I was at my local cafe, Spill the Beans, with a friend recently as he shared some interesting news.

His company is expanding its private equity platform by franchising multiple 7 Brew Coffee locations across the Southeast – a move he was excited about, and with good reason.

{kind=link}

Source: Brad Thomas (East Main Street in Spartanburg SC)

This fast-growing chain features:

-

A long list of tasty, customizable drink choices

-

A fast, efficient drive-thru-only setup that still utilizes friendly face-to-face service

-

Good value for larger cup sizes.

That last factor is a big deal these days considering rapidly rising gas prices… on top of the inflation we’ve already been experiencing for years. People still want their high-brow coffee. Make no mistake of that.

But they want it at prices that don’t break the bank.

That’s why Starbucks (SBUX) CEO Brian Niccol made such a row last week when he went on The Wall Street Journal’s What’s News AM podcast. Talking up the chain’s average price for a cup of coffee, he declared:

What we’re seeing is people, you know, they want to have a special experience. And regardless of what your income level is, a $9 experience does feel like you’re splurging.

… what that means is we have to make it worthwhile, right? And then in other cases, people believe, “Well this is a really affordable premium experience.” Because they’re saying, like, “Well, it’s less than $10 and I get a really premium experience.”

It didn’t take long for people to lambast Niccol as “arrogant,” “elitest,” and “out of touch.” Some even went so far as to call for a boycott.

But before you sell the stock on that negative news, really consider Starbucks’ economic “moat.” If its past, present, and future projections are any indication…

I’d say it’s still more than wide enough to keep the competition at bay.

The Coffee Wars Are Heating Up

Starbucks has been the world’s undisputed coffee destination for decades now – putting plenty of smaller operations out of business along the way.

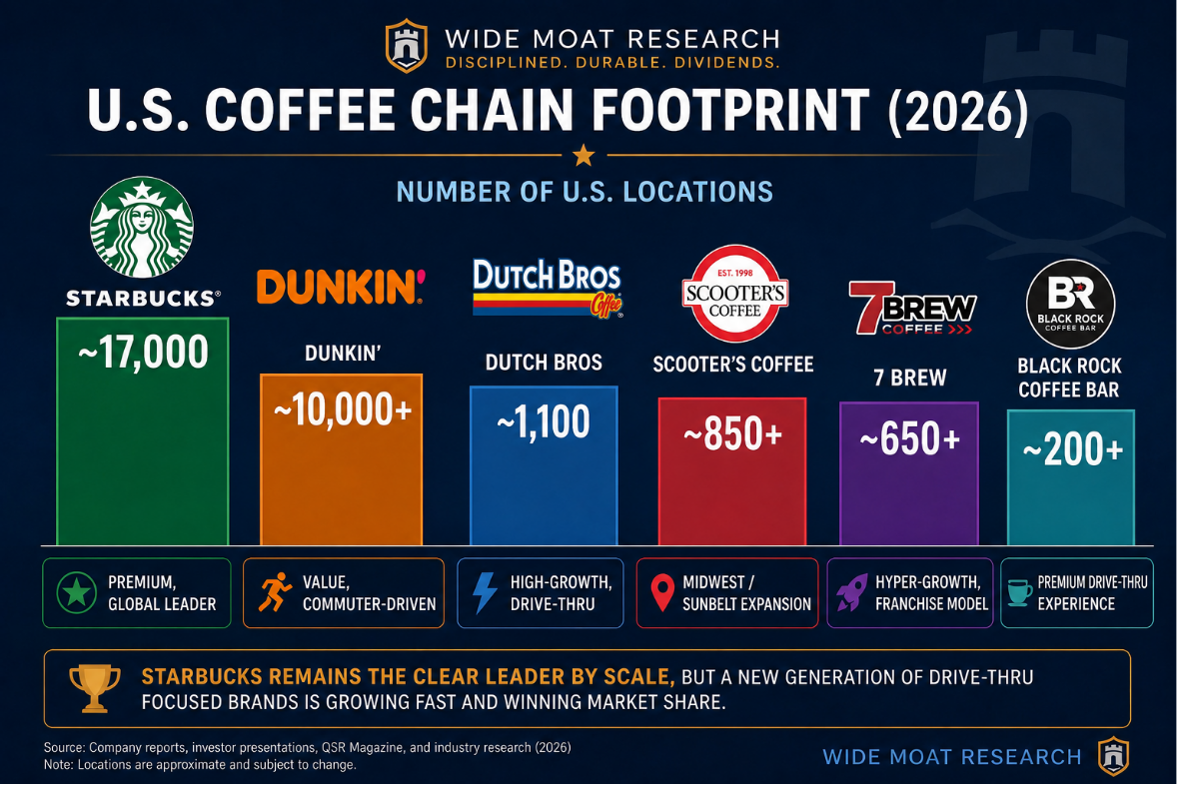

With roughly 17,000 locations across the U.S. and more than 40,000 worldwide, nobody ever questioned its moat in the past. Its fortress-like brand was rooted in customer experience, trendy appeal, convenience, and consistency.

Now, it’s obvious that the coffee landscape is changing, in large part thanks to life’s rising unaffordability. As such, today’s emerging coffee shops aren’t trying to be the next Starbucks…

They’re trying to declare it irrelevant.

One such up-and-comer is Dutch Bros (BROS), which now has over 1,100 locations and a cult-like following among younger consumers. Its drive-thru-first model delivers hard-to-beat efficiency and stronger unit economics than most legacy café formats can manage.

Black Rock Coffee Bar (BRCB), meanwhile, is small but scrappy as it expands across the Sunbelt and Western U.S. It’s extremely community driven while still offering a sleek and modern store experience that stands out from the traditional coffeehouse aura.

As for the previously mentioned 7 Brew, its 650 locations stand out for their simplicity. These smaller buildings are cheaper to build and maintain, which is part of how they can offer the affordable beverages they do.

I also want to mention the privately owned Scooter’s, which has about 850 locations – and counting – across the Midwest and Sunbelt markets especially. Scooter’s might not have the flashiest growth story, but its disciplined, franchise-based expansion strategy is working well nonetheless.

Of course, none of them can compete with Munchkins-craving consumers who can’t get enough of Dunkin’ Donuts. No list of Starbucks competitors can be complete without mentioning that old-timer, which first opened in 1950.

With approximately 14,000 locations worldwide – 10,000 in the U.S. alone – it’s held its own with value-oriented pricing, fast service and, of course, donuts.

{kind=link}

Source: Wide Moat Research

It’s hard to think of Dunkin’ Donuts fading away, even with the rise of newer, hipper competitors. Again, it’s in a space of its own.

But some investors have grown more skeptical about Starbucks’ prospects against so many upstart challengers. There’s no ignoring how coffee consumption trends are shifting toward drive-thru convenience, faster service, and digital integration, these critics point out.

Yet it’s just as true that Starbucks isn’t lying down in the face of these changes and waiting to die.

Not even close.

Starbucks’ First-Mover Advantage

Starbucks has actually been investing heavily in store upgrades, barista training, and operational improvements under the aforementioned Brian Niccol’s guidance.

He was specifically brought on as CEO in September 2024 to win back customers the company had been steadily losing. And despite last week’s unfortunate interview, he seems to be succeeding.

I’m not trying to downplay his hard work when I say that I’m not surprised at the turnaround. It’s just that when it comes to high-brow coffee, Starbucks has a powerful first-mover advantage.

Al Ries and Jack Trout break this concept down in their book, Immutable Laws of Marketing, where they write that “the leading brand in any category is almost always the first brand into the prospect’s mind.” This is simply:

… the law of leadership. It’s better to be first than it is to be better. It’s much easier to get into the mind first than to try to convince someone you have a better product than the one that did get there first.

In which case, Starbucks has an almost unbeatable edge. I would even say the only coffee shop that can truly bring it down is itself.

Back in its undisputed heyday, Starbucks wasn’t just a retailer. It was a ritual. Even a religion. Its brand loyalty was unbeatable…

Until it started taking its customers for granted with poor service, lackluster presentation, and sloppy execution.

Niccol has since been working hard to fix its weak spots. He’s strengthened the company’s marketing, cleaned up some stores, shut down others, and expanded elsewhere into more promising markets.

Starbucks isn’t shrinking; it’s growing its presence, with hundreds of new locations planned for both the U.S. and worldwide in 2026. And it already delivered strong results this past quarter that beat out expectations:

-

Global same-store sales were up 6.2%.

-

U.S. same-store sales rose 7.1%.

-

Revenue increased 9% to $9.5 billion.

-

Profits were up 33% to $510.9 million.

Moreover, Starbucks raised its full-year guidance to between $2.25 and $2.45, a sign of continuing confidence in its comeback efforts.

So no, I can’t say I’m all that concerned about Starbucks as a company. It’s in comeback mode, and I wouldn’t bet against it.

Then again, I also wouldn’t bet on it by buying shares at today’s prices.

SBUX features a relatively expensive price-to-earnings (P/E) multiple of 46.7x with a 2.3% dividend yield. Whereas, historically, it’s traded at around 30.4x.

And prior to COVID, that figure was even lower at around 27x.

This stock needs to take a significant dip before I’d recommend it. But for those who like a good wide-moat play (like we definitely do), feel free to put this coffee king on your watchlist.

And if you get to Spartanburg in the meantime, drop me a message. Coffee can be on me!

Regards,

Brad Thomas

Editor, The Wide Moat Daily

|