Did you know that oil is technically in a bear market?

It’s true. Have a look.

{kind=link}

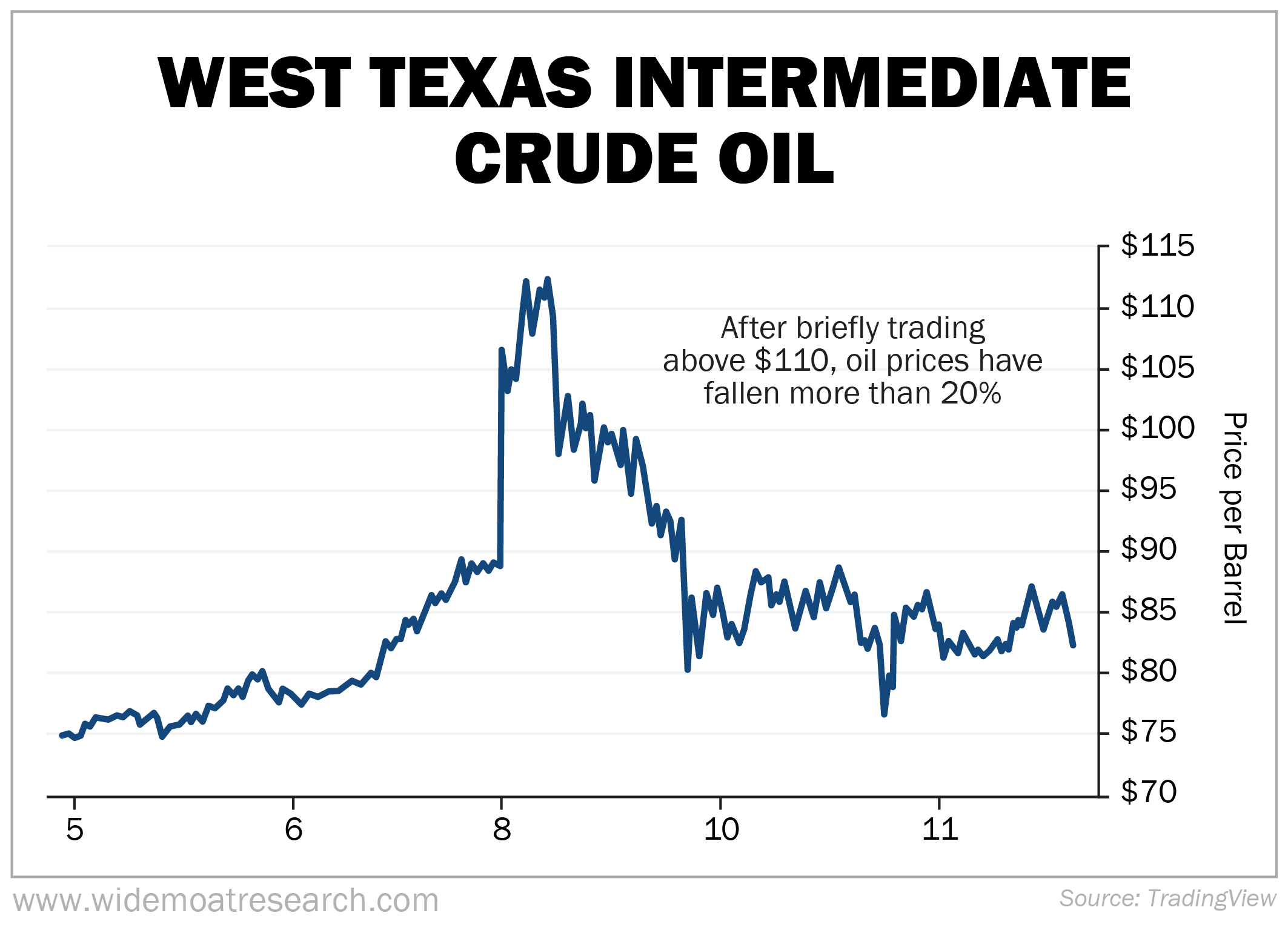

West Texas Intermediate (“WTI”) crude briefly traded north of $110 per barrel on Monday. This coincided with investors considering what a prolonged closure of the Strait of Hormuz – which carries approximately 20% of the world’s oil – would mean.

They didn’t like the answer.

But now, at approximately $84 as I write, the light sweet crude is 25% off those highs… technically a bear market.

Incidentally, that’s a topic fellow analyst Stephen Hester covered on Friday. He did an excellent job, and I highly recommend you read it.

Elsewhere, some other interesting things are happening…

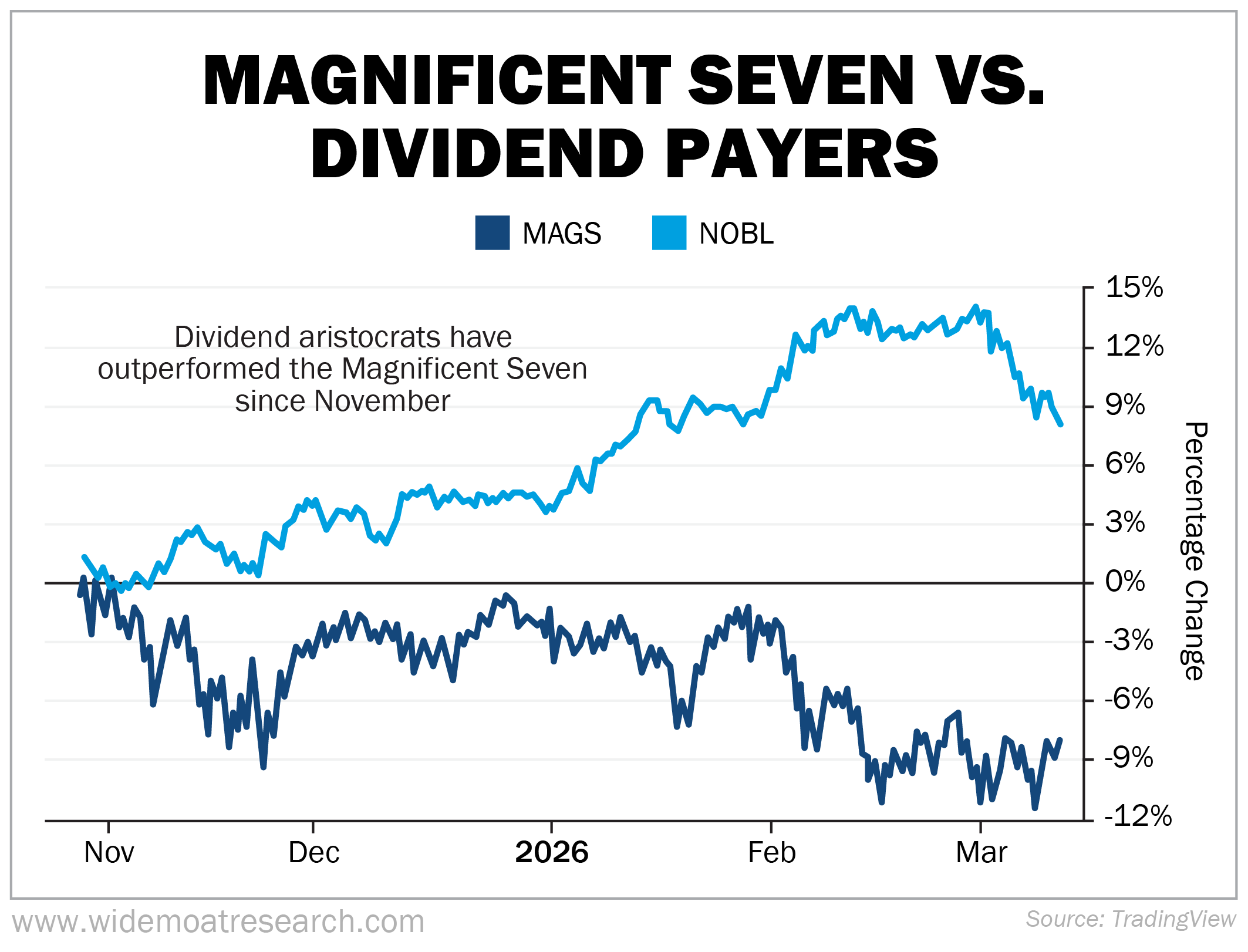

While the world considers the question of regime change in Iran, a different type of regime change is happening in the market. Have a look at the next chart.

{kind=link}

What you’re looking at is the Magnificent Seven – as measured by the Roundhill Magnificent Seven Fund (MAGS) – versus the ProShares S&P 500 Dividend Aristocrats Fund (NOBL).

The former needs no introduction – it’s the seven mega-cap tech stocks that have dominated the market in recent years. The latter tracks a basket of Dividend Aristocrats, companies with at least 25 consecutive years of dividend increases. Most names in that fund will be familiar – Chevron (CVX), Johnson & Johnson (JNJ), McDonald’s (MCD), etc.

It would seem that – at least for the time being – the large-cap AI trade is on hold. Quality and consistent dividends are in. This isn’t entirely surprising.

Research from Morgan Stanley (MS) shows that investors tend to go running for the safe and secure hills in times like this. Or put another way, they put literal stock in high-paying dividend companies.

Which then tend to outperform for months and even years to come.

The Case for Dividend Kings

It’s a lot easier (though not necessarily smarter) to justify risky market plays when the economic sun is shining. Once the clouds start rolling in, however, those assets start to look a lot less tempting.

Here at Wide Moat Research, we believe in building your portfolio based on safety, with a reasonable amount of capital devoted to higher-risk, higher-reward assets. As such, we’re well aware of the Dividend King category. They’re one step above the Aristocrats mentioned above. These are S&P 500 companies that have increased their payouts for 50 years or more.

They’ve proven their ability to not just survive but also thrive in tough times, including but not limited to:

-

The 1979 oil crisis – which also happened to involve Iran

-

Stagflation of the early ’80s

-

The dot-com crisis

-

The economic, political, and societal impact of 9/11

-

The Great Recession of 2007-2009

-

The very much impacted recovery period after that

-

The COVID-19 shutdowns and longer-lasting social distancing efforts

-

Soaring inflation after 2020

-

The higher-interest-rate environment after 2021

Yet they managed their finances brilliantly enough to keep their books balanced and their growth stories progressing. Moreover, they did so with enough cash left over to continue paying and raising their dividends decade after decade… after decade after decade after decade.

Now, this kind of corporate culture is hardly infallible. And it’s important to remember that no track record is guaranteed to continue. That’s why we stress proper portfolio allocation.

With that said, the kind of company that has already proved its mettle in previous hard times is much more likely to get through this latest round.

And if that’s the type of company you’re looking for, there’s one that deserves to be on your radar.

Automatic Data Processing: A Textbook SWAN

Automatic Data Processing (ADP) is one of the world’s largest providers of payroll and human capital management (“HCM”) services. The company offers cloud-based software and outsourcing solutions for payroll processing, benefits administration, compliance, talent management, and HR analytics.

ADP serves more than 1 million businesses worldwide and processes payroll for roughly one-sixth of U.S. workers, making it a mission-critical service provider for companies of all sizes. Its business model is built on recurring revenue and high switching costs, where payroll and HR systems are deeply embedded into corporate operations… making it quite the hassle to change providers.

ADP also benefits from economies of scale, regulatory expertise, and a massive data infrastructure that smaller competitors cannot easily replicate. So, again, its customers tend to stick around.

Yet another advantage is its client funds float, with ADP temporarily holding payroll funds before distribution. It can therefore earn interest on those balances, which can provide meaningful incremental revenue when interest rates rise.

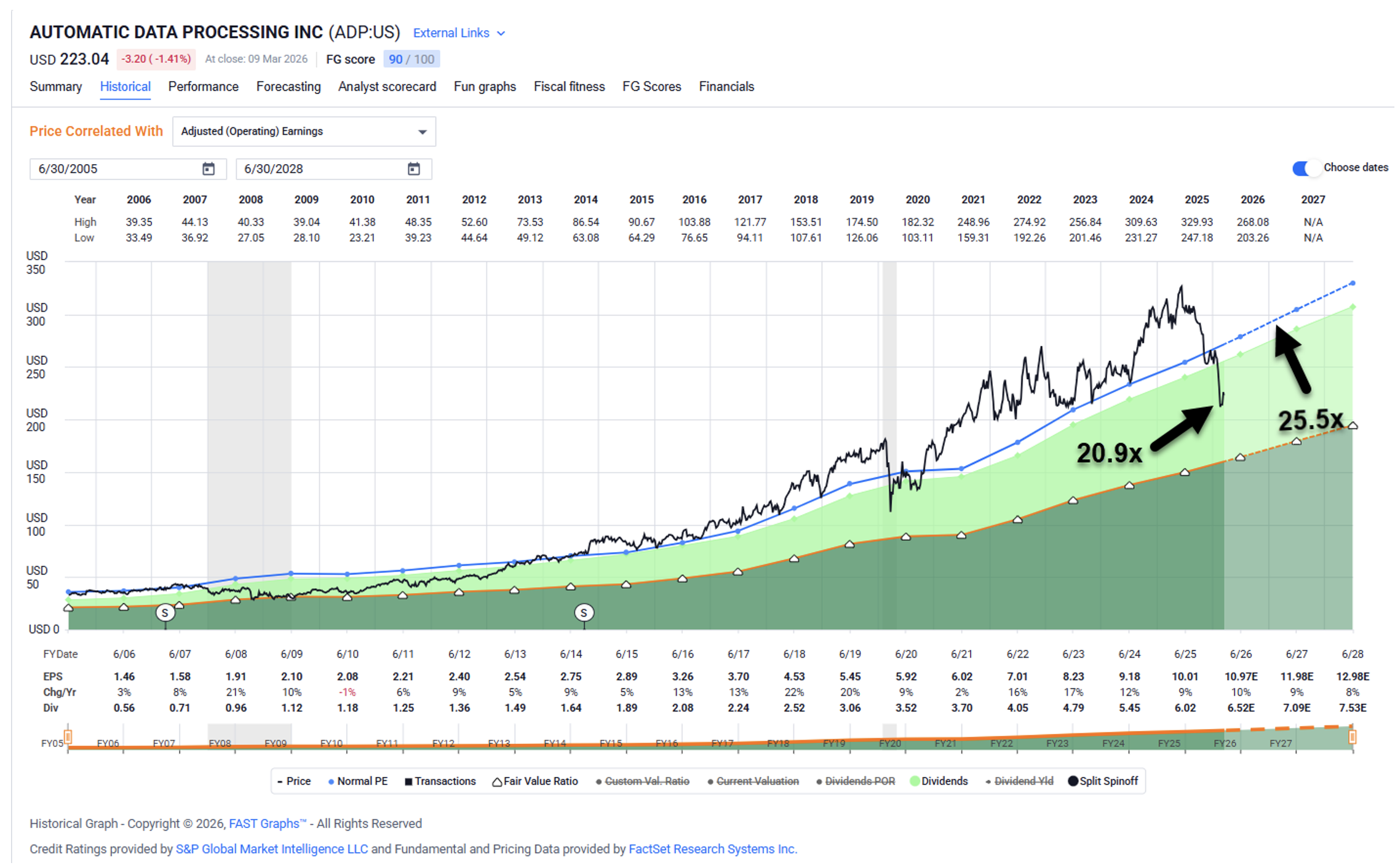

From a valuation perspective, ADP is typically priced at a premium multiple relative to the broader market. This makes sense considering its predictable revenue, strong margins above 25%, and consistent dividend growth.

However, AI fears have investors doubting ADP’s longevity. As you can see below, shares are trading at a wide margin of safety with a 20.9 times multiple compared with its normal 25.5 times.

{kind=link}

Source: FAST Graphs

What they’re overlooking is that ADP is investing heavily in AI-driven HR software, includingnADP Assist and ADP Lyric HCM platform. These tools automate HR tasks, compliance, and workforce analytics, making the company more competitive with modern cloud HR companies.

So the chances are good that this Dividend King will be able to sell its products for higher prices while achieving even better retention than it already boasts.

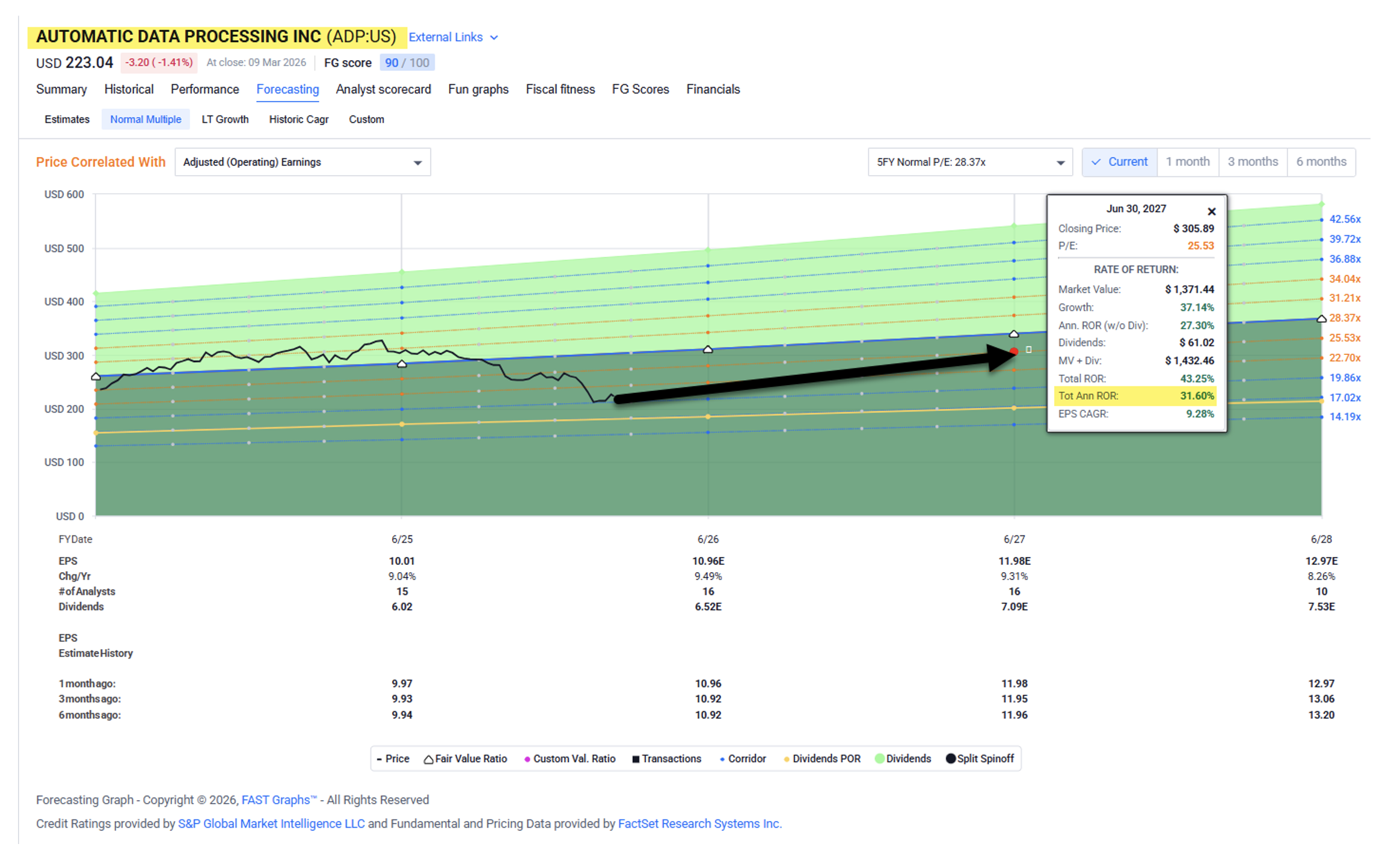

Analysts expect share growth of around 9% in both 2026 and 2027, and the company now pays a healthy dividend, yielding 3.1%. Our conservative total return forecast is for over 25% during the next 12 months.

{kind=link}

Source: FAST Graphs

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Check out the Wide Moat Show on Thursday, where Nick Ward and I will provide a continuing “March Madness” play-by-play of the Elite Eight… Final Four… and championship matchup.

Trust me: You don’t want to miss this one.

|