I love interacting with the Wide Moat Research audience. It’s genuinely one of my favorite things to do.

I can’t tell you how much I enjoy getting up and speaking to those of you who can attend my conferences… or taking questions afterward… or getting questions by e-mail, on YouTube at The Wide Moat Show, on X (@rbradthomas), or LinkedIn.

I’m not exaggerating when I say I appreciate each and every one of you. Yes, even those of you who ask tough questions or even make less than flattering comments. All of that keeps me engaged and humble.

Occasionally, I receive a question from readers who are just starting to build out the real estate investment trust (“REIT”) segment of their portfolio.

The question is “What is adjusted funds from operations (‘AFFO’)?”

It’s a fair question because, unless you’re familiar with REITs, it’s likely not a metric you would come across much when looking at more traditional stocks.

So, that’s what we’ll tackle today. If you’re a newer reader, I hope you find it helpful. And if you’re a longtime reader, a refresher never hurts.

AFFO: The REIT Version of EPS

At Wide Moat Research, we reward companies with proven track records for growing operating cash flow and free cash flow. That gives them more opportunity to reinvest in their businesses, pursue acquisitions, or return the money to shareholders via dividends or stock buybacks.

But healthy free cash flow looks different from company to company and asset type to asset type. And it can look especially different for REITs, which are unique in how they report earnings.

That’s why I get asked about their free cash flow so often. And that’s why I’m discussing it today.

My regular readers know how much I appreciate REITs. Their propensity to offer safe and rising dividends can be a key ingredient in achieving a safe and enjoyable retirement.

However, they do take some getting used to since they deal almost exclusively with real estate. Their earnings are usually weighed down by non-cash depreciation costs that don’t reflect changes in asset value.

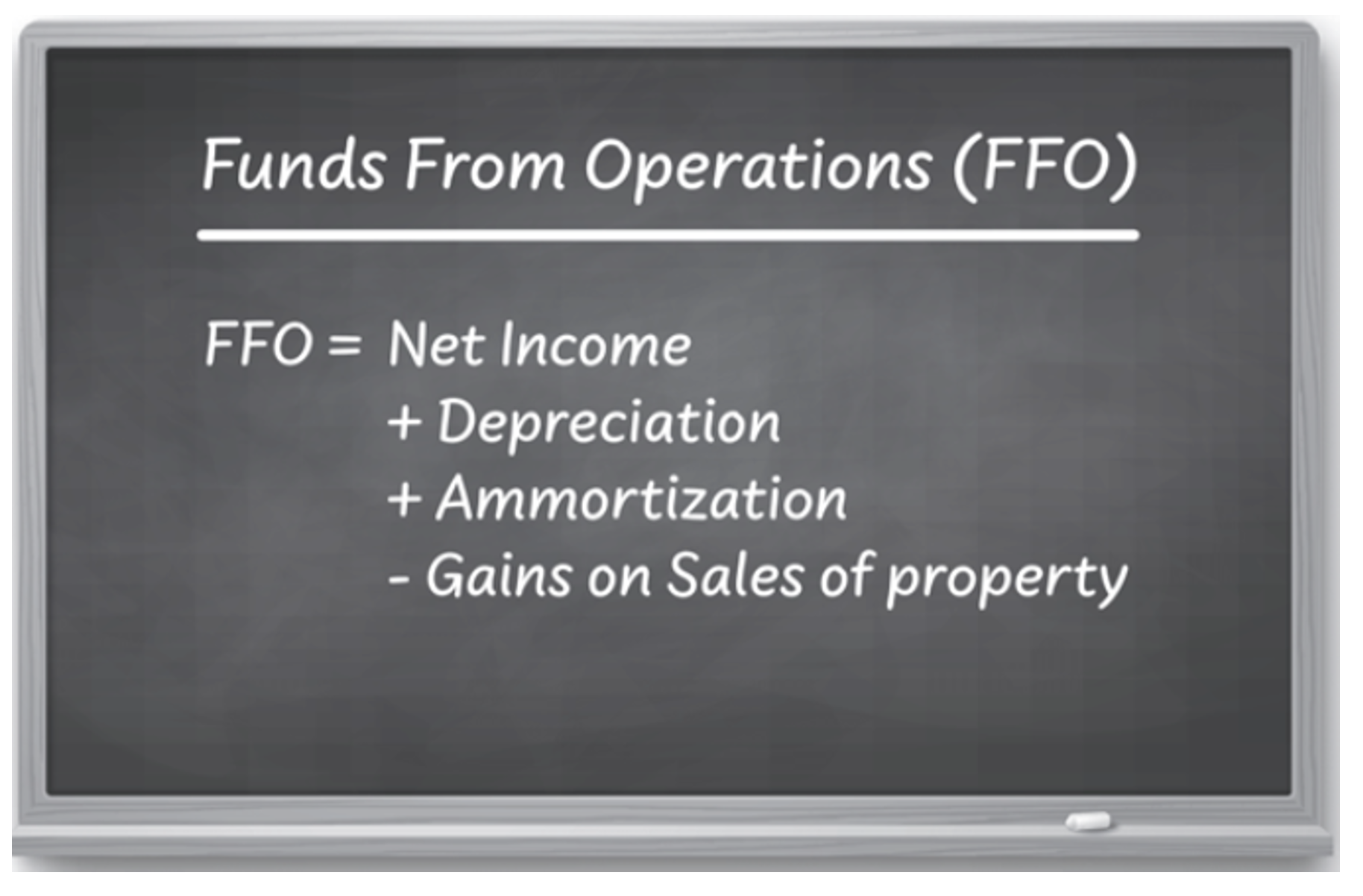

As such, the typical stock assessment, earnings per share (“EPS”), is of little value. So, the term “funds from operations,” or FFO, came into existence instead. It’s calculated as:

{kind=link}

Source: REITs for Dummies by Brad Thomas

When FFO was adopted by REIT advocate and educator Nareit in 1991, it quickly became the yardstick for REIT fundamental performance. However, while it was clearly better than EPS in determining free cash flow… it still wasn’t as accurate as it could be. That’s why analysts and some companies began to report adjusted funds from operations, or AFFO, instead.

It subtracts recurring capital expenditures (capex) from FFO, acknowledging that not all depreciation is non-cash in nature.

Think of it like this: Assume you’re a landlord, and you have to make some improvements to your property every time you sign a new lease. Stuff like changing the carpet and painting the walls.

These are capital expenditures, yet they’re not automatically taken into account in basic real estate reporting… even though they should be. AFFO fixes that problem, giving a more accurate idea of what’s really going on.

The Straight-Lining Truth

AFFO also takes care of how rental income is often “straight-lined” over the term of a lease according to generally accepted accounting practices (“GAAP”).

Let’s say your property has 2% rent increases every year for five years. By that final year, rent will be about 8.25% higher than it started out. Under GAAP, you even out this income across the life of the lease.

That might seem like a great idea in theory. But it ends up showing rents of just over 4% more than you really collected the first year.

This results in an accrued rent receivable that increases over the first half of the lease… and then declines in the second half. In so doing, there’s no acknowledgment of inflation: that a dollar of rent actually loses value as time goes on.

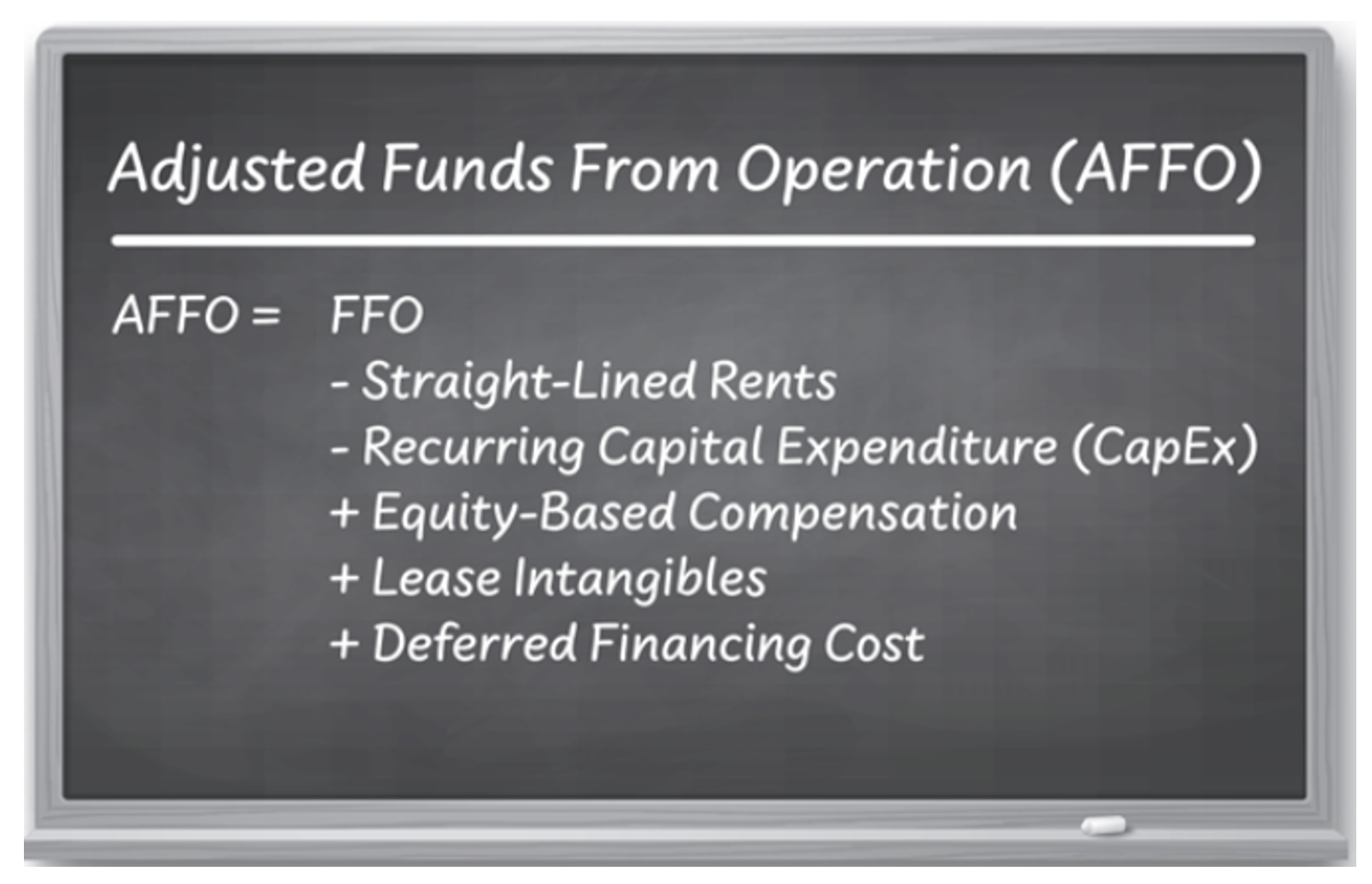

Straight-lining actually lowers FFO per-share growth. AFFO seeks to compensate for this with a calculation that often looks like this:

{kind=link}

Source: REITs for Dummies by Brad Thomas

Lease intangibles, for the record, are supposed to reflect the cost of finding new tenants. And deferred financing costs cover such things as bank and bond financing fees that were paid up front, then subject to non-cash expenses sometime later.

In such cases, there’s a clear recurring cash component as those certificates mature and are replaced.

AFFO: The Measure of REIT Champions

Assessing AFFO can, admittedly, get tricky since it’s not a universally defined term. As such, different REITs or real estate holders can interpret it differently, adding in other items at will if they believe it better reflects their recurring cash flows.

As a result, AFFO isn’t sanctioned by either Nareit or the Securities and Exchange Commission. And, honestly, I don’t know if it ever will be.

However, it’s still exceptionally helpful in determining what REITs are really working with – and what they can offer in terms of dividend hikes and valuation expansion. When it comes to choosing between FFO or AFFO for evaluation purposes, I choose AFFO almost every time it’s readily available.

Consider net-lease REITs, corporate landlords that let their tenants take care of property taxes, maintenance, and utilities. They have little to no recurring capex requirements. They also tend to have particularly long leases, which means straight-lined rents really mess up their FFO calculations.

That’s one very big reason why net-lease REITs like Realty Income (O) and Agree Realty (ADC) are much more likely to report AFFO in the first place compared with, say, office REITs. It’s also one very big reason why I like net-lease REITs so much compared with other REIT categories, offices included.

(Later this week, I’ll be writing an in-depth article on net-lease REITs. So, I’m glad you’re reading this AFFO primer.)

As I said back at the beginning, Wide Moat Research cares very much about evaluating companies’ true cash flows. And when it comes to REITs, it’s simple: AFFO takes more factors into consideration, giving us a better idea of what real estate owners and operators are really working with.

The more we know, the better our decision-making becomes, advancing our ability to make a profit. If you like the sound of that, give me an A… F… F… O!

Regards,

Brad Thomas

Editor, Wide Moat Research

|