Editor’s Note: As longtime readers know, Brad regularly guest lectures on real estate investing at colleges across America. Recently, he was invited to Penn State to speak to a group of finance students. Below is an excerpt from his presentation, edited for clarity.

Good afternoon. It’s wonderful to be here with you today. I always enjoy speaking with students and I’m thrilled to be here at Penn State with you all.

The topic I’d like to discuss today is how to build a real estate investment trust (“REIT”) “monopoly.”

Some people – probably the kind who tend to lose at Monopoly – think it’s mostly about luck.

If you’ve ever played Monopoly, then you know the rules. You roll the dice. You move however many spaces it tells you to. You pay if you have to pay, or you buy it if you can buy. End of story.

But really, Monopoly is very much about understanding the board. It’s about discipline, psychology, timing, and calculating potential returns. For instance, just because you can buy a property doesn’t mean you should…

You’re often much better off saving your money for another deed: one that provides higher rent potential.

In short, Monopoly is very much an investor’s game. You can’t control everything, it’s true; but you can make (or lose) a lot of money with the choices you do have.

For instance, did you know that some of the most advantageous properties to own in the game are the orange ones? Those would be St. James Place, Tennessee Avenue, and New York Avenue. That’s for a few reasons.

First, they are relatively cheaper to purchase and develop. The properties cost $180, $180, and $200, respectively. You can compare that with the dark blue properties, which cost $350 and $400. Houses are $100 each. Your all-in cost to “develop” those orange properties with four houses each is therefore $1,760. Should anybody land on one of those four-house properties, they would pay $750, $750, and $800. Again, that’s respectively. You have, in essence, recouped nearly half your investment… in one fell swoop.

And players land on these properties more often than not. That’s because these properties are six, eight, and nine spaces from “jail.” Ask any statistician, and they will tell you – those three numbers are among the likeliest outcomes when rolling a pair of dice (only seven comes up more often). And because there are cards, and a dedicated space, that sends players directly to jail, it means these properties are among the most landed-on in the game.

Again, while just a game, it teaches us something important – properties that produce superior returns and see consistent “demand” are among the best you can own.

That’s why I stress so often that not all REITs are equal. You must understand their risk/return characteristics and invest only in the highest-quality assets.

The ones that hold a “monopoly” or oligopoly on a certain offering with hard-to-replace assets can:

-

Raise prices (within reason) without losing customers

-

Pass on inflation

-

Maintain margins during downturns

That’s why property sectors such as cell towers, data centers, manufactured housing, net-lease, and industrial REITs outperform over long periods.

Monopolies also benefit from lower unit costs, since fixed costs are spread across more revenue-producing assets. And that leads to higher margins, more reinvestments, and even more scale.

Of course, it’s possible to misuse a monopoly once you have it. So we look for strong balance sheets governed by wise management teams who:

-

Issue equity only when it’s accretive

-

Recycle capital rationally

-

Strategically choose their growth opportunities

That can all be said of two of my favorite REITs. These “monopolistic” landlords are likely to continue generating optimized risk-adjusted returns for years to come…

Starting with a warehouse landlord that helps make the world go ’round.

Prologis Knows How to Play the Game

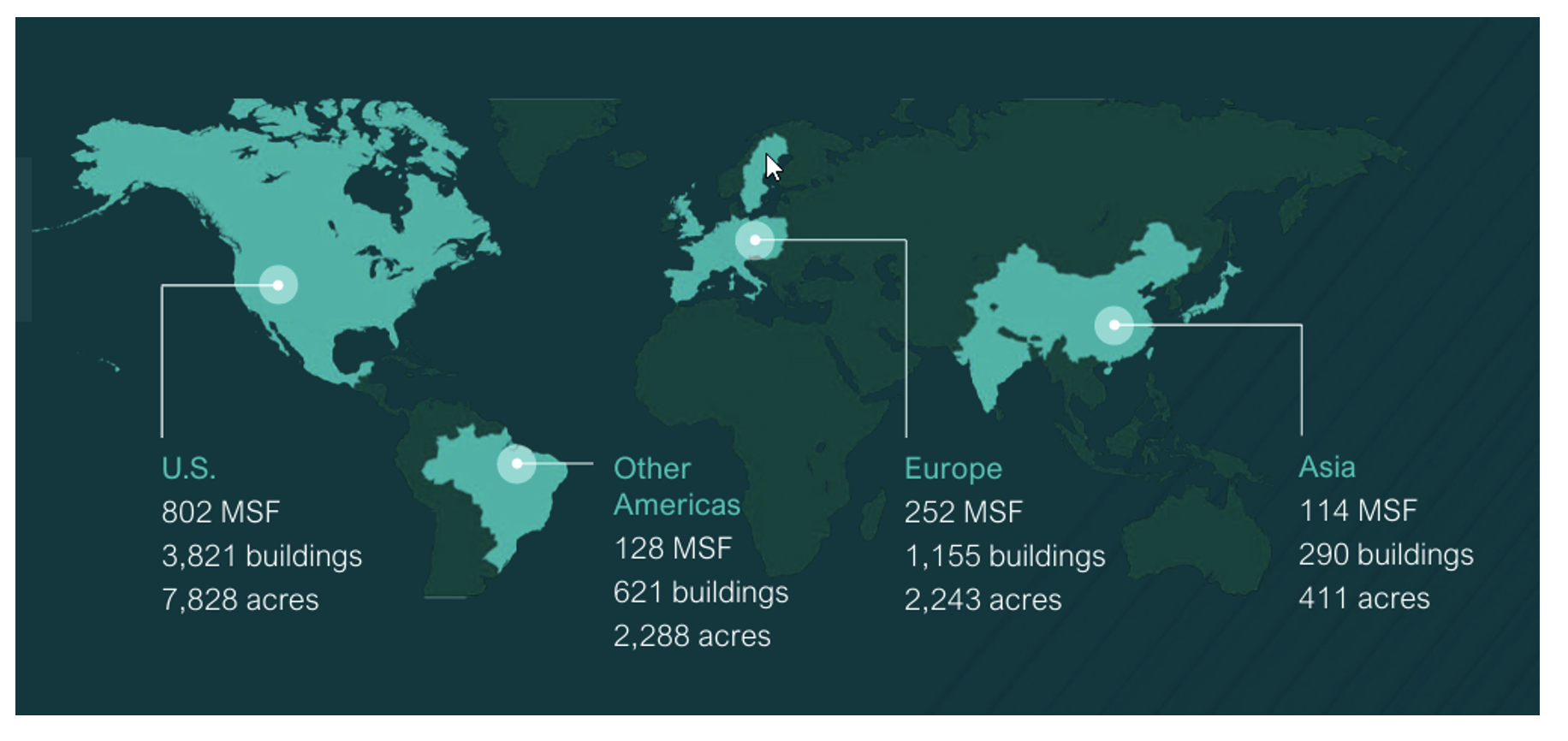

Prologis (PLD) is an industrial REIT that owns a 1.3 billion square feet best-in-class portfolio. Its 6,500-plus customers are spread across 20 countries and 5,887 buildings.

As the largest of its sector-specific peers, Prologis has dominant scale advantage in the U.S. (3,821 buildings), “other Americas” (621), Europe (1,156), and Asia (290).

{kind=link}

Source: Prologis Investor Presentation

Prologis has a market capitalization of around $121.8 billion. It generates around $6.6 billion in net operating income (“NOI”). And it has a development pipeline of $4.7 billion.

The REIT also has a land bank that could add another $42 billion in value, as well as a growing data-center business with 10 gigawatts (“GW”) of capability – so far – with attractive 25% to 50% profit margins. To say nothing of its fortress balance sheet.

As of the fourth quarter of 2025, Prologis reported same-store NOI growth of 4.7% on a net effective basis and 5.7% on a cash basis. Each was ahead of its midpoint guidance. And for the full year, net effective same-store growth was 4.8%, hitting the top end of the range.

In addition, Prologis introduced initial core funds from operations (“FFO”), including net promote expenses, in the range of $6 to $6.20 per share. It expects core FFO excluding net promote expenses to be $6.05 to $6.25.

We also need to consider its development start guidance. It achieved $2.9 billion last year and expects $3.5 billion, including new data-center builds. If achieved, that would be the highest level of starts since 2022.

There’s only one real problem I see in buying in.

Prologis screens slightly more expensive than I’d prefer. Its price/earnings-to-growth (“PEG”) ratio is 3.4 times, its price to adjusted FFO (P/AFFO) ratio is 28.8 times compared with a normal 26.9 times, and its dividend yield is just 3.1%.

As with our Monopoly example, we want to own properties that produce superior returns at a fair price. In the case of Prologis, that price might just be a bit steep at the moment.

Realty Income Is a Real Estate Deal

Another REIT is Realty Income (O), aka “the monthly dividend company.” This San Diego-based company is a net-lease landlord that owns over 15,500 properties in the U.S. and Europe. It has at least one rentable building in every single state, amounting to 82.3% of its portfolio. The U.K. represents another 13.9% and mainland Europe the remaining 3.8%.

Similar to Prologis, Realty Income benefits from its “wide moat” scale advantage. (They’re both S&P 500 constituents as well.) It’s highly diversified by revenue, with modest exposure to its top five customers: 7-Eleven, Dollar General, Walgreens, Family Dollar, and Life Time Fitness.

That’s partially because this REIT has an almost insatiable appetite to grow. Yet it still can be (and is) extremely selective in its growth opportunities thanks to the high fragmentation in the net-lease sector.

Put simply, there are plenty of properties to choose from.

From 2020 to 2024, Realty Income sourced about $345 billion of potential investment opportunities and selectively acquired around $31 billion. And through the third quarter of 2025, it sourced some $97 billion in volume, including $43 billion in the second quarter of 2025 alone – the highest quarterly sourcing volume in its history.

By diversifying and expanding the company’s access to capital, including through private capital, Realty aims to access additional capital sources that enable it to pursue a broader set of opportunities focused on long-term initial rates of return (“IRR”).

We like Realty Income’s valuation today. Shares are trading at 14.5 times instead of their normal multiple of 17.2 times, with a dividend yield of 5.2%. I see a high probability that this REIT will one day become a Dividend King with a 50-year track record of annual dividend growth.

{kind=link}

Source: FAST Graphs

It’s hard to go wrong when you buy up REITs like these two at the right price. I’m not saying they’re perfect. No investment ever is.

But Prologis and Realty Income certainly know how to play the game. And holding their “deeds” certainly tends to pay off.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|