It finally happened yesterday morning.

Alexandria Real Estate Equities (ARE), a life-science-specific real estate investment trust (“REIT”), cut its dividend.

By a lot.

As PR Newswire put it, the company:

… announced that its board of directors declared a quarterly cash dividend of $0.72 per common share for the fourth quarter of 2025, representing a 45% reduction from the dividend declared for the third quarter…

This kind of action can be due to poor, complicated, or even occasionally corrupt management.

But it can also be circumstantial.

During the COVID-19 crisis, for instance, many REITs saw their properties shut down for months or more. The companies (understandably) had to cut the dividend.

I think the recent cut from Alexandria would fall into this latter category. As I’ve shared on numerous occasions, I have a high opinion of management. But the company has been dealing with dynamics in its property sector that were wholly unpredictable.

And so, today, we’ll consider if – with this bad news out of the way – shares have finally reached a turning point.

How Alexandria Real Estate Fell This Far

Alexandria Real Estate was founded three decades ago during the biotechnology revolution of the 1990s. Medical advancements were all the rage back then, making them must-have investments.

But Alexandria decided to capitalize on the craze in a particularly unique way – by building specialized facilities for biotech and pharmaceutical companies to operate in.

I last covered the company on November 3, writing how this:

… was something nobody had done before. But Alexandria did it so well, it was able to go public just three years later. And for a long time, it was an incredible stock to hold.

Between 1997 and late 2021, it returned more than 2,800%, or about 15% annualized. Big-name companies like Merck, Eli Lilly, AstraZeneca, Johnson & Johnson, and Novartis trust it to provide the unique working spaces they require to advance their research, including labs and attached offices.

Altogether, Alexandria boasts 700 tenants and a 39.1 million square-foot portfolio, with another 4.2 million square feet under current construction. These mission-critical facilities are located in medical research hotspots such as:

-

Seattle

-

The San Francisco Bay area

-

San Diego

-

The greater Boston area

-

New York City

-

Maryland

-

The Research Triangle in North Carolina

But then, COVID-19 came along…

At first glance, you might think that would bode well for a company like Alexandria. It spurred even more demand for life-science exploration. While tenants and investors alike were running away from other REITs, the collective determination to end the pandemic made the life-science situation outright manic.

Markets always respond to demand. And the demand for life sciences buildings at the time could be summed up in one word – more!

But, as always happens, this sector got over its skis. The industry overbuilt. And as the urgency of the pandemic receded, we were left with one heck of a supply glut.

As I wrote last month:

… nearly half the lab space completed between 2022 and 2024 remains empty today.

Even the most responsible life-science landlords have suffered as a result of that kind of foolishness. And it shows in [Alexandria’s] stock price. From its peak, the stock is down 74%.

So, no, this life-science landlord isn’t operating in its ideal economic environment right now. That’s why I flat-out predicted:

With earnings slowing down, ARE will evaluate its dividend in 2026 to remain aligned with per-share FFO and maintain capital for core operations. Here at Wide Moat Research, we estimate a 35% dividend cut would preserve the REIT’s $315 million in annual cash flow.

We now know that management decided to be even more conservative, slashing their payout by 45%. And the stock is down by about 13.7% since yesterday’s open.

But does that make Alexandria an even more attractive value proposition? We need more details to sort through this bargain bin.

The 2026 Picture Looks Unimpressive for Alexandria

In the past, we’ve argued here at Wide Moat Research that Alexandria enjoyed “moat like” attributes such as:

- A healthy balance sheet (BBB+/Baa1 ratings from S&P and Moody’s)

- Critical scale advantage

- Long-tenured management team

- Reliable earnings and dividend growth

However, ongoing challenges have narrowed that moat rating.

Over the past 20 years, ARE has featured an average occupancy of 93.5%. But that figure fell to 90.6% in the third quarter of 2025 and will likely decline to around 88.5% by the fourth quarter of 2026… even after accounting for over 2% of properties that may be sold.

We also have to consider slower development leasing, with a 39% reduction in annual construction spending. Then there’s higher capital expenditure (capex) needs, with $2.9 billion of expected non-core asset sales in 2026.

Likewise, ARE’s elevated vacancy will drive higher leasing costs, since new leases are more expensive than renewals. And this will further eat into its adjusted funds from operations, or AFFO (see my recent article on AFFO here).

On its recent investor day, Alexandria noted that revenue and non-revenue-enhancing capex will go up quite a bit. For the past five years, it has averaged 17% for revenue/non-revenue-enhancing capex.

For 2026, that will shoot up to 27% to 32%. Around 55% of this is associated with upcoming vacancies at sizable assets. For instance, Alphabet’s (GOOG) life-science company, Verily, will be vacating its space in San Francisco, and another large property is going dark in Cambridge next year.

ARE has therefore announced 2026 FFO guidance of $6.25 to $6.55, which represents a 29% reduction at the midpoint.

{kind=link}

Source: Wide Moat Research

That’s why it had to slash its dividend so severely. By doing so, it conserves $410 million of capital.

Bargain or Junk: A Deeper Dive Is Needed

Alexandria has some other tools in its arsenal to regain shareholder value. This includes lowering construction spending, buying back shares on the cheap, and continuing to reduce general and administrative (G&A) costs – where it plans to save compared with 2024.

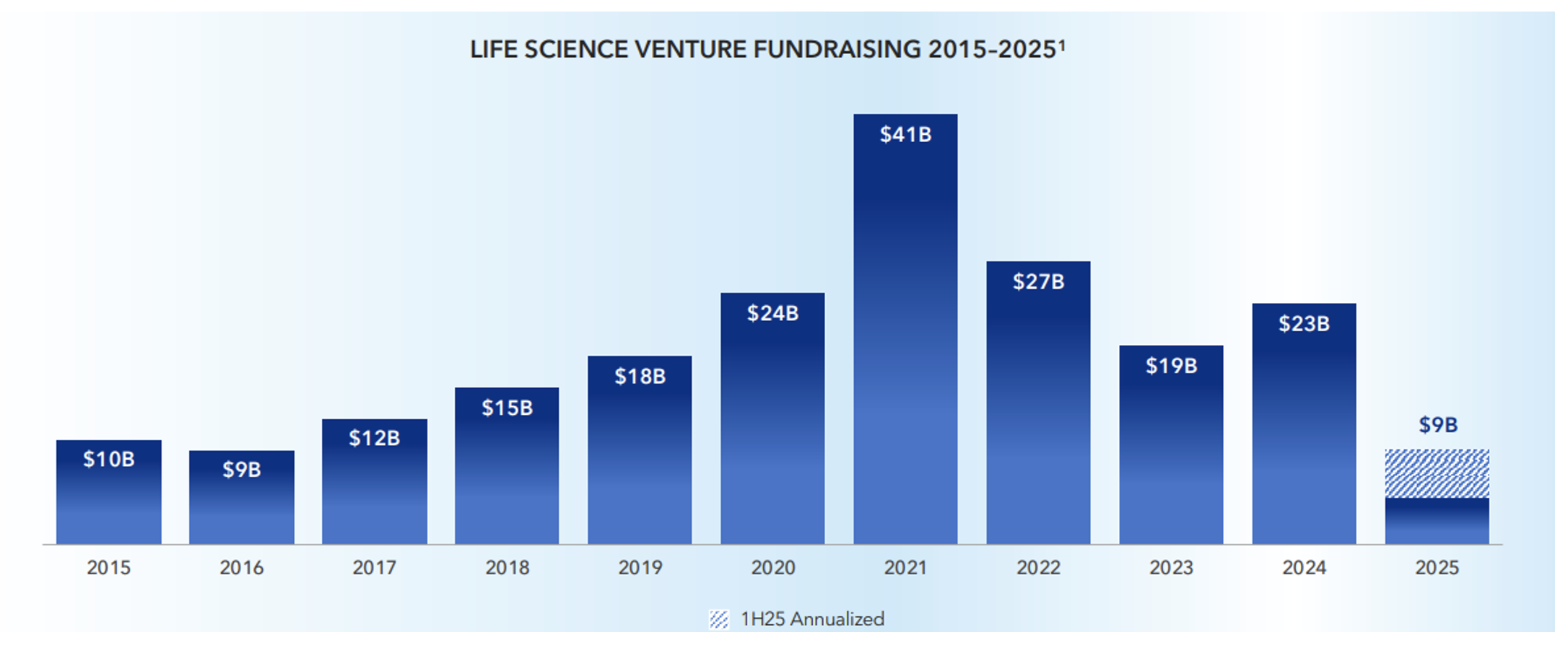

Then again, there are catalysts it can’t control, such as the recovery in capital formation for early-stage life science companies.

As viewed below, life science venture capital (“VC”) fundraising is at its lowest level since 2016.

{kind=link}

Source: ARE Investor Day Presentation

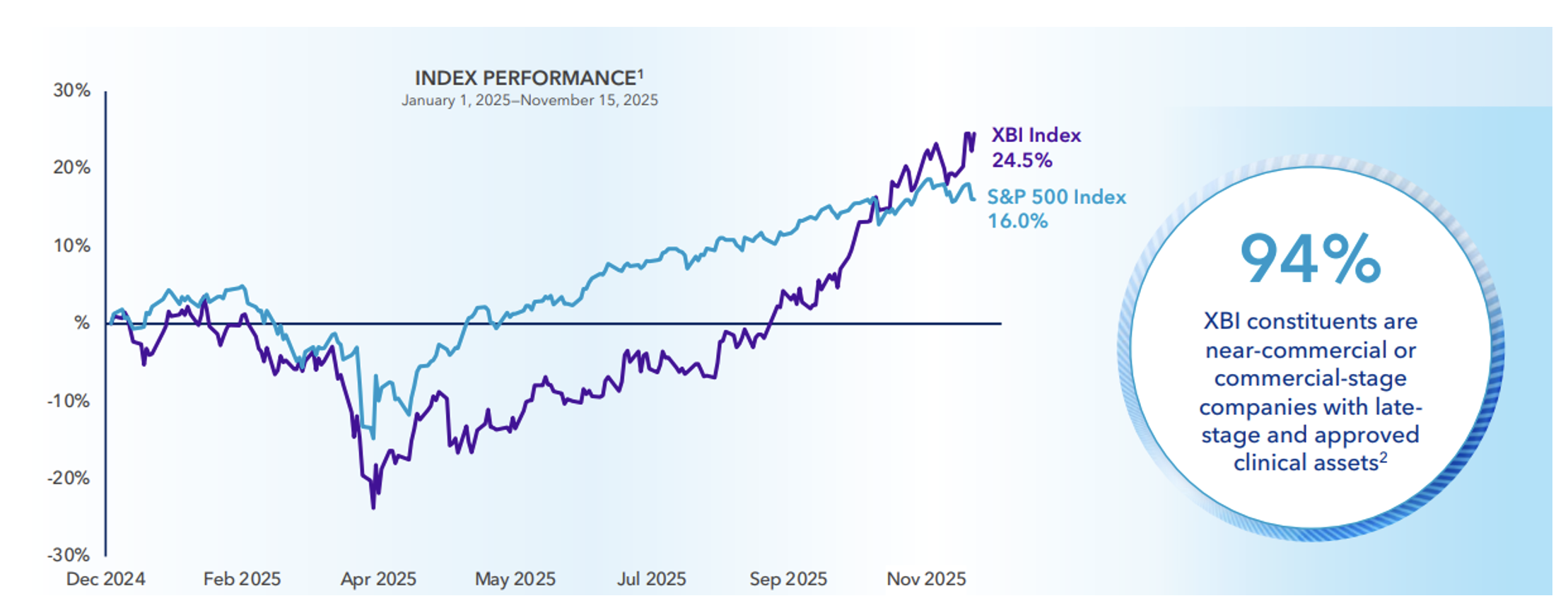

On the plus side, there is an increase in biotech interest, complete with renewed IPO activity. And that kind of growth demands more lab space.

{kind=link}

Source: ARE Investor Day Presentation

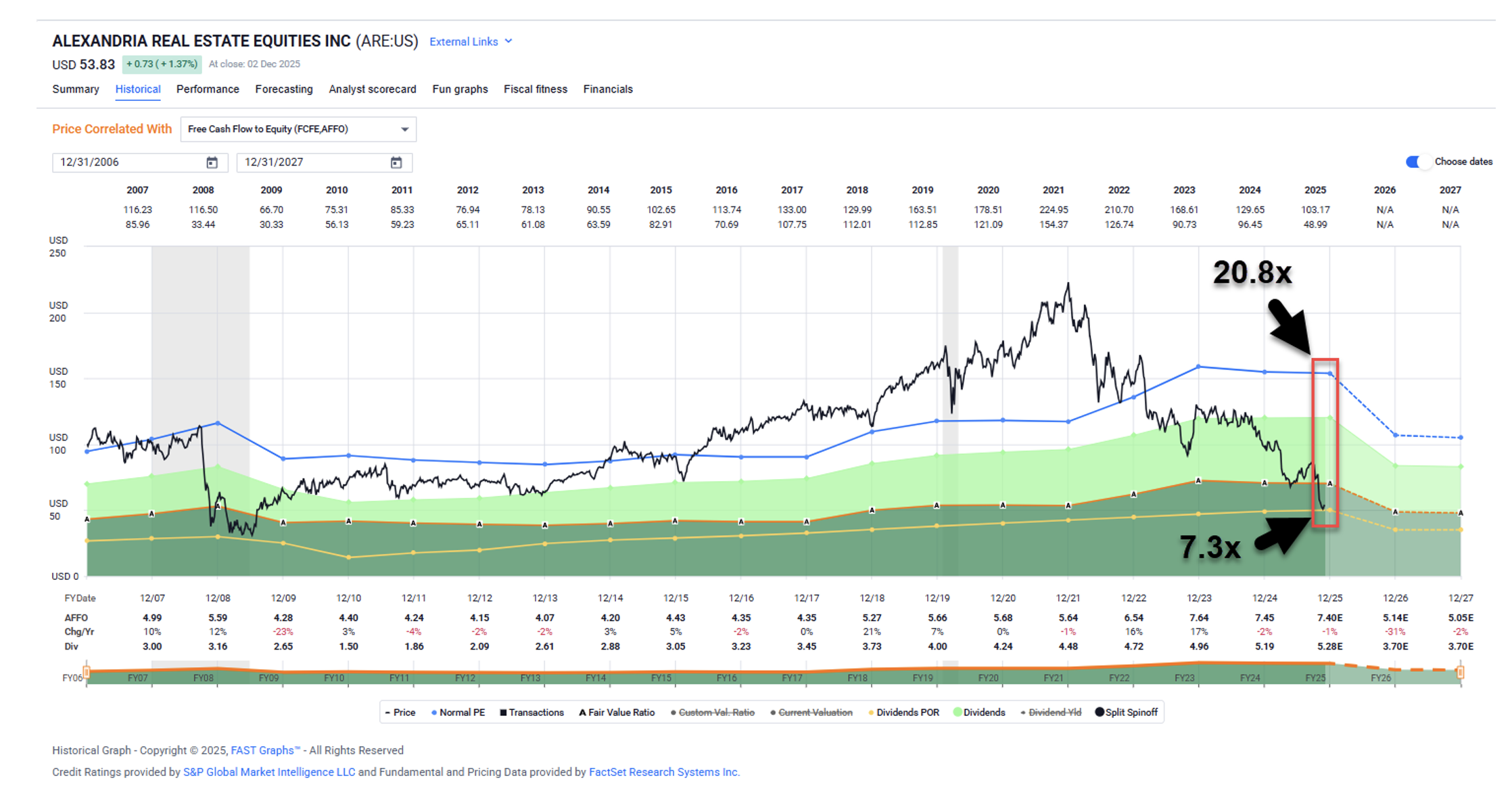

So is ARE’s stock price in bargain territory?

As shown below, ARE is trading at a multiple of 7.3 times compared with its normal P/AFFO of 20.8 times. The REIT hasn’t traded this low since the Global Financial Crisis.

{kind=link}

Source: FAST Graphs

We have to also consider that how interest rates are coming down (though perhaps not this month). That supports VC interest and, in turn, serves as a catalyst for development leasing and improved profit margins at ARE.

From a value investor’s lens, one could argue that ARE is a clear bargain since it’s trading at a 50% discount to its intrinsic value. Still, its fundamentals have certainly become weaker, as evidenced by the latest dividend cut news. And there is a chance that ARE could be removed from the S&P 500 as a result.

It’s a tough call to make, which is why I plan to interview Alexandria CEO Joel Marcus on Monday. Wide Moat Letter subscribers will have access to that full transcript next week…

Along with my final decision on whether this is a bargain of a lifetime or not.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|