With all the Trump news circulating these days, you may have missed Deere’s (DE) quarterly results. That’s understandable. Compared with renegotiating the global trading paradigm, the humble agriculture technology firm might seem “boring.”

Then again, if you know anything about me, you know I consider “boring” to be beautiful – if it means reliable earnings and dividend increases over time. And for years, that’s what Deere provided.

But the company might have just hit a snag.

Deere is a dividend aristocrat, meaning it has increased its dividend annually for at least the past 25 years. In fact, its track record goes all the way back to 1987 – which is doubtlessly why so many of its investors have stuck with it despite global tractor sales falling since 2023.

Those troubles are partially due to the war in Ukraine, which has destroyed enormous swaths of farmland and increased the price of fertilizer. Plus, the European Union has been making farmers’ lives decidedly more difficult in its quest to fight climate change.

As a result, Deere’s net income fell 22% last quarter after suffering repeated hits in 2024. Yet investors still sent the stock shooting up 6.8% on the news and then another 2.94% on Friday.

The reason?

Deere’s earnings might have been down year over year, but it was better than investors were expecting. For its second quarter, the company posted earnings per share (“EPS”) of $6.64. Investors had been expecting $5.56.

Despite the news. This is still a tough market for Deere. As CFO Josh Jepsen said:

We continue to expect large [agriculture] equipment industry sales in the U.S. and Canada to be down approximately 30% due to pressures from high interest rates, elevated late model used inventory levels, and trade uncertainty.

As for me though, I’m much more interested in Jepsen’s following statement that:

These headwinds are slightly mitigated by stable crop prices, even tighter global stocks, and bolstered farm balance sheets strengthened by the distribution of government funds.

In which case, I know exactly how to invest. And it’s not through Deere.

The REIT Way to Buy Farmland

I’m not counting Deere out. The company has a lot going for it. It’s the largest supplier of agricultural equipment in the world. That’s why we held it for years in the model portfolio of The Wide Moat Letter. We sold the stock in December for a 38% return. As Nick Ward explained at the time:

[W]e’d be willing to place a higher-than-average fair-value multiple on DE shares. We believe that a 17 to 18 times multiple is fair for Deere.

The problem is, from today’s prices, we’d need to see roughly three years of earnings growth to justify today’s valuation, which is pointing toward overvaluation.

And thanks to the earnings surprise, Deere now trades at around 25 times earnings. That makes it just a little too expensive for me to recommend.

And to me, there’s a better way to gain exposure to farmland profit potential. Of course, it’s with a real estate investment trust (“REIT”).

I talk about REITs a lot here on Wide Moat Daily. They’re essentially corporate landlords that operate under very specific legal rules, including the mandate to pay out at least 90% of their taxable income in the form of dividends. This tends to keep their management levelheaded and their payouts safe and steady.

REITs are also exceptionally diverse, allowing investors to buy into the office sector, data centers, hotels, hospitals, research laboratories, warehouses, and self-storage facilities – all of which I’ve written about before. The same goes for single-family rentals, manufactured housing, cell towers, and retail.

But even my regular readers might not know that there are farmland REITs, too. Exactly as they sound, these businesses own large plots of land they rent out for crop production, livestock, or timber.

As I explained two-and-a-half years ago, the last time I wrote about farmland REITs:

[F]armland is one of the largest commercial real estate sectors. Yet it’s still mostly owned by individual farmers, not billionaires and corporations.

Of course, it’s not easy to make a profit that way. There are government regulations to adhere to, equipment and facilities to maintain, and weather to worry about.

That’s where farmland REITs come in, taking “on the land cost, freeing up capital for actual farmers to do what they need to do.”

There are only two publicly traded players in this sector: Farmland Partners (FPI) and Gladstone Land (LAND). And one easily beats out the other in my book.

I’ll let you see why…

Farmland REIT No. 1 Versus No. 2

First up in the farming REIT sector, we have Gladstone Land. It owns 150 farms with around 103,000 acres in 15 states, plus over 55,000 acre-feet of water assets in California.

LAND focuses on fruits and vegetables and certain permanent crops – such as blueberries and nuts – instead of commodity crops like corn and wheat. These categories are generally more profitable and earn the highest rents for landlords.

Since its IPO in 2013, LAND has expanded aggressively to a current value in excess of $1 billion. But in so doing, its payout ratio has become dangerously elevated… which means there’s a high probability it will have to cut its dividend.

{kind=link}

Source: Wide Moat Research

So even though it’s trading at an attractive valuation with a 5.7% dividend yield and a 22 times price to adjusted funds from operations (“AFFO”) ratio, I’m labeling it a “value trap.” That’s a topic I talked about on YouTube last week and also in Wednesday’s Wide Moat Daily.

But bottom-line: Value traps are not something I advise getting tangled up with. I’d much rather direct your attention to FPI.

In addition to traditional farming revenue from commodity crops, FPI has been expanding into energy projects. Today, it has 10 solar farms with a capacity to generate 207 megawatts of renewable energy, and a modest amount of revenue generated from wind turbines as well.

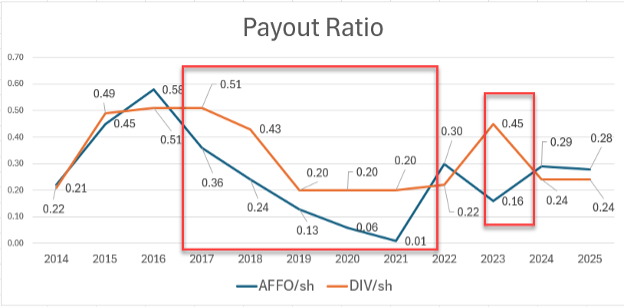

Since FPI listed in April 2014, shares have admittedly returned a miserable 19%, or around 1.6% annually. And much of that underperformance has been driven by poor fundamentals, including an elevated payout ratio for several years.

{kind=link}

Source: Wide Moat Research

But I think it has turned a corner.

FPI, with its $485 million market cap, has reduced its AFFO-based per-share payout ratio to a much healthier 85%. And analysts are forecasting growth of 21% next year.

The REIT also reduced risk and costs by 15% in 2024, and I expect shares to return at least 25% over the next 12 months.

Agricultural land isn’t the type of thing most people think of, but they rely on it every day. Farmers would say people rely on them three times a day – at breakfast, lunch, and dinner. That’s not changing.

And while Deere is the obvious play on agriculture, it’s not necessarily the best right now. For investors looking to get some exposure, I’d recommend taking a closer look Farmland Partners.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. As I write, the breaking news is that Moody’s downgraded the U.S. government, stripping it of its triple-A rating. Stocks opened lower, the dollar sank, and long-term bond yields briefly touched 5%. Be sure to check back for tomorrow’s issue. I’ll be sure to share my thoughts on what it means for the U.S. creditworthiness – and markets – on Tuesday.

|