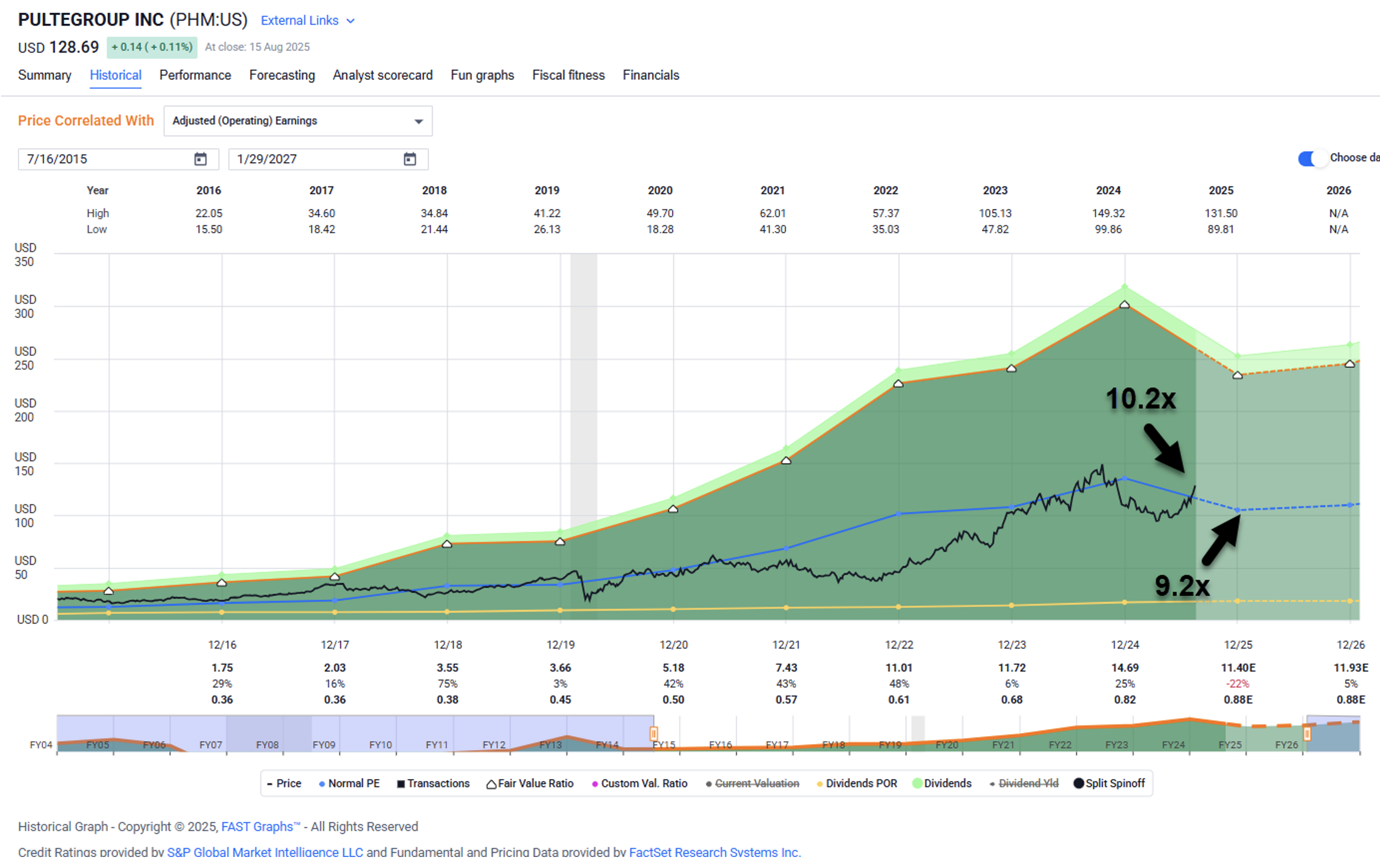

PulteGroup (PHM) beat on both quarterly revenue and earnings estimates. However, new orders were down 7% year over year to 7,083 homes. And home sale revenue was down 4% to $4.3 billion.

While investors hailed the news anyway, sending the stock upward… that just means we’re once again facing modest overvaluation. PulteGroup is trading at 10.2 times instead of its normal 9.2 times.

Analysts are forecasting 5% growth, though not until next year.

{kind=link}

Source: FAST Graphs

Another common homebuilder play is Beazer Homes (BZH). It generated $565.3 million in the second quarter, up from $541.5 million a year earlier. However, net profits fell from $39.2 million to $12.8 million. And operating cash flow fell from $14 million to $3.5 million.

That’s quite the drop, yet Beazer’s shares are now trading at 15 times. That’s much higher than the normal valuation multiple of 5.9 times.

There are no bargains with this builder right now.

{kind=link}

Source: FAST Graphs

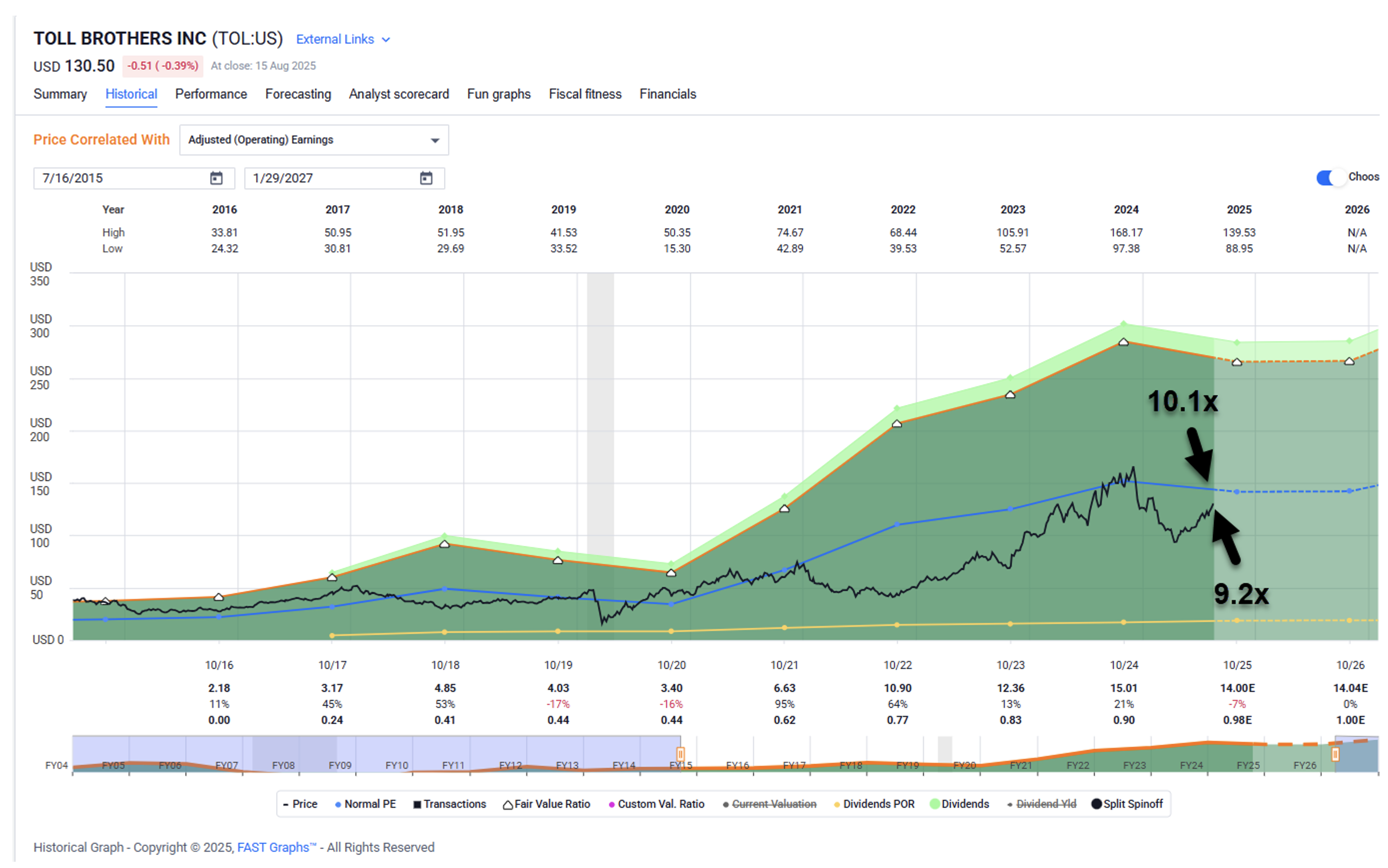

The Exception to the Homebuilder Rule

In this cycle, where affordability is such an issue, I like luxury homebuilder Toll Brothers (TOLL). On its latest earnings call, CEO Douglas Yearley explained how:

With many entry-level buyers struggling with affordability challenges, we are pleased to be serving an affluent consumer. Over 70% of our business serves the move-up and empty nester segments. These buyers are wealthier, have greater financial flexibility and most have equity in their existing homes.

With an average second-quarter home price of approximately $983,000, the financial strength of Toll Brothers’ customer base is highlighted by its:

- Industry-low cancellation rate

- Low loan-to-value ratios for those who do take out a mortgage

- High percentage of all-cash buyers.

In fact, around 24% of buyers paid everything upfront in the second quarter of 2025, up from Toll Brothers’ long-term average of approximately 20%.

As seen below, it’s still somehow trading at 9.2 times, below its normal valuation multiple of 10 times. As such, I view this homebuilder as the most attractive of the lot based on both quality and value.

{kind=link}

Source: FAST Graphs

Even so, I have to say that there are many better opportunities out there if you want to invest in the residential real estate sector. This includes through real estate investment trusts, royalty companies like Texas Pacific Land (TPL), asset managers like Blackstone (BX), and energy-focused firms such NextEra (NEE) or IdaCorp (IDA).

Tune in this week to my YouTube show, where we’ll be discussing several of these alternatives in greater detail.

Buffett may be buying homebuilders. But – with few exceptions – I’m not. And I hope readers will consider the numbers above before they enter this space, especially with so many better alternatives available.

Regards,

Brad Thomas

Editor, Wide Moat Daily

The Wide Moat Show

Longtime readers will know I’ve always warned against “sucker yields.” These are dividends that are so high that they seem too good to be true. That’s because, more often than not, they are…

Sucker yields are prime targets for dividend cuts. And that makes them worth avoiding.

But today, Nick and I will share a few high-yielding stocks that are reliable. And Nick will even share an options strategy he has been using to generate reliable income from the market.

For any income-oriented investors, today’s episode will be a can’t-miss.

Be sure to catch it all right here.

MAILBAG

Do you agree with Brad that there are reasons to be optimisitc about Main Street America? Write us at feedback@widemoatresearch.com.