There’s always an excuse to be greedy… especially in a bull market.

In many ways, greed is an evolutionary phenomenon. Thousands of years ago, when human beings were still hunted regularly by wild animals, we learned that the penalty for having too little was much more severe than the penalty for having too much.

And so, we collect, we store, we accumulate… far beyond what we actually need. That human instinct is why storage facilities are such a large industry.

Probably the most influential study on greed came from American psychologist Leon Festinger in 1945. His “Theory of Social Comparison Process,” stated that “There exists, in the human organism, a drive to evaluate his opinions and his abilities.”

But what to evaluate ourselves against? The answer, of course, is other people. Festinger’s study is where we get the phrase “keeping up with the Joneses.”

Your friend or neighbor buys an AI stock/crypto/meme stock, sells it, and makes a bundle. “Why didn’t you?” your mind shouts at you.

And so, we do the predictable – take far too much risk, with assets we scarcely understand, to achieve returns that we really don’t need.

This phenomenon, it turns out, also applies to dividend investing.

Last Friday, Nick Ward wrote a great piece about how Gen Z has become fixated on dividends (which sound great.) But they don’t seem satisfied with the reliable dividends paid by wide-moat companies made possible by sturdy cash flows. Instead, they’re reaching higher… thanks to leverage and derivatives.

I’ll echo Nick’s message from that essay: If it sounds too good to be true… it probably is.

To me though, those high-yielding assets are (more often than not) a “sucker yield.” My longtime readers will know all about sucker yields. They’re the dividend yields that seem too good to be true… because they usually are.

And so, I thought today might be a good opportunity to revisit the topic.

The Anatomy of a Sucker Yield

A sucker yield is exactly as it sounds: a dividend yield that’s temptingly, but unsustainably, high. This happens when a company’s stock price and its earnings erode while its payout amount stays the same or even rises.

The exact percentage where a dividend yield enters “sucker” territory can and will vary. There are companies that can sustain very high yields. And there are instances where the market will irrationally push down a stock, thus raising its dividend yield.

For instance, the real estate investment trusts (“REITs”) I write about so much tend to have higher yields by nature. They’re legally required to pay out at least 90% of their annual taxable income to shareholders via dividends. This means they often offer bigger dividends compared with their share prices.

Even so, there is a certain point where bigger becomes decidedly not better. As I explain in REITs for Dummies:

A REIT that yields 10 percent or higher almost always means (with some exceptions) that investors perceive very low growth or, even worse, a potential dividend cut up ahead. It’s tempting to act on that kind of percentage, but it usually ends badly.

I also wrote:

If a stock seems to pay out a dividend that’s exceptionally high, investors should look even harder at the payment behind that dividend than they otherwise would. When a REIT [or any other kind of stock] pays a dividend beyond its earnings power, it’s essentially eroding capital. It has to find money to cover its obligations, borrowing from its savings, operations, or elsewhere until it can’t even do that anymore. (Or, much less likely, it manages to dig itself out of that financial hole.)

That’s an important point. The dividend yield itself only tells you so much. More important is the payout ratio, the percentage of earnings – for REITs, it would be a comparable metric like funds from operations – going to shareholders in the form of dividends.

REITs, due to their structure, have high payout ratios. But any company that sustains a payout ratio above 100% for long enough will, by simple arithmetic, eventually be forced to cut.

I’ve seen this kind of scenario play out far too many times. And while I’ve very often been able to warn readers about it, saving some of them thousands of dollars in the process…

Others ignore my advice, give in to greed, and suffer the painful consequences.

It’s ultimately each individual’s choice whether he’ll get swayed by a sucker yield or not. But in an effort to help you make the most informed decisions you can, here are some warning signs I’m seeing right now…

Once a Sucker, Still a Sucker

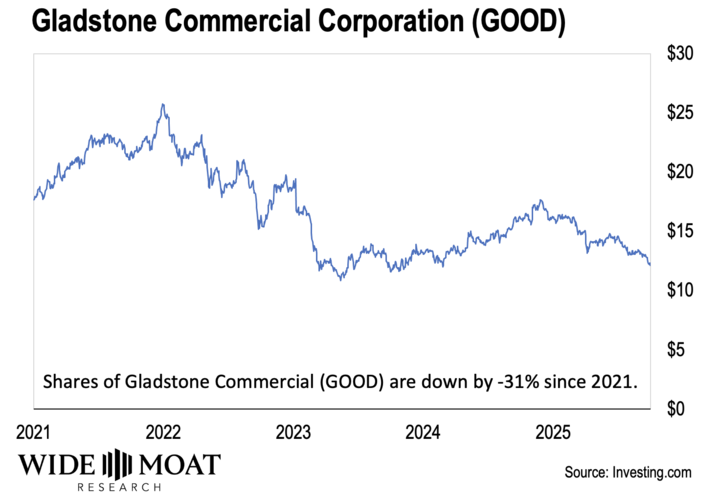

Back in May 2021, I wrote an article on Seeking Alpha titled “Gladstone Commercial: Too Good to Be True.” At the time, Gladstone (GOOD), a net-lease REIT, was trading at $20.67 per share and yielding 7.2%.

That was warning sign No. 1. A yield that high meant shares were sold off. And Mr. Market (usually) dumps a stock for a reason.

Another negative is how it was (and still is) externally managed by – often a telltale sign that a C-suite isn’t properly aligned with shareholders. As I explained:

… having an internal management team could allow the company to focus on creating shareholder value by growing earnings per share [in the form of adjusted funds from operations, or AFFO]… instead of AUM (assets under management). One of the disappointments with GOOD (since the IPO) is that the company has maintained a flat growth rate.

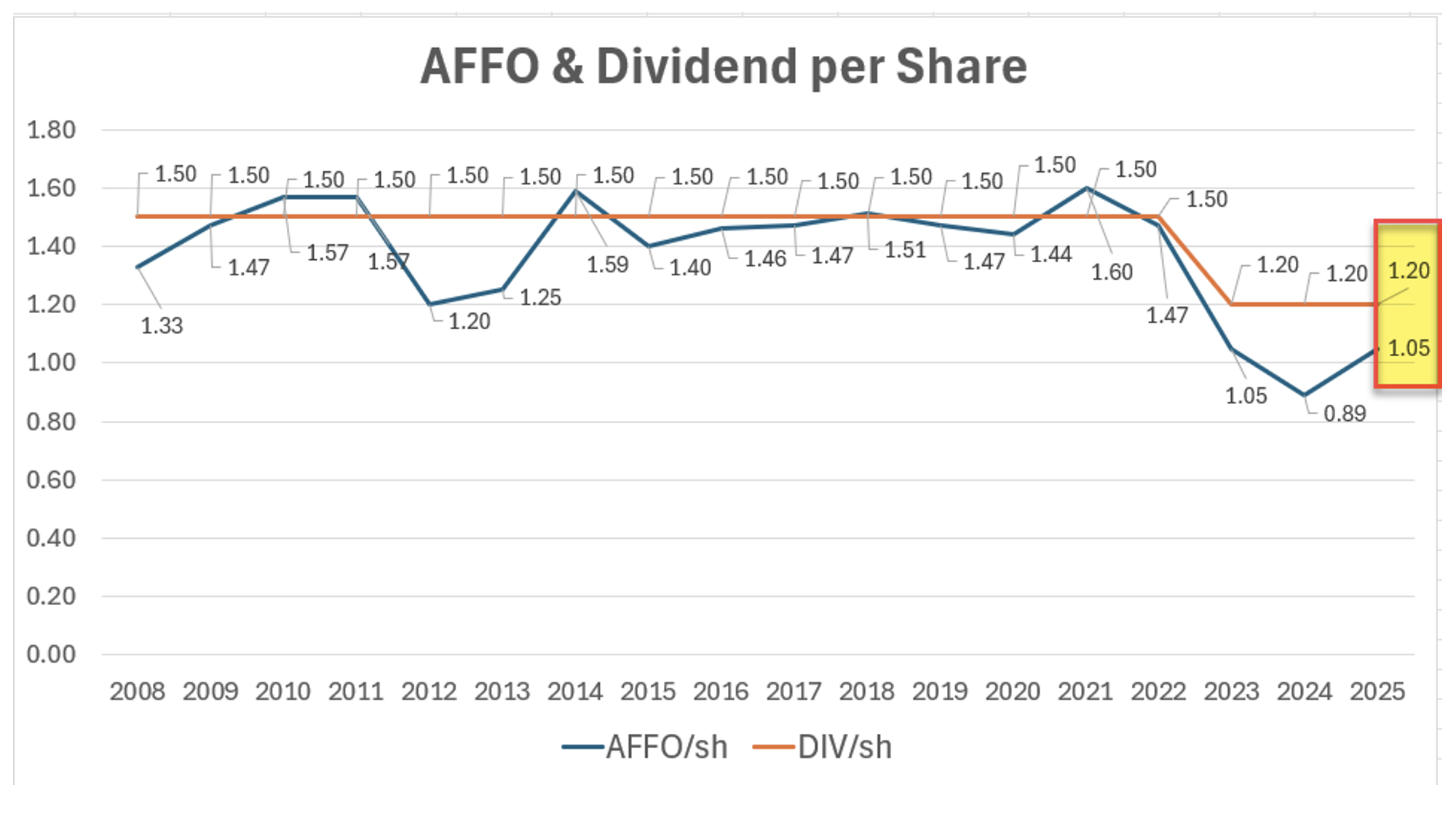

I also noticed that Gladstone’s payout ratio was “strikingly dangerous: 104% in 2021 and 111% based on analyst AFFO per share estimates.”

As it turned out, this was a wise call. Gladstone did indeed cut its dividend in January 2023 by around 20%.

But things haven’t gotten better from there. Since that May 2021 article, shares have crashed by around 31%.

{kind=link}

Worse yet, Gladstone remains a sucker yield with a payout ratio of 114%. This means its dividend of $1.20 per share is higher than its AFFO per share of $1.05.

{kind=link}

Source: Wide Moat Research

It’s only a matter of time before this REIT has to cut again.

Buyer Beware

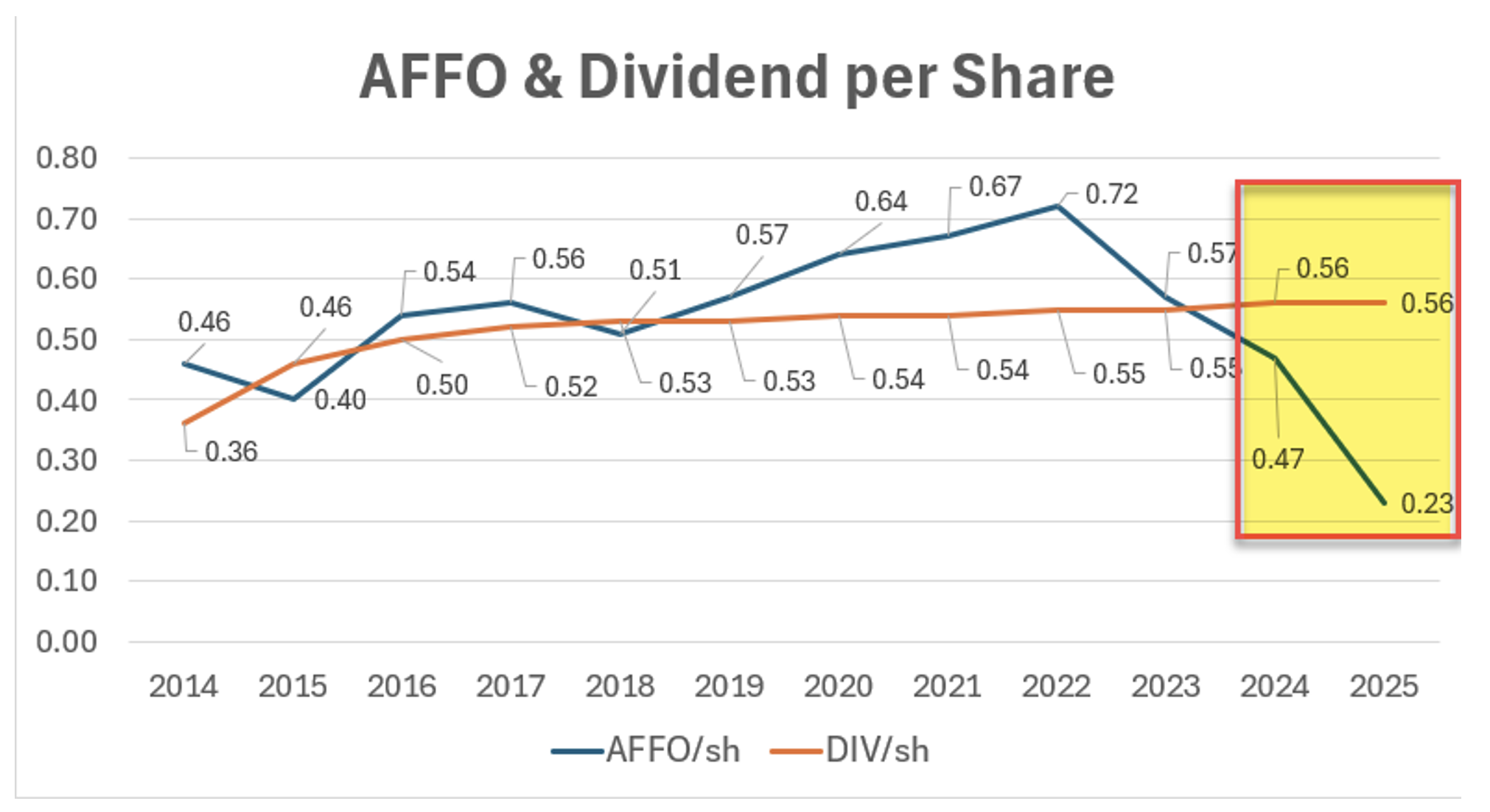

Gladstone Land (LAND) is another problematic company with another elevated payout ratio. It’s also externally managed – and by the same company Gladstone Commercial operates under, The Gladstone Companies.

In the second quarter, LAND recorded a net loss of about $7.9 million. Its net loss for common shareholders was $13.9 million, or $0.38 per share.

AFFO, meanwhile, was down $3.4 million, or down $0.10 per share compared with $3.7 million, or $0.10 per share, in the second quarter of 2024.

As seen below, Gladstone Land is also paying out a much higher dividend than it can afford. In fact, its payout ratio is an enormous 240%!

So, there’s no way this situation is going to end well for shareholders.

{kind=link}

Source: Wide Moat Research

Call me crazy, but I prefer to see companies with a strong dividend record. It demonstrates that management is committed to their shareholders. As you’ve heard me say many times here at Wide Moat Research, “the safest dividend is the one that just been raised.”

And there’s no raising being done at the Gladstone REITs.

Happy SWAN (sleep well at night) investing!

Regards,

Brad Thomas

Editor, Wide Moat Daily

|