“On Tuesday, the roof caved in on software, media, and information company stocks… “

That’s how Adam Levine for Barron’s described the carnage we’re seeing in software and related companies.

And the description is apt…

The iShares Expanded Tech-Software Fund (IGV) – which holds a basket of software stocks – is down about 21% over the past month.

The reason behind that collapse was artificial intelligence (“AI”) – specifically, Anthropic’s newest round of AI tools from its Claude Cowork, a desktop app that can read, create, and edit computer files. It’s apparently now branching out into sales, finance, legal tasks, and customer support.

Put another way, the AI seems capable of handling tasks typically accomplished by enterprise software. That led Mr. Market to lose faith in the companies selling that (very expensive) software.

But while the “SaaS-pocalypse” brought software stocks low, the fear also bled into another area of the market – business development companies (“BDCs”).

BDCs offer loans to small, mid-sized, and specialized businesses that might otherwise struggle to obtain meaningful funding. Since many software companies fit into that “specialized” category, they often seek out BDCs to help them grow. As Stephen Hester shared yesterday, enterprise software usually represents about 15% to 25% of a private-credit portfolio.

That’s why Claude’s new capabilities scared BDC investors, sending many down 5% or more.

But as so often happens, Mr. Market overreacted.

The Hallucination Problem

To quote the aforementioned Levine again, “While the AI tools show the potential power of AI in office work, they’re not ready for prime time and, in fact, could prove dangerous to the companies that use them.”

Mr. Levine is referring to the so-called “hallucinations” that often crop up in large language models. Put more simply, these models sometimes make stuff up. In fact, every single AI model comes with that disclaimer.

These hallucinations may not happen often, but they do happen. You have to wonder if large companies would really risk their entire operations by depending on a program with such an existential risk of failure.

Somehow, I doubt it…

And despite the weakness in software stocks, Wall Street seems to doubt it, too. Here’s our own Nick Ward sharing some details on Intuit (INTU), one of the victims of the sell-off.

During its most recent quarter, Intuit beat Wall Street’s expectations on both the top and bottom lines, posting year-over-year revenue growth of 17.9% and earnings-per-share (“EPS”) growth of 34%.

The company also established full-year 2026 guidance, which called for earnings growth of approximately 15% during the upcoming year.

Wall Street agrees, calling for 15% EPS growth this year and 14% EPS growth during both 2027 and 2028.

That certainly doesn’t seem like a company at risk for imminent bankruptcy…

So, if the sell-off in software names is overblown, then the sell-off in BDCs likely is, too.

And that means the short-term volatility could present some attractive entry points for BDC investors brave enough to wade into the panic.

But just keep this in mind…

A Crash Course on BDCs

We often cover the benefits of real estate investment trusts (“REITs”) at Wide Moat Research. One of the biggest is the mandate to distribute at least 90% of their taxable income to shareholders. That’s why REITs are known for having higher yields than your average dividend stock.

BDCs abide by the same rule. However, REIT shares tend to yield 3% to 8%… whereas BDCs go into the double digits at 10% to 13%.

Now, before you race to go buy them all up, understand that’s not the only difference between them and REITs. As I often tell retirees and other investors with income concerns, BDCs are inherently riskier than REITs.

For instance, they typically run about 1 to 1.25 times debt-to-equity ratios. They also finance their operations through short- and intermediate-term floating rate debt while the financing they offer tends to be longer-term.

This works for them in the best of times. And, to be fair, there are plenty of BDCs that have survived through the worst of times.

However, their stocks tend to be much more volatile as a result.

REIT leverage, admittedly, varies sector to sector. But it’s usually secured against tangible property – the kind that AI or anything else can’t really replace. That’s why their returns tend to be stable while BDCs are more prone to boom-and-bust swings.

The Kind of BDCs to Look For

Here’s one more thing you need to know about BDCs: Unlike REITs, they tend to do better when interest rates are higher.

Since most of them borrow at fixed rates and lend at floating rates, their earnings decline when those spreads narrow – sometimes to the point where they have to cut their dividends.

Sometimes by quite a lot.

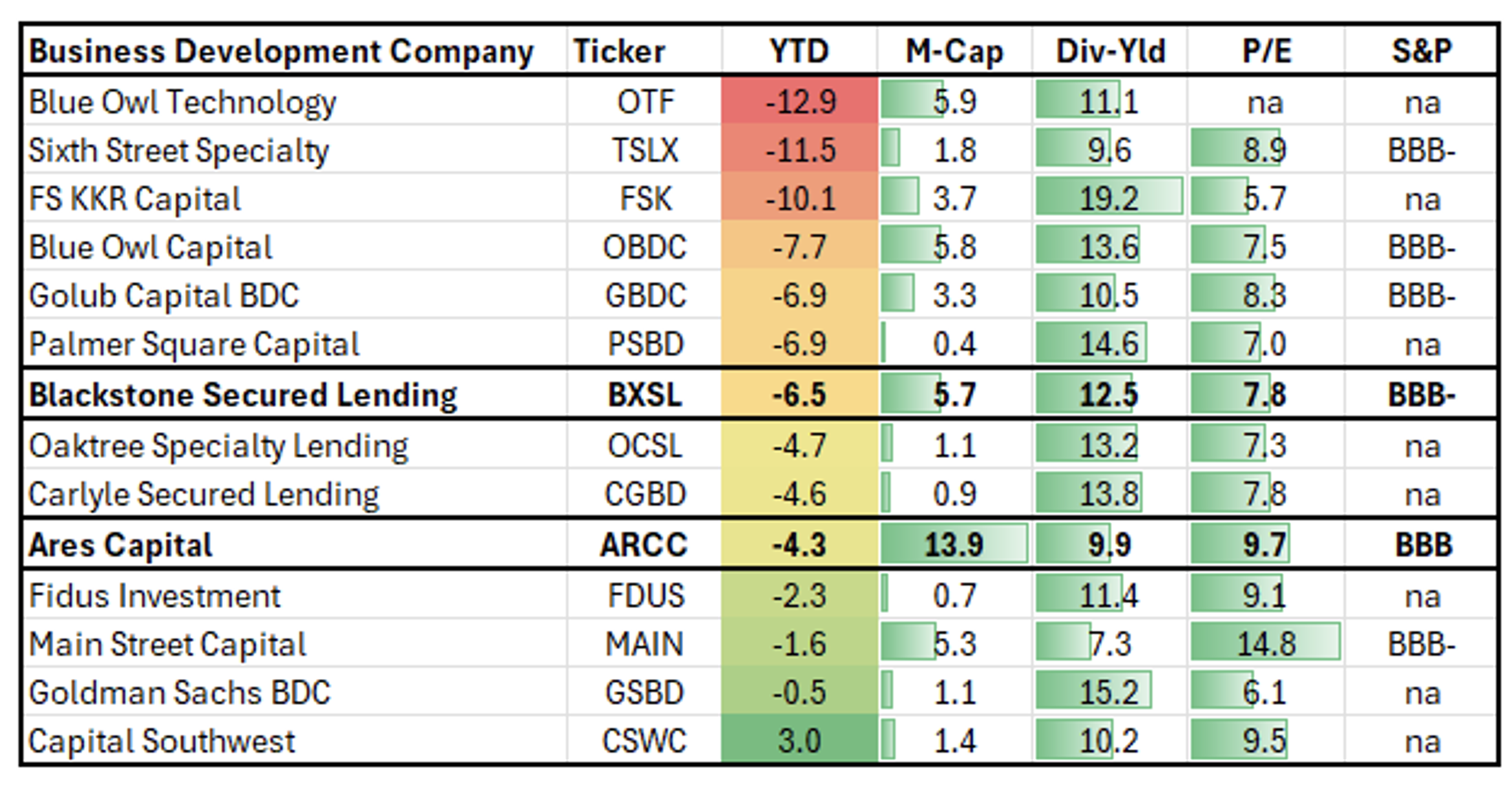

That’s why it’s so important to screen for BDCs with strong balance sheets, healthy payout ratios, and a history of managing credit risk. Two names that stand out in that regard are Ares Capital (ARCC) and Blackstone Secured Lending (BXSL).

Ares has scale advantage with a $13.59 billion market value. It’s focused on financing firms that secure data-center capacity and renewable energy. And most of you know how I feel about data centers.

(If you don’t, read my latest article on the topic here.)

Also, Ares’ software portfolio has a solid loan-to-value of just 37%. In fact, its Capital CEO, Kort Schnabel, said the company’s portfolio quality in general is in “excellent shape,” with non-accrual loans around 1% of the portfolio.

Ares, which is rated BBB by S&P, has over $156 billion of dry powder. Analysts are forecasting -3% EPS growth in 2026 and -1% in 2027. But that might not matter if you’re buying it on the cheap like it is right now.

Its dividend yield is 9.9% and appears to be covered for the time being.

As for Blackstone Secured Lending, it generates revenue from its conservative 97.5% of first-lien senior secured loans. The firm does have software exposure at around 20%. However, like Ares, its average loan to value is less than 50%.

Blackstone also has a strong balance sheet, rated BBB- by S&P, with ample liquidity of $2.5 billion. It’s true that analysts expect it to produce -8% growth in 2026, but its dividend should remain covered regardless.

And again, it’s trading well below even those unimpressive predictions. Both BDCs are. Ares Capital now trades at around $19 – a 5% discount to its net asset value (“NAV”) – while Blackstone is sitting at a 10% discount.

That’s just what happens when Mr. Market sells the headlines: It opens up room for us to buy the dips.

{kind=link}

Source: Wide Moat Research

Regards,

Brad Thomas

Editor, Wide Moat Daily

|