In the 19th century, railroad stocks dominated the U.S. market.

These companies weren’t mere modes of transportation. They were the infrastructure powering America’s rise as an industrial powerhouse. They linked farms, cities, factories, ports, raw materials, and production centers together, creating an increasingly more efficient system of production and commerce.

Investors rewarded that critical infrastructure. Railroads represented about 60% total U.S. stock market capitalization in 1900. Really, railroads didn’t just dominate the stock market back then. In some sense, they were the stock market.

These were (and still are) capital-intensive businesses. Railroads demanded enormous piles of cash for years or even decades before profits were possible. There was land to acquire; earth to be graded and moved; tracks to install; locomotives and railcars to manufacture; stations, depots, and railyards to build…

As a result, they had to rely on sophisticated financing structures involving corporate bonds, equity offerings, and investment banking. All these options already existed, of course, but railroads took them to the next level.

They also relied on foreign capital, particularly from Great Britain and mainland Europe. In return, they were the first U.S. sector to attract modern-day levels of global capital.

You can probably guess where I’m going with this…

The New Railroad

Today, there are eight companies that dominate the S&P 500.

Those would be:

-

Nvidia (NVDA)

-

Apple (AAPL)

-

Microsoft (MSFT)

-

Amazon (AMZN)

-

Alphabet (GOOG/GOOGL)

-

Meta Platforms (META)

-

Broadcom (AVGO)

-

Tesla (TSLA)

As I write, these eight stocks represent about 36% of the S&P 500’s weighting. And as I’m sure you noticed, they’re all tech firms with big plans for artificial intelligence (“AI”). These are the new railroads.

And like the railroads of the 19th century, they need mountains of cash to build out their infrastructure. Nick Ward provided some details in today’s Conviction List update for The Wide Moat Letter (catch up here).

Alphabet is expected to spend as much as $185 billion in capital expenditures (“capex”) this year. Meta could spend as much as $135 billion. And Amazon is guiding for capex in the ballpark of $200 billion for 2026. Together, that’s $520 billion, more than the GDP of Norway.

And it’s just three companies…

It’s easy to look at the rise of AI as one giant profit opportunity. But investment is never that simple.

The Four Most Dangerous Words in the English Language

The four most dangerous words in the English language are “this time is different.”

In the case of the railroads, even decently established entities fell victim to overexpansion, economic downturns, and other catastrophes along the way.

Take the Pennsylvania Railroad, which was once the world’s largest railroad organization. And it expanded its scope even further by merging with the New York Central Railroad in 1968 to create Penn Central Transportation Company.

But that wasn’t enough to save it from increasing regulations, heavy infrastructure costs, and the rise of the trucking and aviation industries. In 1970, it was forced to file for the largest corporate bankruptcy in American history up until that point.

You really never know what’s going to happen.

Barring some act of God, AI will continue reshaping how we do almost everything for decades to come. This is not a force we should or even can ignore. But assuming every AI company will be a winner long term is a mistake.

At Wide Moat Research, we’re not interested in picking horses. We simply don’t know which AI model will win out and claim market share over the long term.

But here’s what we do know…

The Data-Center Path to Profits

Data centers are to AI what tracks are to railroads in the sense that, without the former… You can’t have the latter.

I’ve written about data centers – specifically in the context of real estate investment trusts, or REITs – for a solid decade now. The presentation I released this year is a culmination of that investigative and ongoing journey.

It’s marked by private equity firms such as Blackstone (BX), KKR (KKR), and GI Partners that have acquired data-center platforms and funded large-scale development pipelines. Their involvement signals the magnitude of the AI opportunity…

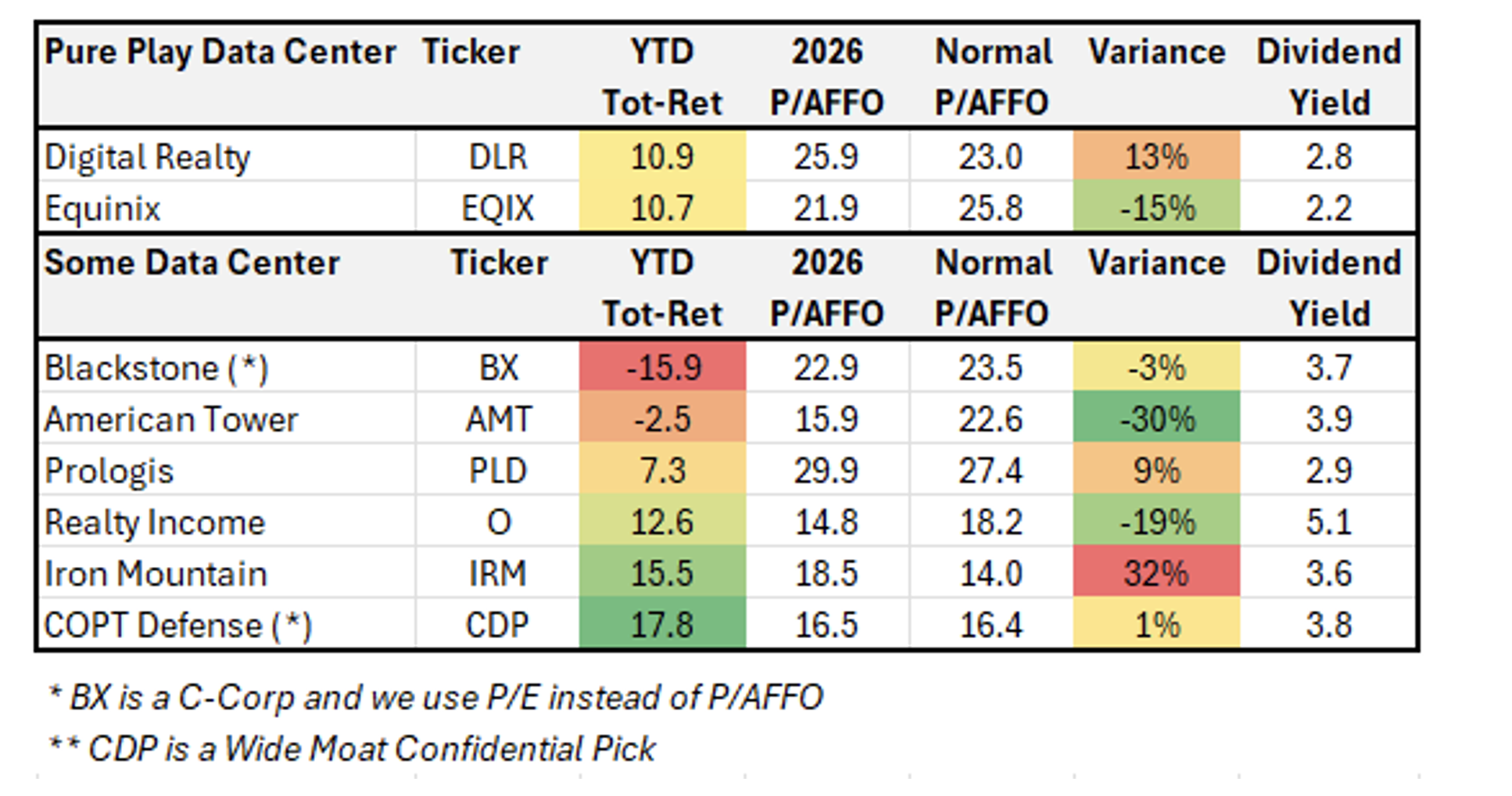

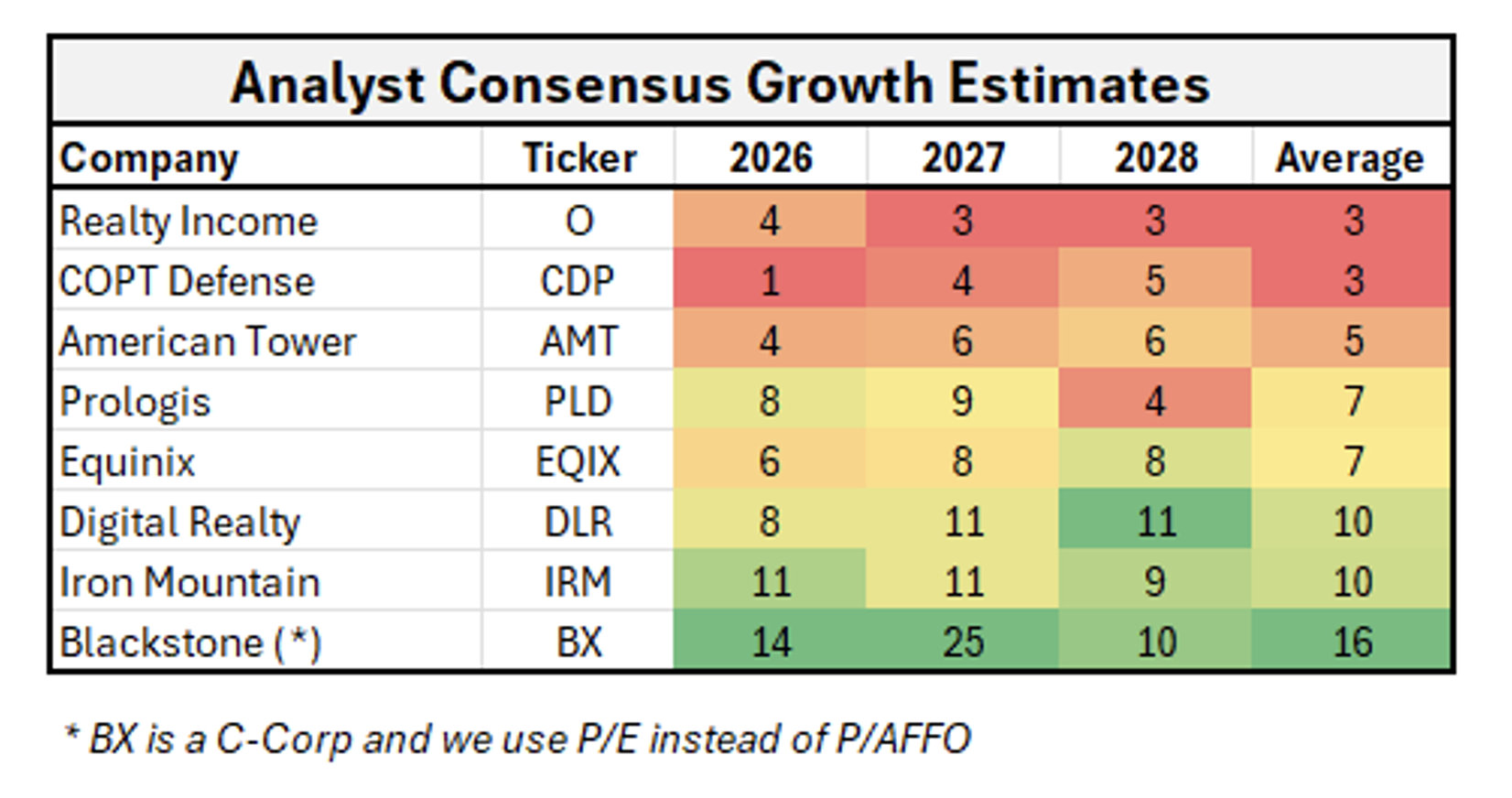

That’s why I’ve been so focused on pure-play data-center giants such as Equinix (EQIX) and Digital Realty (DLR) lately. Nor have I ignored how other-sector REITs have increasingly entered the game, such as:

-

Iron Mountain (IRM)

-

Realty Income (O)

-

Prologis (PLD)

-

COPT Defense Properties (CDP)

-

American Tower (AMT)

{kind=link}

Source: Wide Moat Research

They all understand the importance of providing infrastructure. Control the means of transportation, as it were, and you dictate the entire game.

This doesn’t mean every single data-center venture is a guaranteed success story, though. For instance, I’ve already mentioned Fermi (FRMI) several times since its October 1, 2025 debut. While the company saw its stock leap 55% to $32.53 in its IPO, it’s now the subject of multiple class-action lawsuits and was trading at a dismal $8 at Friday’s close.

For the record, that’s after rising 11.11% over Thursday.

You see, it has no actual operating, profit-making properties currently. Moreover, it lost a $150 million funding deal back in December that shocked its investors.

Fermi might still be able to pull itself together, and we still have it on our watchlist. But for the time being, it should serve as a very real example of why we always invest in quality over hype.

Just because a company is associated with a highly profitable trend doesn’t mean it will profit.

We also want to be careful about how and when we invest in even the most well-established data-center businesses. If they’re trading at a premium, we could still end up losing money when valuations eventually contract. As they always do.

That’s why I put my data-center presentation together, which you can still get access to by clicking here. And that’s why I’ll continue to evaluate the sector going forward.

I have absolutely no doubt there’s more profits to be made in this revolutionary sector… at least for those investors who know how to follow the right tracks.

{kind=link}

Source: Wide Moat Research

Regards,

Brad Thomas

Editor, Wide Moat Daily

|