In the 1999 cult classic film, Fight Club, there were eight rules that members must abide by.

But the first two were the most important.

One, “You do not talk about Fight Club.”

And two, “You DO NOT talk about Fight Club.”

Hold that thought. We’ll come back to it.

First, have a look at this.

{kind=link}

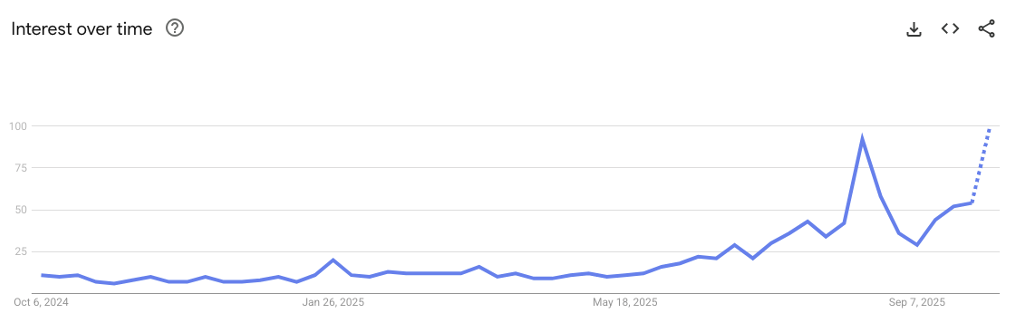

Source: Google Trends

That’s a chart from Google Trends. It shows the relative popularity of a search term over time. This particular chart shows results for “AI bubble.” The dashed line implies incomplete data. But if it holds, it means the term is trending at its highest levels all year.

Browsing some recent headlines, that seems to ring true.

The AP:

Is there an AI bubble? Financial institutions sound a warning.

Bloomberg:

Why Circular AI Deals Among OpenAI, Nvidia, AMD Are Raising Eyebrows

Yahoo Finance:

Why Fears of a Trillion-Dollar Bubble Are Growing

Everybody is talking about it. And that brings us back to Fight Club.

For a massive bubble to form in the stock market, investors must abide by the same two Fight Club rules.

-

You cannot talk about the bubble.

-

You CANNOT talk about the bubble.

That’s what allows the euphoria necessary to fuel a bubble to exist.

When investors are constantly talking about “the AI bubble” and comparing it with the dot-com boom/bust cycle in the late 1990s/early 2000s, they’re generating fear.

Heck, gold prices just hit an all-time high. Gold is the ultimate fear-driven asset class.

Bubbles cannot exist in a fearful environment. Fear and euphoria are like oil and water. They don’t mix.

You think people were sounding the alarm during the dot-com bubble? I mean, some people were. But most of the market was busy explaining why webpage views were more important than earnings and why it made sense for an unprofitable pet-food delivery company to spend $2.2 million on a single Super Bowl ad.

Now, that’s a bubble.

Despite the headlines regarding (potentially circular) dealmaking between technology firms (more on that soon), we’re probably not looking at an AI bubble right now.

On the contrary, I think it’s more likely that we’re looking at a bubble in AI bubble chatter. And it will ultimately dissuade people from investing and capitalizing on great opportunities in the market.

As someone who personally invests a lot of money in the technology sector, I’m alright with that.

Bull markets always climb a wall of worry. That fear is what allows bull markets to sustain themselves over long periods of time without euphorically evolving into bubbles that fly too close to the sun.

That’s all very high-level talk. So, let’s dig into the details.

Why 2025 Is Nothing Like 1999: Fundamentals

There’s bad news and good news. Let’s start with the bad.

Yes, several of the popular AI stocks appear to be speculatively valued at best… or highly overvalued at worst.

Palantir Technologies (PLTR) is probably the worst offender in this regard.

PLTR shares are up by 142% year to date. They’re up by 343% during the past 12 months. And during the past five years, they’re the second-best performer in the entire S&P 500, up by nearly 1,800%.

Yet, all of these gains are based upon future speculation, not present-day fundamental growth.

PLTR is expected to produce $0.64 in earnings per share (“EPS”) this year. With a share price around $182, that implies a price-to-earnings (P/E) multiple of 284 times. Yes, really.

Let’s be generous and look at 2026 earnings. EPS for next year is expected to clock in at $0.84. That would imply a forward valuation of… 216 times.

To be fair, PLTR’s earnings trajectory is strong. The company’s EPS rose by 64% last year. So far, this year’s results point toward another year of 50%-plus bottom-line growth. And looking at analyst forecasts, Wall Street believes that PLTR can continue to compound its profits at a 30%-plus rate for many years to come.

For a company growing that quickly, a 30 times P/E ratio would be more than fair. But to get there, PLTR would need $6.06 in EPS. And to get that, PLTR will have to compound its EPS at a 30.9% rate over the next decade.

Can PLTR do that? Maybe!

But a lot can happen in 10 years. That makes this a very speculative bet.

There will always be individual stocks that trade well above or well below their fair valuations.

Relatively speaking, it requires a lot less capital (and irrational investors) to move an individual stock’s price too high or too low than it does the entire market.

And if Palantir’s stock price tanks, it won’t be catastrophic for the S&P 500 at large.

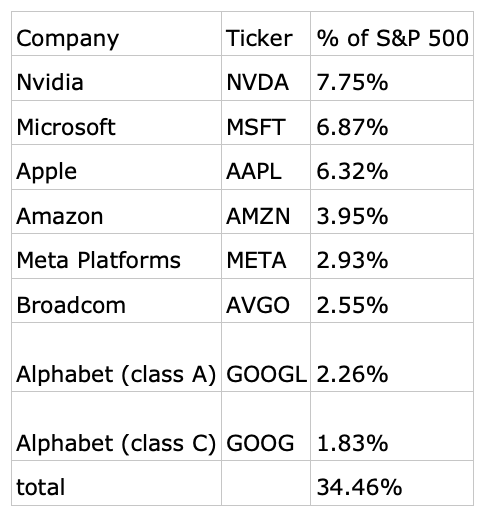

Yes, the largest components of that index are technology stocks. The top seven holdings of the S&P 500 Index make up about 34.5% of its overall market capitalization. All of these companies are factoring into the “AI bubble” talk.

{kind=link}

Thankfully, they all generate extremely strong cash flows and trade with much lower valuations than Palantir. That means the broader market is on much stronger footing now than it ever was in the late 1990s.

{kind=link}

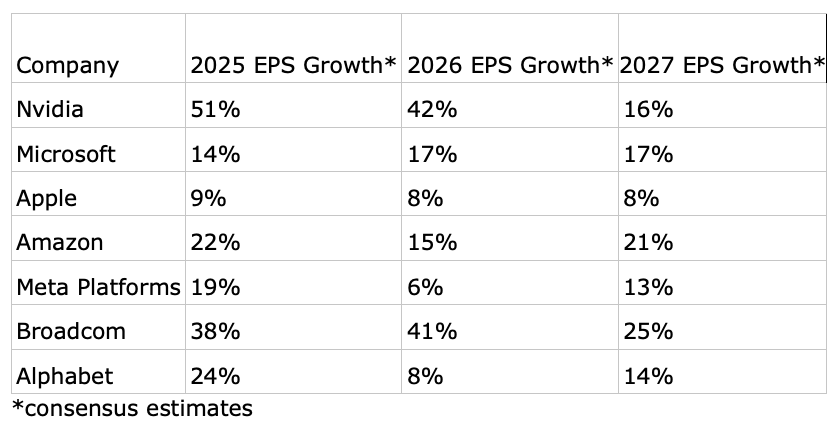

Their growing profits are why I don’t believe the so-called “AI bubble” is going to lead toward a major sell-off.

For instance, Nvidia trades with a forward P/E ratio of 29.8 right now. If NVDA shares sold off by 20%, they’d be sporting a forward P/E of less than 24. NVDA shares haven’t been that cheap since before COVID-19. And 24 times earnings for a company growing its earnings at a 40% rate is very attractive.

Simply put, I don’t see the market letting shares dip much lower than that.

If Microsoft were to trade lower by 20% its forward P/E ratio would be 27, below its five- and 10-year averages of 35.1 and 29, respectively. Microsoft is expected to compound its EPS at a roughly 15% rate over the next five years or so. And with that in mind, it doesn’t make sense for investors to let this stock get much cheaper than 25 times or so.

We can do this same exercise for each of the largest seven stocks in the S&P 500 and come to similar conclusions.

Assuming a 20% fall in the share price, here’s the valuations you’d get:

-

AAPL: 25 times forward earnings

-

AMZN: 23 times (the cheapest valuation I’ve ever seen on those shares)

-

META: 19 times

-

GOOG: Less than 20 times

GOOG would have the valuation of the bunch at just 18 times forward earnings. If GOOG ever trades at 18 times forward earnings, you buy it. It really is that simple.

AVGO would still be pricey after a negative 20% sell-off at 29 times. However, its earnings growth rate for next year is expected to be north of 40%, so on a price-to-earnings-to-growth ratio basis, we’re still talking about a cheap stock.

Could a negative 10% to negative 20% sell-off occur in the Big Techs and the wider market?

Sure, it could. Stocks can go down.

But if the market has any sense at all (and it does), that’s about as far as it goes.

Hopes and dreams were fueling the dot-com boom. Enormous profits are fueling this one.

People are talking about an “AI Bubble.” But talk is cheap. People – especially naysayers – love to blow hot air. Unless the numbers change, I doubt a true bubble will ever form.

Regards,

Nick Ward

Analyst, Wide Moat Research

|