You probably know about Blackstone (BX), the world’s largest alternative asset manager. The company has a reputation as the “king of private equity.”

And for good reason…

It boasts $1.2 trillion in assets under management (“AUM”) from a wide range of institutional and individual investors. Based in New York, Blackstone has offices and operations throughout the American continents, Europe, the Middle East, and the Asia-Pacific region.

And this all from $400,000 in seed money. That’s how much founders Stephen Schwarzman and Pete Peterson were working with back in 1985 when they established Blackstone.

The stock has also been a great one to own for years. Over the past decade, its annualized return has been north of 22%.

Blackstone’s stock has fallen out of favor in recent weeks for reasons I’m about to explain. But the drawdown has brought shares down to near-bargain levels for such a quality compounder. For value-oriented investors, it deserves to be on your radar.

Blackstone’s One-Two Punch

We’re not even two months into the year, and Blackstone has already had two big developments that hit the stock.

The first came when President Trump attacked institutional investors buying up single-family homes (“SFH”), then renting them out. He went so far as to propose a ban on larger investors buying these properties. And while revenue from Blackstone’s residential portfolio is pretty marginal, the news was still enough to send the stock lower about 6%.

I addressed that unexpected development exactly a month ago. At the time, I said these large investors were not the villains most people made them out to be. In many ways, they saved the day after the housing market crashed in 2008. From that article:

[By] 2010, a record of approximately 3 million homes were foreclosed on. And, given the dire straits of the economy, not many individual buyers were stepping up to claim them.

So institutional investors stepped into the mess by buying distressed single-family homes… at very attractive prices and renting them. Very often, they’d rent them back to the former owner who was still living there.

That housing carnage continued for years, prompting Blackstone to enter the market in 2012 through its affiliate, Invitation Homes – now an independent real estate investment trust (“REIT”) that trades under the ticker symbol INVH. Blackstone has since divested its position in that venture, but it remains a major player in the game.

So it does make some sense that it has taken a hit since Trump’s announcement that he was “immediately taking steps to ban large institutional investors from” the SFH stage – even though, to my knowledge, nothing concrete has come of that pledge so far.

Then came the second punch…

Earlier this month, artificial-intelligence (“AI”) startup Anthropic and OpenAI released their latest AI models on the same day. Those would be Claude Opus 4.6 and GPT-5.3 Codex. The new models go beyond just being “chatbots.” They’re explicitly designed to automate tasks typically done by enterprise software. The software stocks took a big hit as investors pondered if these businesses were in the early innings of being disrupted.

Blackstone is not a software company. But private credit is a large part of its business. And as Stephen Hester wrote in yesterday’s edition of Intelligent Options Advisor:

In short, investors are worried that the growth story for many Software as a Service (“SaaS”) companies is over. These companies aren’t going bankrupt overnight, but they could be under pressure if new AI tools disrupt their business models.

This fear has bled over into the firms that lend to these companies. After all, enterprise software is typically 15% to 25% of every diversified private-credit portfolio. That’s the thinking, anyway.

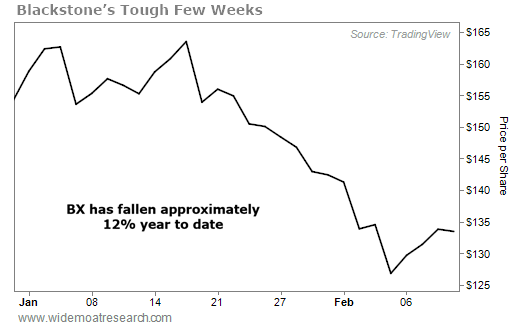

The result is that BX is down about 12% year to date. And it’s down about 30% from its 52-week high.

{kind=link}

But, as they say, if you come at the king, you’d best not miss. And, to me, Blackstone still looks like the king… one with a tantalizingly cheap price tag.

Taking a Closer Look at the King

Like most asset managers, Blackstone doesn’t limit itself to just one department, operating in business segments such as:

-

Real estate, where it’s a global leader with $319 billion of AUM across the world

-

Private equity, with $416 billion of total AUM

-

Credit and insurance at $443 billion

-

Multi-asset investing, with $96 billion in AUM – making it the world’s largest discretionary allocator to hedge funds

I’ve been covering this asset manager for over a decade. Back in 2014, I wrote on Seeking Alpha how, “I’m keenly aware of the growth behind this powerful private equity firm, and I consider [its] more recent track record to be very attractive.” Sure enough, shares have returned over 618% since that article was published, compared with 270% for the S&P 500.

In the fourth quarter of 2025, Blackstone posted solid results with AUM increasing 13% year over year, outpacing quarter three’s 12% growth. Inflows were stronger, too, a sign that investors are confident in the company’s business model.

And it recorded an 11% boost to fee-earning AUM, another jump from quarter three’s 10% increase.

Generally accepted accounting principles (“GAAP”) net income was $2 billion. Plus, distributable earnings (“DE”) were $2.2 billion, or $1.75 per common share, resulting in a $1.49 dividend.

These were Blackstone’s best results ever.

For the year, DE increased 20% to $7.1 billion, or $5.57 per share. This was powered by strong growth in fee-related earnings and a significant acceleration in net realizations.

In a recent Wide Moat Daily article, I presented Blackstone as a good way to access the data-center sector. After all, the company owns QTS Realty – an enormous global data-center player – and is a major investor in the modernization and growth of the U.S. electric grid through Blackstone Energy Partners.

And with its fortress balance sheet, complete with $198.3 billion in investable cash… Schwarzman was completely right to declare “that Blackstone is more than ready to capitalize on any major opportunities that come up.”

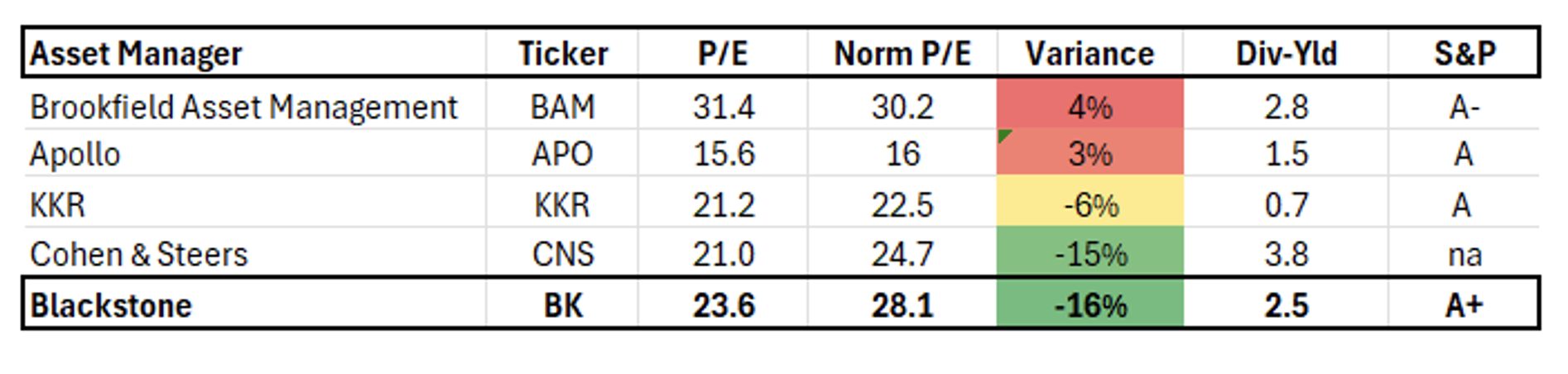

Yet shares are trading at around $135, with a price-to-earnings (P/E) ratio of 23.6 times and a 2.5% dividend yield. That makes Blackstone one of the cheapest big-name asset managers around based on the spread between its current and normal multiples, as shown below.

{kind=link}

Source: Wide Moat Research

It’s hard not to see good things ahead for Blackstone… and its investors who believe today’s bad PR doesn’t define its future.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|