On April 2, Donald Trump announced his “Liberation Day” tariffs.

On April 3, all hell broke loose…

The Dow Jones fell almost 4%. The S&P 500 was off by 4.8%. And the Nasdaq collapsed by about 6%.

But the president, surprisingly, didn’t seem bothered. Here’s what he said that same day:

I think it’s going very well… markets are going to boom, stock is going to boom, the country is going to boom.

And, yet, by April 9, the tariffs were “paused” for 90 days.

I’m speculating a bit, but I don’t think it was the equities market that worried the administration, it was Treasurys.

A falling stock market is one thing. Perhaps you can live with that. But ask anybody who has worked in finance, especially fixed income, and they’ll tell you – things get very spooky with a disorderly Treasurys market. The U.S. 10-year is the anchor for the global credit market. Everything from mortgages to corporate financing “feeds” off of it.

And after an initial “flight to safety” rally in the aftermath of Liberation Day, the yield on the 10-year spiked from around 3.9% on April 4 to a high of around 4.5% on April 11. If you’re unfamiliar with the bond market, take my word for it. That is a massive move in such a short amount of time.

I think that’s what spooked the administration. Trump appeared to even admit as much: “I was watching the bond market. That bond market is very tricky.”

And if Trump were forced to back down because of the bond market, he wouldn’t be the first president. It was Clinton who supposedly said, “You mean to tell me that the success of the program and my reelection hinges on the Federal Reserve and a bunch of [expletive] bond traders?”

Yes, the bond market can be that powerful. For most people, it’s also a mystery.

Inverted yield curves. Credit spreads. Does anyone really understand what these fixed-income guys are talking about?

I do. I was an institutional due diligence officer for some of the largest broker/dealers in the country. And I know that the bond market is the most honest storyteller in finance. It just speaks in ways most can’t decipher.

In this issue of the Wide Moat Daily, we’ll have a look at the two most important things the bond market is telling us today.

The Bond Market Speaks, but Few Understand

In my hedge fund days around the Great Recession of 2008/2009, we had about 250 traders on the floor. I specialized in thinly-traded, complex, and distressed investments. Others focused on commodities or large-cap momentum stocks.

But no matter their specialty, we all felt the same way about the bond market: “You don’t always understand what it’s saying, but it never lies.”

The U.S. credit markets are valued at $55 trillion. That’s larger than all U.S. stock markets combined. And most fixed income – like investment-grade bonds, municipal bonds, or U.S. Treasury bonds – are not valued with the same subjectivity as stocks.

Is Nvidia fairly valued at its current multiple? Does the valuation attached to Tesla capture the company’s future growth? People can debate those questions, and that debate is what causes these stocks to soar and crash over and over again.

But for bonds, it’s much more black and white.

The average bond has a fixed coupon and maturity with limited upside. And so long as the company doesn’t go bankrupt, all payments should arrive on time. In that sense, it’s a lot simpler than evaluating a stock.

But that also means it’s more competitive.

Intense analysis of the issuer (the company selling the bond) and a bond’s relative value to other bonds is where the “alpha” is in fixed-income investing. It’s more math and less speculation. Outside of super risky junk bonds, values fluctuate based on complicated formulas, not headlines or political distractions.

In short, the fixed-income market is all business.

Credit analysts are also a different breed than equity analysts. Think actuaries and statisticians versus finance and business majors. Volatility in credit markets is always due to fundamentals, and it’s worth paying attention to.

What the Bond Market Is Saying Today

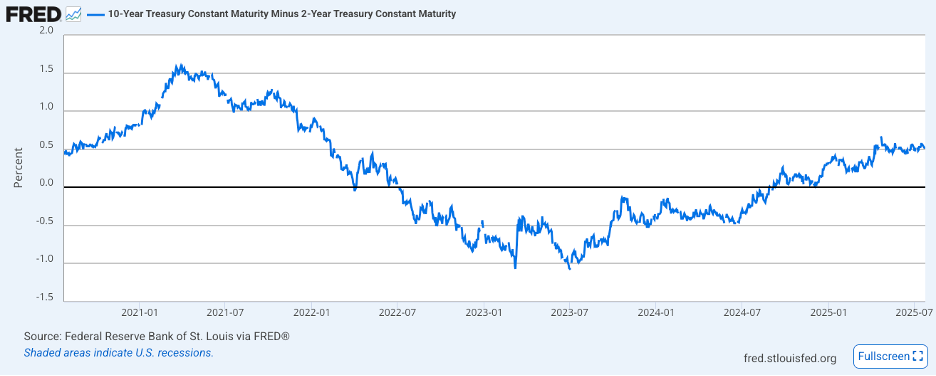

As of July 24, the 10-year U.S. Treasury yield is about 4.4%. This is the benchmark everything else is priced from – even the bonds of other governments. A year ago, it was 4.25%. That’s what you earn for a 10-year commitment, but what about a short-term Treasury investment?

The two-year Treasury now pays 3.8%. A year ago, it was a much higher 4.4%.

This is where things get interesting.

A year ago, the short-term two-year bond yielded more than the long-term 10-year bond. That’s the definition of the “inverted yield curve” you’ve heard about. You can see it for yourself by looking at the “10s and 2s,” as it’s known:

{kind=link}

Source: FRED

When that line dips below zero, the two-year yields more than the 10-year, and the yield curve is inverted.

It is supposed to “guarantee” a recession. That’s because under “normal” circumstances, the 10-year should always yield more than the two-year. After all, 10 years in the future is more uncertain than two years. And this increased uncertainty should reward investors with higher yield.

And when that doesn’t happen, the bond market is telling you something important is off. It’s true that the Fed tends to cut interest rates aggressively in a recession. That spurs borrowing and investing to boost the economy. Now you understand why many interpret lower long-term rates as a recession on the horizon. They believe it’s because when the recession hits, the Federal Reserve will slash rates.

I can’t tell you how many Wall Street pros bet their entire reputation on a recession because of this inversion. I’ve simply lost count.

But it didn’t happen. Those people jumped to their own conclusions. They were focused on what the bond market was saying instead of the why.

In short, the bond market wasn’t buying what the Fed was selling. Ever since 2022, Fed Chair Jerome Powell has sounded decidedly hawkish. The Fed has mostly been signaling that it will be “data dependent.” In other words, they’re in no rush to cut rates.

But the bond market believed interest rates would go down over the next few years no matter Fed policy. Unlike stock investors, the credit markets know that the Fed’s true ability to influence interest rates is grossly exaggerated. Trillions of carefully invested bonds all told the same story.

Contrary to what you might believe, rates can fall for reasons other than the Fed cutting. One is because a recession crashes the economy. The other is inflation lowers.

How do we know which it is?

The bond market can tell us that, too.

Credit Spreads Are the Next Piece of the Puzzle

Many stock investors make decisions based on momentum, hype, and the loudest voice in Internet forums. Fixed-income investors are mostly stoic institutions that focus on cash flows, default probabilities, and interest rate risk. That’s why the fixed-income market tends to be a lot more reliable than the more volatile stock market.

So, what is the fixed-income market telling us about risk today?

We can use credit spreads to find out.

Spreads are just the difference in yields between different fixed-income investments. If a 10-year Treasury bond yields 4% and an investment-grade corporate bond yields 6%, the spread is 2%. That’s the “risk premium” for moving from “risk-free” government bonds to slightly riskier, but still quality, corporate bonds.

This difference – or spread – is a powerful signal about how credit investors perceive risk.

When this spread widens sharply, it means investors are panicking. To give you a bit of context, at one point during 2008, the spread between Treasurys and investment-grade corporates was 6.5%, something you’d typically only see from junk bonds. That is what panic looks like. The credit markets were pricing in that even many strong companies were in potential trouble.

But that’s not the market we’re in.

As of last month, investment-grade bonds paid just 1.35% more than comparable government bonds. Riskier high-yield bonds paid 4.25% more. This is slightly richer than the pandemic boom days. At the same time, they are significantly below historical averages.

This means credit investors are more cautious than the “free money” COVID era, but are less worried than they normally are. In other words, the credit markets are not betting on a severe recession. Instead, they believe inflation will slowly reduce over time, and the economy will remain strong for years to come.

What You Should Do Today

Wall Street’s most reliable recession indicator was dead wrong. The inverted yield curve of a year ago didn’t cause an economic collapse. There wasn’t even a mild recession.

That’s because people heard what they wanted instead of what the credit markets were saying: the Fed can manipulate short-term interest rates all they want, we still believe long-term rates and inflation are heading down.

Credit spreads are a “no BS” way to evaluate recession risk.

If there were a looming recession, the spread between safe bonds and risky bonds would expand rapidly well before the recession actually hits.

But that’s not happening.

As of now, those spreads are less than historical averages.

You’ll likely hear television pundits scream about a severe recession right around the corner.

They’re wrong. And they’ll stay wrong until the $55 trillion credit markets say otherwise.

Right now, the bond market believes the risk is low. And unlike the talking heads on TV, they put their money where their mouth is.

And it brings me back to something I’ve been telling subscribers of High-Yield Advisor for months: Now (right now) will one day be remembered as the best time to buy high-quality bonds in our lifetime.

We have several investment-grade-rated investments paying current annual yields around 10%, and our total annual returns are about double that since inception.

Here are just two examples of recent recommendations:

-

Preferred shares from an insurance giant yielding 7.2% and estimated 48% upside

-

A corporate bond from a leading automotive company paying 7.5% for the next 72 years

And, no, these are not risky bonds issued by companies on shaky footing. They’re about as rock solid as you can hope for.

And the reason I can find them is because I spent 15 years as institutional due diligence officer. I translated that experience into a strategy that gives you the benefits of high-yield investing without putting year heard-earned money into high-risk investments.

If any of that sounds interesting, we’re always accepting new members. The easiest way to learn more is to get in touch with our U.S.-based customer service team. They’d be happy to tell you more. Feel free to reach out right here.

Regards,

Stephen Hester

Chief Analyst, Wide Moat Research

|