Yesterday, I argued that the Federal Reserve will drop rates – perhaps significantly – in September. It all but has to after the jobs numbers last week.

In case you missed it, the Bureau of Labor Statistics (“BLS”) reported utterly dismal numbers. July’s jobs came in at a mere 73,000 jobs instead of the expected 104,000. And May’s figure was revised from 144,000 down to 19,000, while June’s went from 147,000 to 14,000.

It wasn’t pretty, to say the least.

On the plus side, as I wrote, that almost certainly means the Fed will cut rates in September.

Powell & Co. has maintained the Fed Funds rate at 4.25% to 4.5%.

One of the given reasons behind this continued decision has been the strong jobs market. Powell even said on July 30 that “the labor market is kind of still in balance.”

That’s why he has been fully focused instead on potential inflationary effects from Trump’s tariffs…

Powell will often talk about the Fed’s “dual mandate” – price stability (controlling inflation) and maximum employment. Since late 2021, the Fed has been focused almost exclusively on the former. Now, Powell’s going to be forced to look at the latter.

That’s why, as of [yesterday] morning, the market is pricing in an 85% chance of a quarter-point cut in September, as measured by the CME FedWatch Tool.

And we could see more cuts in October and December as well, depending on how subsequent data shapes up. That could do wonders for business dealings, including mergers and acquisitions. The housing market, too, perhaps.

That’s another topic I wrote about recently – last Thursday, to be precise. But I’m switching the subject to commercial real estate (“CRE”) today.

The housing market continues to struggle under numerous factors. Interest rates are just one of them. But there are far fewer factors depressing well-established, well-maintained, corporate-owned CREs these days.

That means investors should be looking at real estate investment trusts, or REITs.

Where REITs Are and Where They Should Be

I’ve talked about REITs many times before here on Wide Moat Daily. These corporate landlords are my specialty and an asset class I’m proud to cover.

I’ve personally seen how the right REITs can transform a portfolio over time. These mandatory dividend payers are governed by strict rules that tend to keep them more conservatively managed.

In exchange for an income tax exemption, REITs pay out at least 90% of their otherwise taxable income annually to shareholders. This setup tends to mean that they pay higher dividends than other companies, not to mention more stable ones, too.

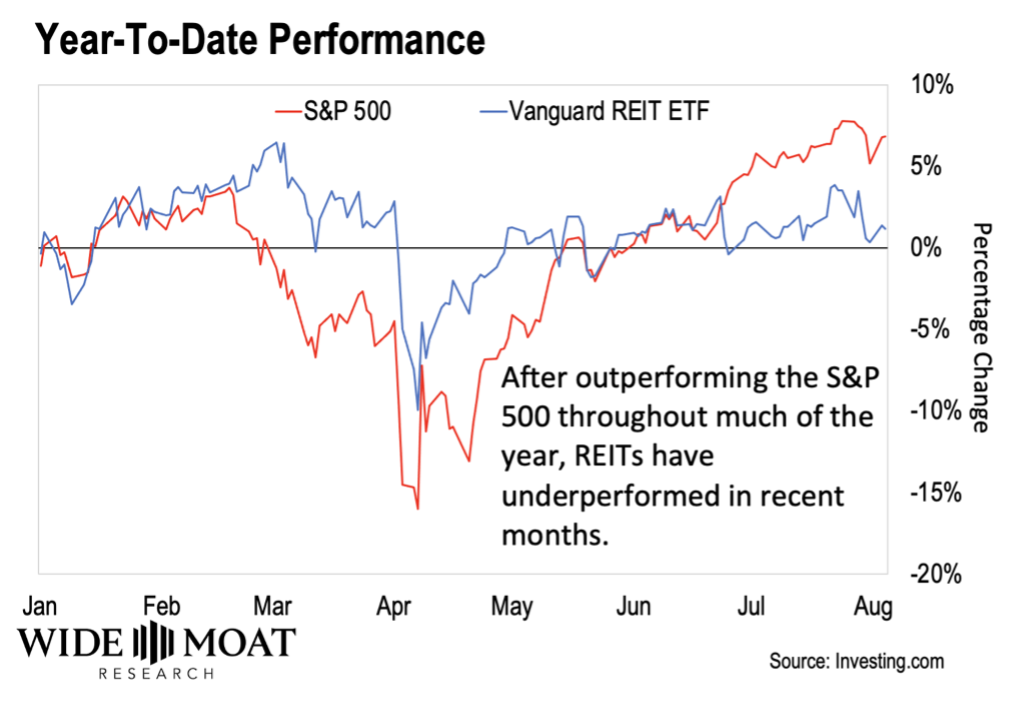

Dividends are well and good. But when it comes to share price appreciation, REITs haven’t done much lately. In fact, they haven’t done that well since the Fed began raising interest rates in early 2022. And while REIT enthusiasts like me certainly hoped this year would mark their big share price return…

That just hasn’t happened yet.

As of yesterday, the S&P 500 was up 7.6% year to date. Whereas Vanguard Real Estate Index Fund (VNQ) – a suitable gauge for U.S. REIT shares in general – is up a mere 0.8%.

{kind=link}

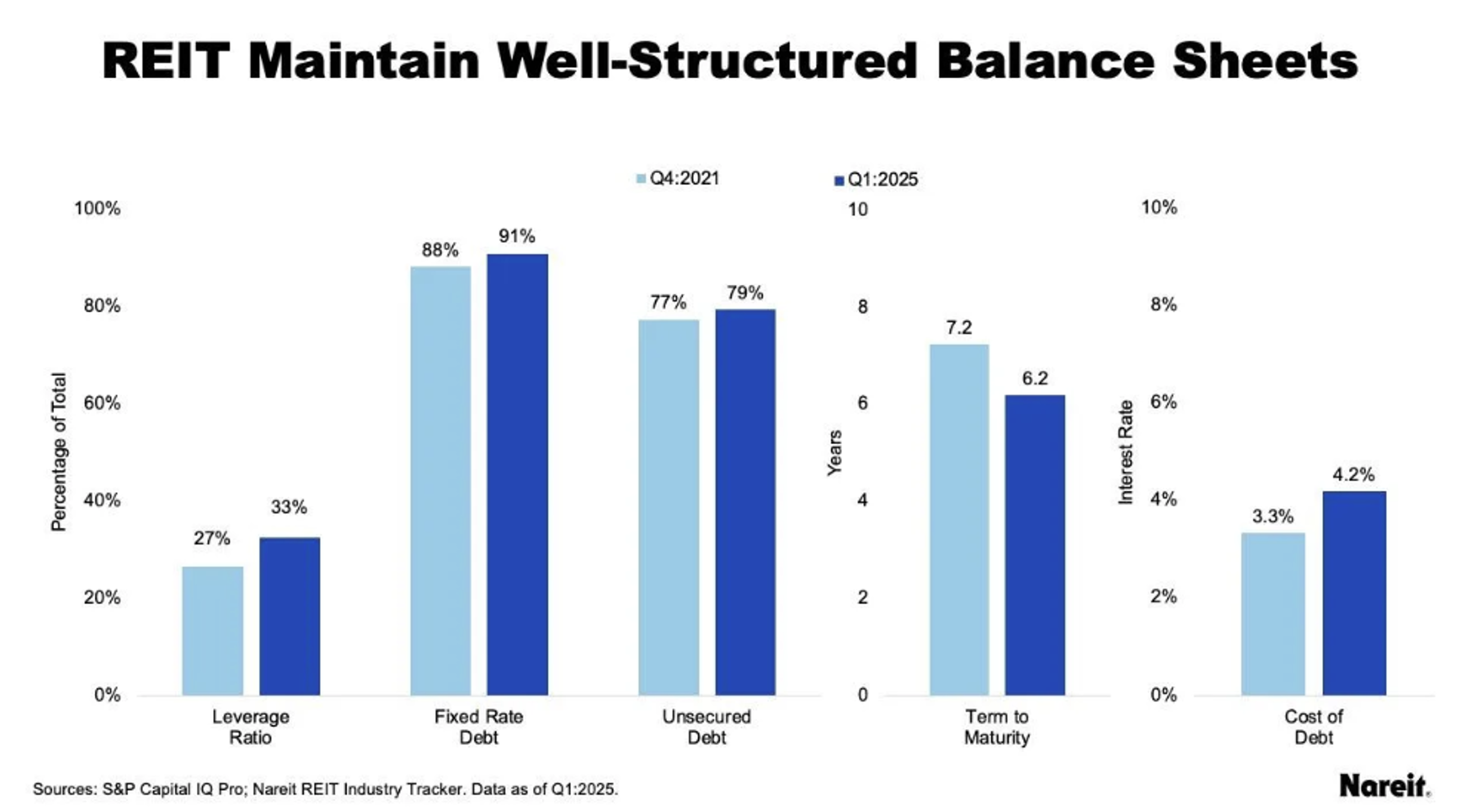

Yet when it comes to their actual financial strength, REITs had a banner first half of the year. CRE Daily, one of my trusted and preferred real estate sources, reported last month that:

-

Average debt costs rose just 0.9% from the fourth quarter of 2021 to the first quarter of 2025, even as the 10-year Treasury yield surged by 2.9%.

-

Emphasis on fixed-rate, long-term debt has insulated REITs from rate volatility.

-

Access to unsecured and cost-effective capital continues to provide operational flexibility.

In short, the share prices for many quality REITs are not reflecting their true value.

{kind=link}

That’s the way it goes with REITs sometimes, though. The markets automatically assume they can’t thrive in higher-interest-rate environments.

Clearly, that isn’t the case, judging by the figure above. But try telling Mr. Market that.

On the plus side, his prejudice gives us a large and clear window to buy quality REITs on the cheap.

A Quick and Easy Play Into REIT-Dom

I’m normally a big fan of buying up individual stocks, REITs or otherwise. But I do see the value in owning some “basket” assets such as exchange-traded funds (“ETFs”).

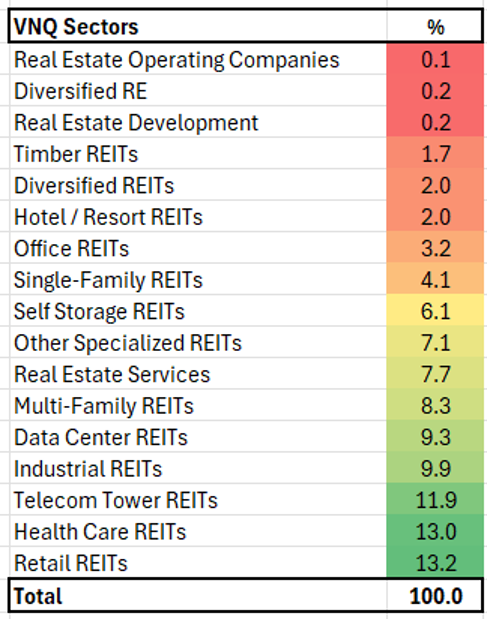

This includes the aforementioned VNQ.

With just under $64 billion in assets under management, VNQ tracks the MSCI U.S. Investable Market Real Estate 25/50 Index’s performance through full replication. This means it physically holds every security the index does in the same exact proportion.

As such, the ETF does own non-REIT positions as well. But those are in the minority, comparatively speaking.

{kind=link}

Source: iREIT

Altogether, it boasts 155 holdings. And it comes with a 3.9% dividend yield – which is really good when you consider the S&P 500 Index tracker yields only 1.14%. Its five largest holdings are:

-

American Tower (AMT), the dominant cell-tower REIT that has a 3.21% dividend yield

-

Welltower (WELL), a health care REIT, with a 1.78% dividend yield

-

Prologis (PLD), the global powerhouse industrial REIT I wrote about last month, with its 3.85% yield

-

Equinix (EQIX), the world’s largest data-center infrastructure provider, at 2.43%

-

Digital Realty Trust (DLR), another data-center REIT, with its 2.83% payout

All five of these REITs, for the record, are top-notch holdings. Though WELL and DLR are both trading higher than I’d like right now. So, if you’re looking for individual assets instead of asset baskets, those two should be wish-list possibilities only until their valuations become more reasonable.

If you simply have to have them now, then the smartest way is probably through an ETF like VNQ.

As for VNQ itself, it closed yesterday at $89.83 – well off its five-year high of $113.15. That price point, incidentally, was achieved in December 2021, shortly before the Fed began to raise interest rates.

That should give you an idea of this ETF’s potential once the Fed begins to reverse course…

Just keep in mind that it does come with a 0.12% expense ratio. This means you pay $12 in fees for every $10,000 in value.

Commercial real estate as an asset class has had a tough few years. No doubt. But I’ve been through my fair share of real estate cycles. Things never stay depressed forever.

Many investors have been ignoring CRE assets for years. My suspicion is that in a few more years, they will wish they had paid attention today.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. If you’re interested in individual REIT names I like at the moment, be sure to check out The Wide Moat Show, my weekly YouTube show, right here.

|