Insurance companies are not the most popular businesses in the public eye these days.

That’s understandable, considering how much money we give them every year between health insurance, car insurance, and home or renters’ insurance.

There’s also liability, long-term care, and life insurance for those interested. It all adds up.

The Hill reported late last year that an average family’s health plan now costs close to $27,000 per year. Fortunately for them, employers tend to cover most of that for full-timers, who only end up shelling out $6,850.

So, it could be worse.

Then again, it could be better considering how that $27,000 annual price tag has risen three years in a row now. And as The Hill stated, “Family premiums are up [6%], or $1,408, from” 2025. That was “more than double the rate of inflation and similar to the [7%] increase in each of the previous two years.”

Car insurance, meanwhile, increased 55% between February 2020 and October 2025. Today, it sits at a national annual average of $2,524, or $210 per month, after rising repeatedly these past few years. And home insurance runs at $2,966 per year, or approximately $247 per month, a 46% hike since 2021.

That’s quite the chunk of change for a family of four living in their own house with two vehicles.

Add to that the perception – real or imagined – that insurance companies employ a “delay, deny, defend” strategy when handling customer claims. In short, many people accuse them of regularly weaseling out of their obligations.

That’s such a common complaint, in fact, that a whole other industry opened to act as the middleman and advisor when dealing with insurance companies.

And it’s that industry I’m turning to today for reliable “refunds.”

Your Insurance Against Insurance

Welcome to the world of insurance brokerage and risk management.

If you own a business or work for a government-affiliated organization, you might have already heard of it. But most individuals – unless they’re very well off – go through their lives utterly unaware this field exists.

That’s a shame, considering the attractive investment possibilities it can hold.

Nick Ward and I discussed this topic earlier today on The Wide Moat Show on YouTube. And I highly recommend you check it out. While there is some overlapping information between it and what you’re reading now, both have unique aspects I don’t want you to miss.

For instance, there are two other portfolio possibilities Nick and I bring up in the show. Whereas I can explain the actual insurance brokerage and risk management business model better here.

Again, this isn’t the actual insurance industry we’re talking about. This one seeks to find the best insurance policies possible for customers by:

-

Understanding the business or estate in question from top to bottom, inside and out, to know their coverage needs

-

Evaluating the options available for that business or individual to determine which one is best suited for them

-

Negotiating better deals when necessary

And when something does go wrong that insurance should cover, these brokers and risk managers step in to make sure everything goes about as smoothly as it possibly can.

This can all save a company 10%, 20%, or even 40% on annual insurance expenses, more than making up for the price of hiring such mediators to begin with. If anything, they’re becoming more attractive than ever due to rising coverage costs.

Brown & Brown: The Insurance Troubleshooter

That’s just one of the reasons why I like the looks of Brown & Brown (BRO) right now.

While not an insurer itself, Brown does sell insurance policies that it earns commissions and fees from. This is true for both new customers and renewals, which gives it an attractive recurring revenue model.

And this comes part and parcel with no underwriting exposure and therefore minimal balance sheet risk. Brown has a BBB- credit rating from S&P that gives it a lower cost of capital it puts to good use.

The company is very good at growing by rolling up smaller insurance agencies.

Case in point, Brown announced in February that it acquired The Protectorate Group Insurance Agency (which does business as American Adventure Insurance). The new purchase specializes in dealerships for motor homes, travel trailers, campers, boats, watercrafts, and motorcycles.

Last August, Brown completed the purchase of RSC Topco, the holding company for Accession Risk Management Group. And other recent acquisitions include:

-

The Protectorate Group Insurance Agency (e.g., American Adventure Insurance), which focuses on RV and marine dealership coverage

-

Kevin Campbell Agency in the retail space

-

The highly specialized MGA Pardus Underwriting Limited

-

All Medical Professionals Limited, with its obvious healthcare focus

-

U.K. private-client and bloodstock broker Weatherbys Hamilton

All told, Brown & Brown has made more than 600 acquisitions since the 1990s – all of which it has masterfully integrated into its existing system to drive cross-sell and operating leverage alike.

During the first quarter of 2026, the company delivered solid cash flow of over $260 million… an approximate $50 million, or 23%, increase over the first quarter of 2025. Management said it “anticipates good cash generation for the remainder of the year and will balance the deployment of capital between share repurchases, [mergers and acquisitions], dividends, and deleveraging.”

Brown is also a Dividend Aristocrat, having achieved 32 consecutive years of dividend growth. And since it keeps its payout ratio in the low- to mid-teens, it retains plenty of room to continue growing the dividend by around 10% annually.

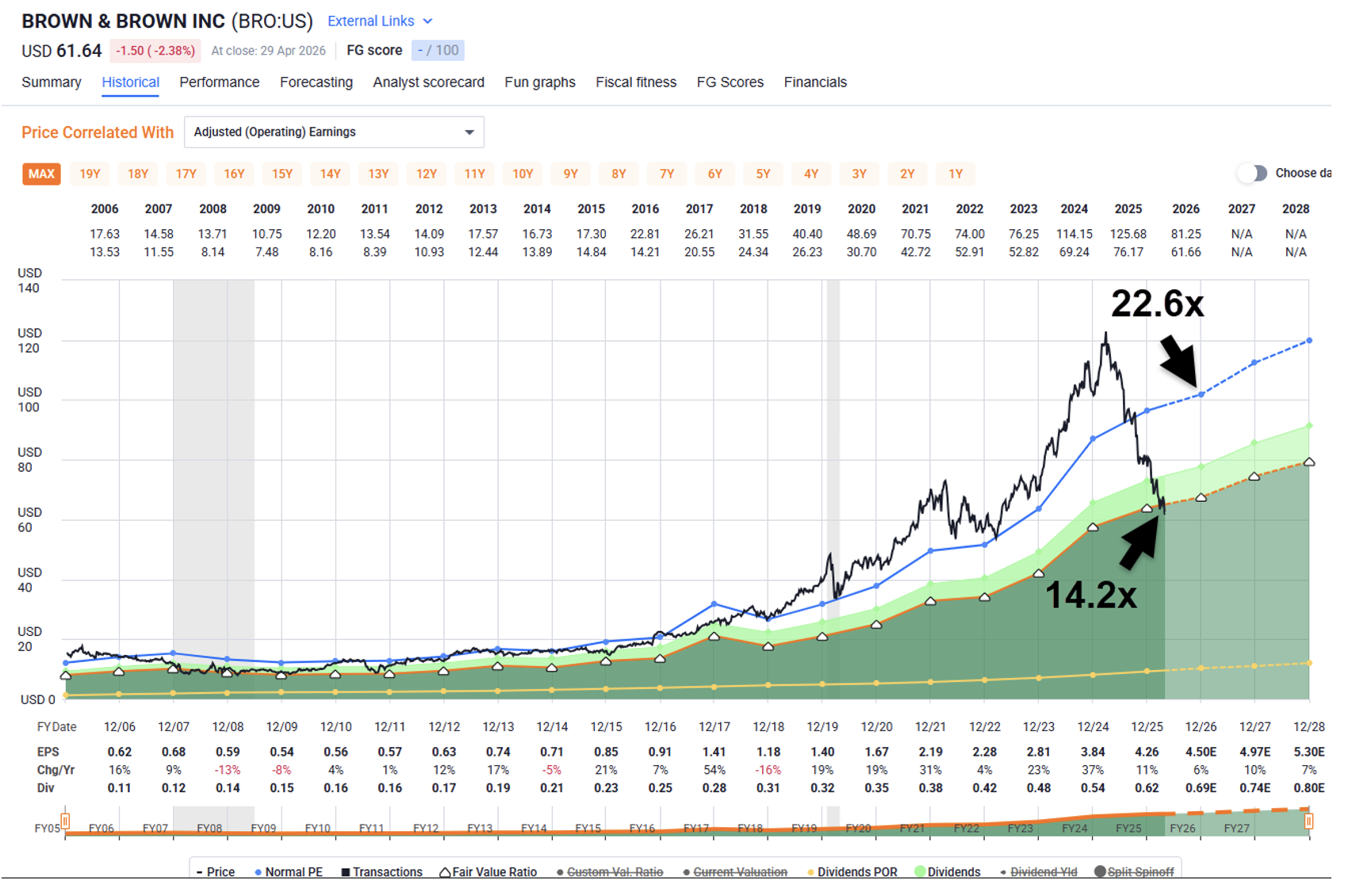

Yet the company is trading at a bargain. The stock’s current price-to-earnings (P/E) ratio is 14.2 times, far lower than its normal multiple of 22.6 times and even further below the high of about 29 times it reached in 2024.

Analysts expect 6% growth this year and 10% growth in 2027. And while its 1% dividend yield is admittedly modest, our 12-month total return forecast is 25%.

As such, Wide Moat Research puts Brown & Brown solidly in our Strong Buy category.

{kind=link}

Source: FAST Graphs

Regards,

Brad Thomas

Editor, Wide Moat Daily

|