As I explained in Monday’s edition of Wide Moat Daily, rate cuts are now inevitable. And it’s not because inflation is down.

In fact, consumer inflation is still on the warmer side, as we learned this morning.

According to the latest reading of the Consumer Price Index (“CPI”), overall consumer prices rose 2.9% from August 2024 to August 2025. That would make it the highest reading so far this year. Core inflation – which strips out the volatile food and energy segments – rose 3.1%.

However, both readings were in line with expectations. And I doubt it will change the Federal Reserve’s course of action on rates. The market agrees. At last check, the futures markets were implying a 90% chance of a quarter-point cut this month.

Remember the Fed has a dual mandate:

-

Maximum employment

-

Price stability (control inflation)

Since late 2021, the Fed has mostly focused on No. 2 by raising its key rate. And even though inflation is still hanging around, it really needs to shift gears and focus on No. 1.

That’s because the labor market is getting worse.

It has been bad for even longer than we realized. The annual number of jobs gained through March 2025 likely has to be revised down by a mind-boggling 911,000 positions.

All told, we have to come to terms with the dreaded economic S-word: Stagflation. If you lived through the 1970s, you already know what that is – stagnant growth, sticky inflation.

That’s why I’m so focused on quality real estate investment trusts (“REITs”) right now. They offer protection against both slow business growth and rising prices at the same time.

Many REITs have annual “escalators” built into their leasing contracts. That simply means they get paid more rental income each year. As a result, their dividend payments also tend to rise annually.

Better still, they should offer attractive share price appreciation now that the Fed is practically forced to lower rates.

So far this week, I’ve discussed REITs in sectors such as farmland, ground-lease, and health care. But there’s one specific property type that should perform best in this declining rate environment.

By that, I mean net-lease REITs: companies that invest in free-standing or stand-alone buildings under triple-net leases. As I explain in my book REITs for Dummies, “Net-lease refers to a rental situation where the renter pays for some or all of a property’s taxes, insurance, and maintenance.”

Instead of dealing with aggravations related to taxes, toilets, or tenants – what I call the “three Ts” – these landlords can sit back and collect the rent without the headaches that usually comes from being a landlord.

In most cases, net-lease contracts are signed for 10, 15, or even 20 years with options to renew. As mentioned, they also include rental increases, which provide the landlord with a high degree of predictability concerning future cash flows.

This steady stream of rental income is one of the primary attractions to the property sector… for both owners and investors alike.

A Deeper Dive Into Net-Lease REITs

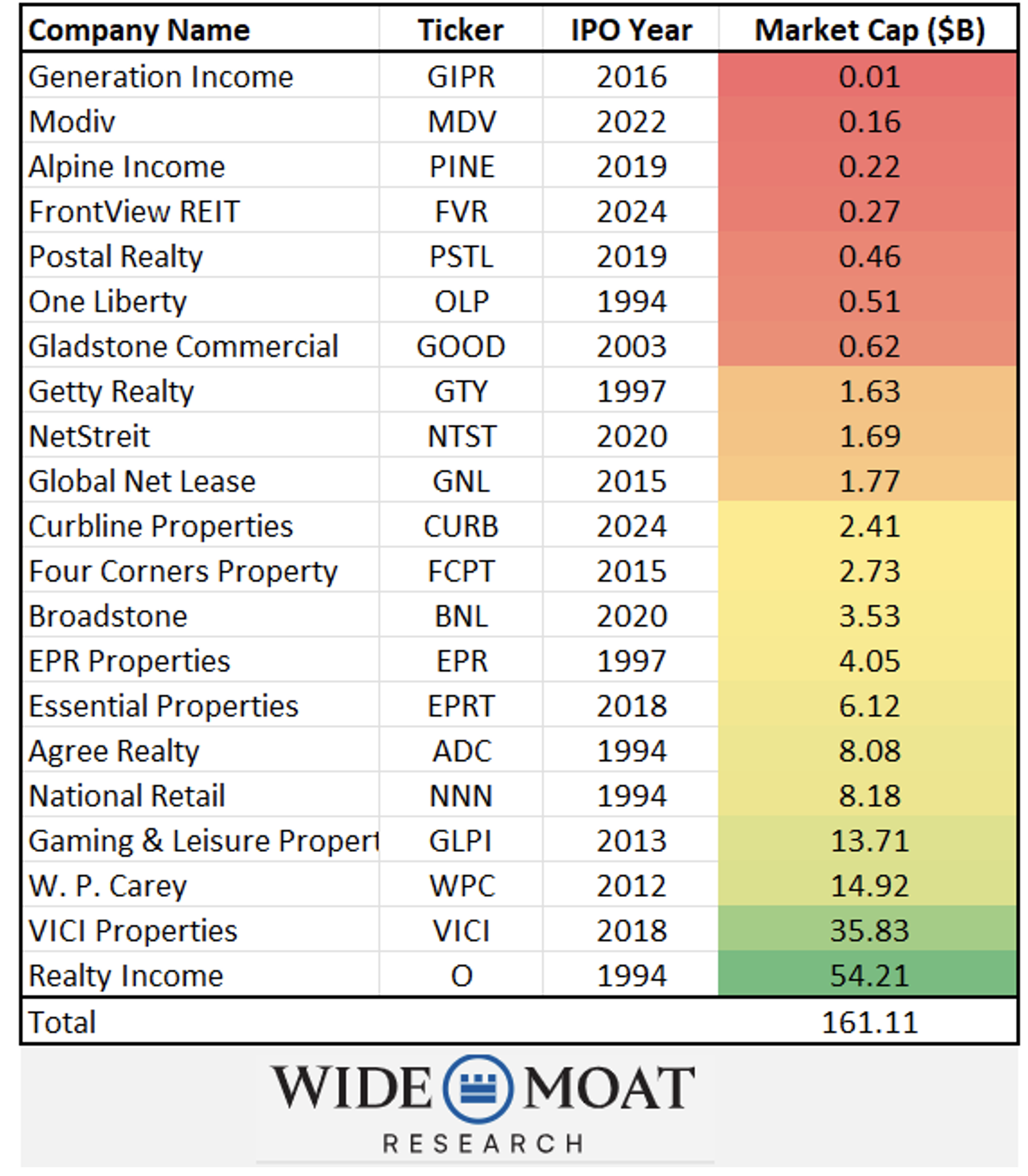

There are 21 publicly traded net-lease REITs in the U.S. They range from the nano-cap Generation Income Properties (GIPR) to the gigantic Realty Income (O).

{kind=link}

So far this year, the sector has returned around 15% compared with the entire equity REIT universe’s 2.1%. High-quality triple-net REITs like Realty Income have shined. O has returned about 17% year to date, beating the S&P 500 at around 12.5%.

However, when you widen your scope to consider its performance over the past two years, it’s clear…

Due to higher costs of capital from higher interest rates, these free-standing landlords have struggled.

That will change though just as soon as the Fed gets serious about cutting rates – as I imagine they are now. After all, a declining interest rate environment improves sentiment and actively strengthens the fundamentals that drive performance, and lowers borrowing costs.

At the same time, inflation will keep property values rising, adding even more value to the net-lease REIT structure. The result is that they become the “prettiest girl in the room,” especially compared with bonds as yields compress.

And that allows them to take their rightful place as one of the most compelling options for income-focused investors.

I focused on net-lease REITs in today’s YouTube show as well, calling it the “Nothing but Net-Lease Masterclass.” In it, I break down all 21 net-lease REITs into three categories:

-

REITs to avoid

-

REITs to consider

-

My "Fab 5" net-lease REITs

I hope you’ll take the time to watch the entire episode. We’re adding about a thousand new followers per week, and I’m sure you’ll see why.

In the meantime, let’s discuss my top two picks below…

An Essential Net-Lease REIT

Essential Properties Realty Trust (EPRT) is a net-lease REIT that owns 2,190 properties amounting to 23.6 million square feet. Spread across 48 states, its tenants include:

-

Restaurants (quick service, casual, and family dining)

-

Car washes

-

Automobile services

-

Medical services

-

Convenience stores

-

Entertainment venues

-

Health and fitness facilities

-

Early childhood centers

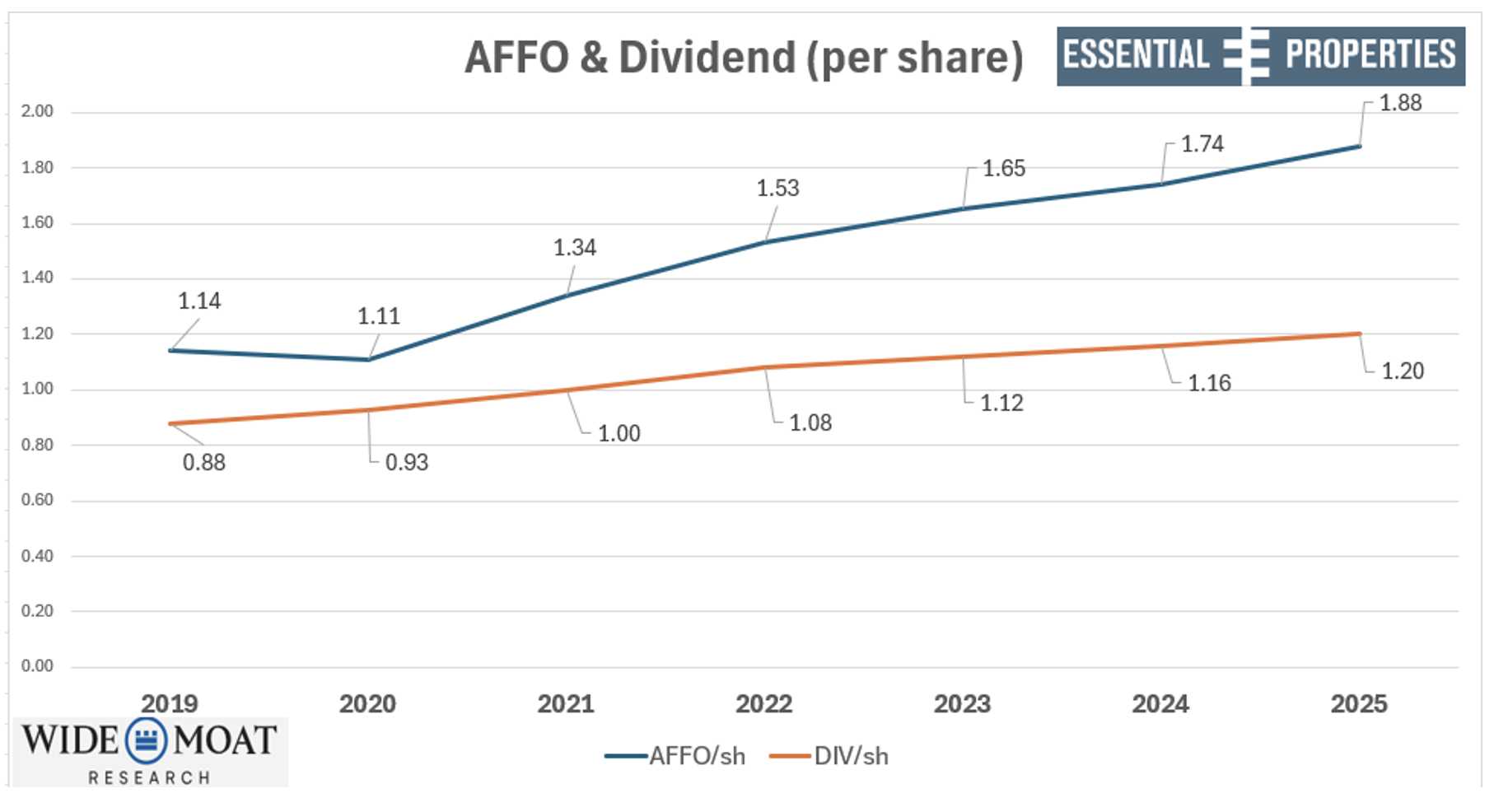

Founded 10 years ago, EPRT has evolved into a defensible dividend grower with a history of above-average dividend growth. It has a conservative capital structure with a 100% unsecured balance sheet. And it features well-laddered maturities, which has led to high cash flow coverage of 4.8 times.

EPRT also has leading earnings growth and investment spreads. As seen below on the blue line, adjusted funds from operations (“AFFO”) has increased by around 8% annually. That’s created a wider margin of safety for the dividend, which has a healthy payout ratio of 64% and 4% yield.

{kind=link}

Shares are also trading at a wide margin of safety, with a 16.3 times price-to-AFFO (p/AFFO) multiple versus its normal 18.4 times. Also, analysts are forecasting growth of 9% in 2026.

For all those reasons, I’m targeting shares to return 20% or more over the next 12 months.

{kind=link}

Source: FAST Graphs

Game On!

VICI Properties (VICI) is a net-lease REIT that owns 93 properties that generate over $3.15 billion in annualized rent. A majority of its properties are leased to casino operators such as Caesars Entertainment (CZR), MGM Resorts (MGM), and Penn Entertainment (PENN).

One key advantage for VICI is how its lease terms are much longer than its peers, averaging 40.1 years. In addition, 42% of its rent roll includes CPI-linked escalation this year. And a full 90% have those provisions over the long term.

I recently interviewed VICI CEO Ed Pitoniak for members of Wide Moat Premier, and we discussed Las Vegas’ current soft economy. He told me his company’s portfolio remains 100% leased, nonetheless.

That’s because the gaming regulatory environment creates high barriers to entry, limiting tenants’ ability to switch locations. Plus, it’s a costly hassle moving an entire casino from place to place.

Honestly, can you imagine Caesars Palace or the Venetian moving locations because of one or two slow years in Vegas? Of course not. And that’s why – even through COVID-19 – VICI collected all of its rent checks on time.

That’s the kind of moat we look for.

Since VICI was formed in 2017, it has demonstrated solid financial discipline. So much so that it took the shortest time from IPO to inclusion in the S&P 500 of any other REIT.

Yet somehow, VICI shares remain cheap, trading at 14.2 times p/AFFO compared with its normal 15.4 times. Its dividend yield, meanwhile, is 5.4%.

Analysts are forecasting growth of 4% in 2026, which leads me to my 12-month total return target of 20%.

{kind=link}

Source: FAST Graphs

Zooming back out to a bigger economic picture, we’re forecasting two to three rate cuts by the end of 2025… and up to five next year. That will lower the cost of capital for REITs and drive wider investment spreads.

Net-lease REITs should be particular beneficiaries of a declining-rate environment. But make sure you still choose your portfolio picks wisely.

One way to do that? Make sure to watch my YouTube show today.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|