I’m a big believer in diversification.

I have been ever since I lost everything in 2008, when the housing market crashed.

Almost all my net worth was in the brick-and-mortar commercial real estate (“CRE”) I owned. That and a few franchise businesses. So I had little to fall back on when the bubble burst.

That’s why I’ve amended my investment ways since.

It’s true that, 17 years later, I still buy into CRE. And my regular readers know I recommend a lot of real estate investment trusts, or REITs, as well.

These companies, which own real estate-specific assets, are legally exempt from paying corporate income taxes. In return, they pay out at least 90% of their annual taxable income to shareholders in the form of dividends.

The right REITs – and there are many of them – offer consistently rising dividend payouts and share price appreciation at the same time. That’s one of several reasons I like holding them so much.

Even so, here’s what I wrote in The Intelligent REIT Investor Guide a few years ago:

A wise investment strategy is to own both REITs and other higher-yielding stocks along with other investments. You should always strive for the right investment mix for your personal financial situation, tolerance, and goals.

In other words, you shouldn’t own only REITs. And, as I go on to explain further in the book, you shouldn’t own just one.

REITs span over a dozen categories – from retail to data centers to casinos to hospitals – giving investors even more chance to diversify their holdings. I highly recommend holding at least six in the average portfolio, though 10 to 20 is probably more ideal for diversification across the various real estate sectors.

With that said, if you’re just getting started in the REIT world and you’re looking to buy up just one at a time… then Realty Income (O) is a great place to start.

A Wide Moat REIT

I know, I know. I write about Realty Income… a lot. In fact, some readers will occasionally write in asking why it’s such an area of focus.

Today, I’ll tell you. And I’ll show you why now might be the best chances to buy shares in over a decade.

Realty Income started out as a small, West Coast-focused, free-standing net-lease REIT in 1969. Today, though, it has grown into an S&P 500 juggernaut with over 15,600 properties around the world.

The REIT recently entered Poland, its eighth market, where it acquired an asset from EKO-OKNA, a well-known PVC window producer.

With around 13.1% of revenue generated from Europe and the U.K., Realty Income maintains a competitive edge by sourcing properties at higher cap rates. You can think of a cap rate as the “yield” on an asset based on one year of income. So long as that rate is sustainable, the higher the better.

In the second quarter of 2025, for instance, Realty Income invested $1.2 billion – with nearly $0.9 billion in Europe, where cap rates averaged 7.2% compared with 7% in the U.S.

This geographic diversification also mitigates risks related to regional economic slowdowns and geopolitical volatility. And while it mostly focuses on non-discretionary, low-price-point, service-oriented customers, it makes sure to spread itself out by industry, too.

Realty Income’s portfolio of clients are leaders in their industries, spanning categories such as groceries, drugstores, convenience stores, and gaming facilities. Its top 15 clients, which make up 15% of its total annualized contractual rent, include.

-

7-Eleven (3.5%)

-

Dollar General (3.3%)

-

Walgreens (3.3%)

-

Dollar Tree/Family Dollar (3.0%)

-

EG Group Limited (2.1%)

-

Wynn Resorts (2.0%)

-

Lifetime Fitness (1.9%)

-

FedEx (1.9%)

-

B&Q or Kingfisher (1.6%)

-

BJ’s Wholesale Club (1.6%)

-

Asda (1.5%)

So even if one of those big names went under, it would only affect Realty Income so much.

Realty Income also recently launched an Evergreen U.S. Core Plus Fund as means to diversify its sources of capital even further. By utilizing an open-end fund structure to invest in net-leased real estate, it can enhance acquisition investment spreads and bolster returns for shareholders.

These kinds of business decisions help Realty Income maintain a “wide moat” cost of capital. At the end of the second quarter of 2025, its debt-to-annualized pro forma adjusted earnings before interest, taxes, depreciation, and amortization was 5.5 times, with $5.4 billion of liquidity.

Realty Income ended the second quarter of 2025 with 98.6% portfolio occupancy. That’s approximately 10 basis points ahead of the first quarter of 2025 and above its historical median of 98.2% from 2010 to 2024.

Adjusted funds from operations (“AFFO”) were $1.05 in the second quarter of 2025. It raised the low end of its guidance, which is now $4.25 to $4.28 per share. And it increased its 2025 investment volume guidance to $5 billion.

In short, Realty Income is very well positioned to handle the present and future alike.

The Price Is Right

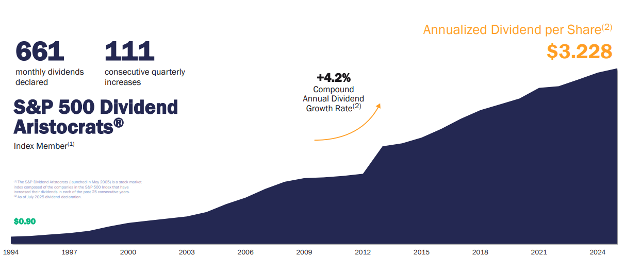

When it comes to dividends, Realty Income is the real deal. It has increased its dividend annually all throughout its 30-year history as a public company and even its overall 50 years.

Realty Income even trademarked itself as “The Monthly Dividend Company.” That’s how serious it is about paying its investors.

{kind=link}

Source: Realty Income

And all of that currently comes with a very attractive price tag.

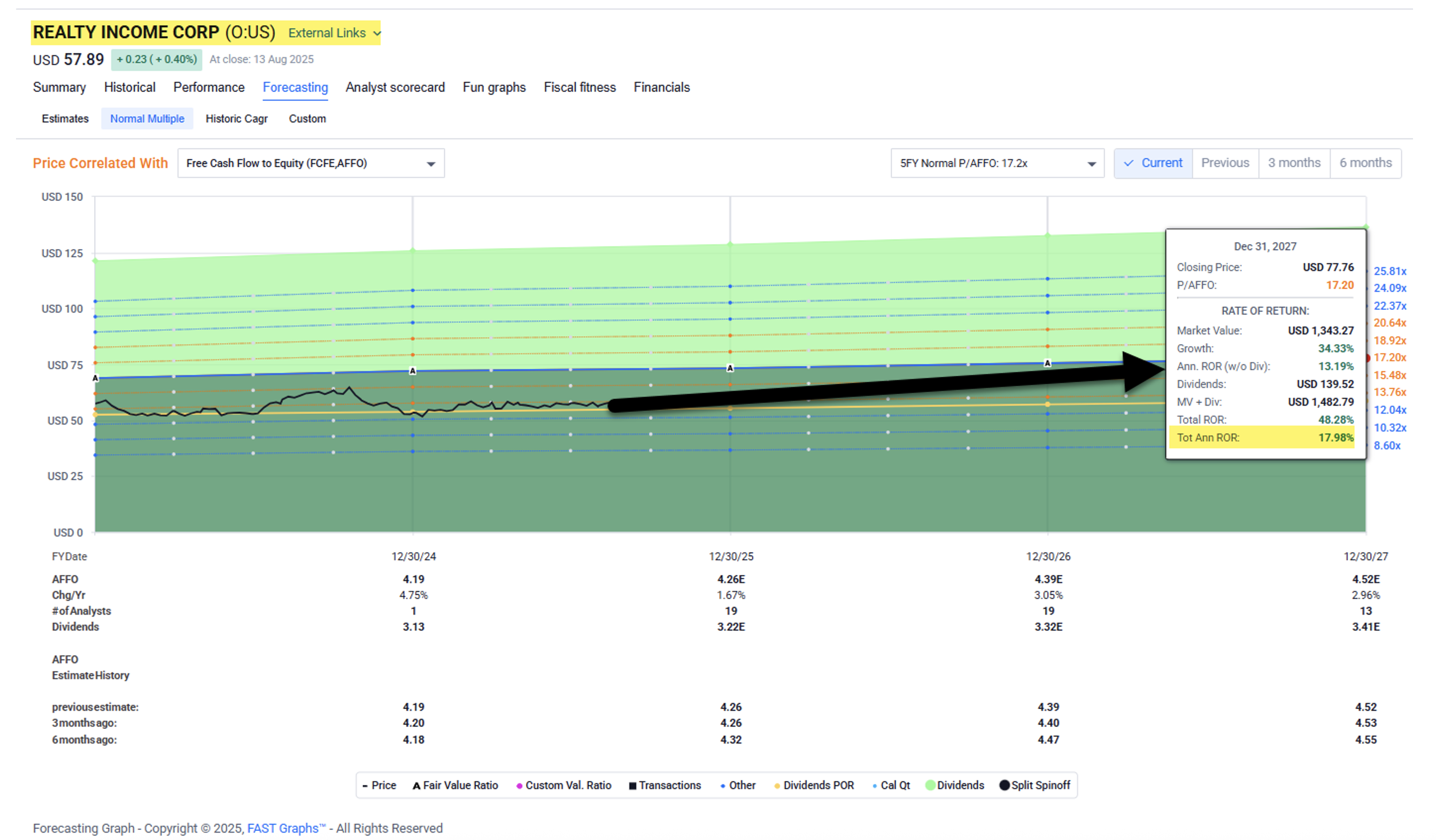

Realty Income is now trading at 13.7 times price-to-AFFO multiple. That’s far below its normal multiple of 18.1 times. And as my friend Chuck “Mr. Valuation” Carnevale pointed out recently, it has only been cheaper twice – in 2008 and very briefly in 2020.

Like many other REITs, it has become cheaper as a result of higher interest rates… even though those rates have only modestly impacted the company’s investment spreads.

As I mentioned, in the second quarter of 2025, the company acquired assets at cap rate of around 7.1% with a weighted average cost of capital of around 6.2%. It has normally grown earnings by 4% to 5%, but earnings are now in the 2% to 3%, range given the higher-rate environment.

{kind=link}

Source: FAST Graphs

It should also be pointed out that Realty Income’s European exposure means it’s not completely subject to U.S. interest rates, which are fairly high compared with many other countries. (This factor also creates an additional net investment hedge capacity in euros, providing the company with more debt capacity in a low cost of capital currency.)

But as for the U.S., where does Realty Income hold the bulk of its assets? In my view, when rates begin to decline (see my latest article here), Realty Income will be one of the first REITs to lift off. But for now, you can still buy shares with a dividend yield of around 5.6%.

That’s extremely attractive considering the company’s quality balance sheet, revenue stream, and dividend. Consistency and durability are attributes for competitive advantage.

What I find most attractive about Realty Income is the potential for long-term wealth creation.

There’s no need to be cute when it comes to Realty Income. It’s one of the best REITs to own right now, and I expect shares to return between 15% and 20% over the next 12 months.

{kind=link}

Source: FAST Graphs

I know I talk about Realty Income a lot. It has earned that attention. Chances are very good I’ll be mentioning it again before too long. It’s the picture of reliability and consistency.

It deserves a spot in any serious REIT investor’s portfolio. And if you’re just starting to build out the real estate segment of your portfolio, this should probably be the first one you buy.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|