Investors managed to shake off their jitters for the tech sector yesterday. The Nasdaq was up about 2.8%.

But they’re still not so sanguine about retail.

Target (TGT), for example, sank an additional 3.52% on Monday as investors continued to digest its less-than-amazing quarterly results.

I have some opinions about that particular store, which I’ll be sharing on The Wide Moat Show this Thursday. (Yup! It’s still running on Thanksgiving Day.) But for now, let’s all agree that Target isn’t as well-positioned as it would like to be.

The same applies to Lowe’s (LOW) and Home Depot (HD), two other retailers that recently reported quarterly results. The former saw its sales grow year over year but lowered full-year profit expectations. And the latter fell short of Wall Street’s earnings altogether.

Then there’s Lululemon Athletica (LULU), a trendy purveyor of activewear with more than 750 stores worldwide, our subject for today.

As you’ll see, the company has been going through a rough patch. But, in my estimation, the market has overdone it, and the stock now looks like a tempting value.

The Yoga Pants That Launched an Empire

Founded in 1998 as a yoga pants retailer in Vancouver, British Columbia, it really began gaining ground in the early 2010s as women’s leggings became must-have apparel.

That popularity continued for over a decade as Lululemon strategically expanded its products to include larger athletic offerings, accessories, shoes, and even personal care products – for guys as well as gals.

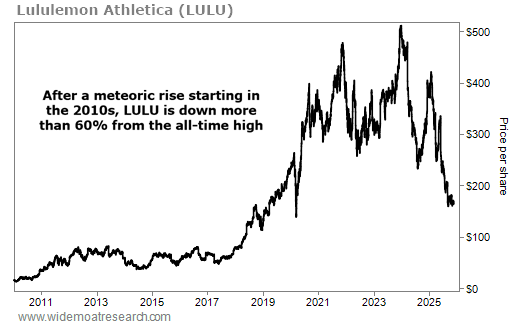

And for years, the stock was a standout. From 2010 to the all-time high in 2023, LULU returned as much as 3,900%.

{kind=link}

But it has fallen on harder times since early 2024. And it shows in the share price, which is down more than 60% from the former highs.

Everyone knows who to blame for that decline, including its own CEO, Calvin McDonald. “We have become too predictable within our casual offerings,” he admitted in September amidst another round of sales drops throughout North America.

Retail Strategy Group’s Liza Amlani added separately that Lululemon’s “assortment has been predictable for some time now. And the reality is that brands like Alo and Vuori have become the bugaboo and are gaining momentum themselves.”

In her opinion – and, apparently, Lululemon’s as well – the company got too comfortable with its own success and lost its edge. Investors have recognized this, too, driving its once lofty share price down, down, and down some more these past two years.

Down so far, in fact, that it has entered official bargain territory.

A Closer Look at Lululemon’s Major Missteps

For the record, I’m not disagreeing that Lululemon took its eye off the ball. Nor am I going to ignore its continuing troubles.

Like how last week, its president of the Americas, Celeste Burgoyne – who has been with the company for 19 years – said she was stepping down to become executive vice president and chief revenue officer at Vail Resorts instead.

This is Lululemon’s second high-profile exit in the past 18 months. Sun Choe resigned last May as chief product officer, a position the company then removed altogether.

On top of that, founder and former CEO Chip Wilson bought a full-page advertisement in the Wall Street Journal last month, equating Lululemon’s “decline” to a “plane crash” and a “sinking ship.”

Directors have “dismantled the business model and lost employees who held the institutional knowledge that made the company great,” he added. But perhaps his biggest critique was that they only care about short-term financial gains in quarterly reports.

And, as I brought up yesterday, that kind of thinking rarely ends up paying off.

Even so, Lululemon hasn’t sunk just yet. Last year, it still saw its company-operated store net revenue rise 14%. And e-commerce net revenue increased 6%.

And while it did recently revise its yearly guidance down from between 5% and 7% to between 2% and 4%, it’s still expecting revenue between $10.85 billion and $11 billion. That would represent 2% to 4% growth year over year – which might not be astronomical but are positive expectations nonetheless.

Lululemon also boasts an excellent balance sheet, ending the latest quarter with $1.16 billion in cash and cash equivalents… with no debt whatsoever.

In addition, the company is aggressively buying back stock at its currently depleted prices. Last quarter alone, it purchased approximately 1.13 million shares at an average price of $247.

But it’s not done yet. As of the start of this current quarter, Lululemon had approximately $860 million remaining on its $1 billion repurchase program.

Lululemon’s Current Price and Value Don’t Match Up

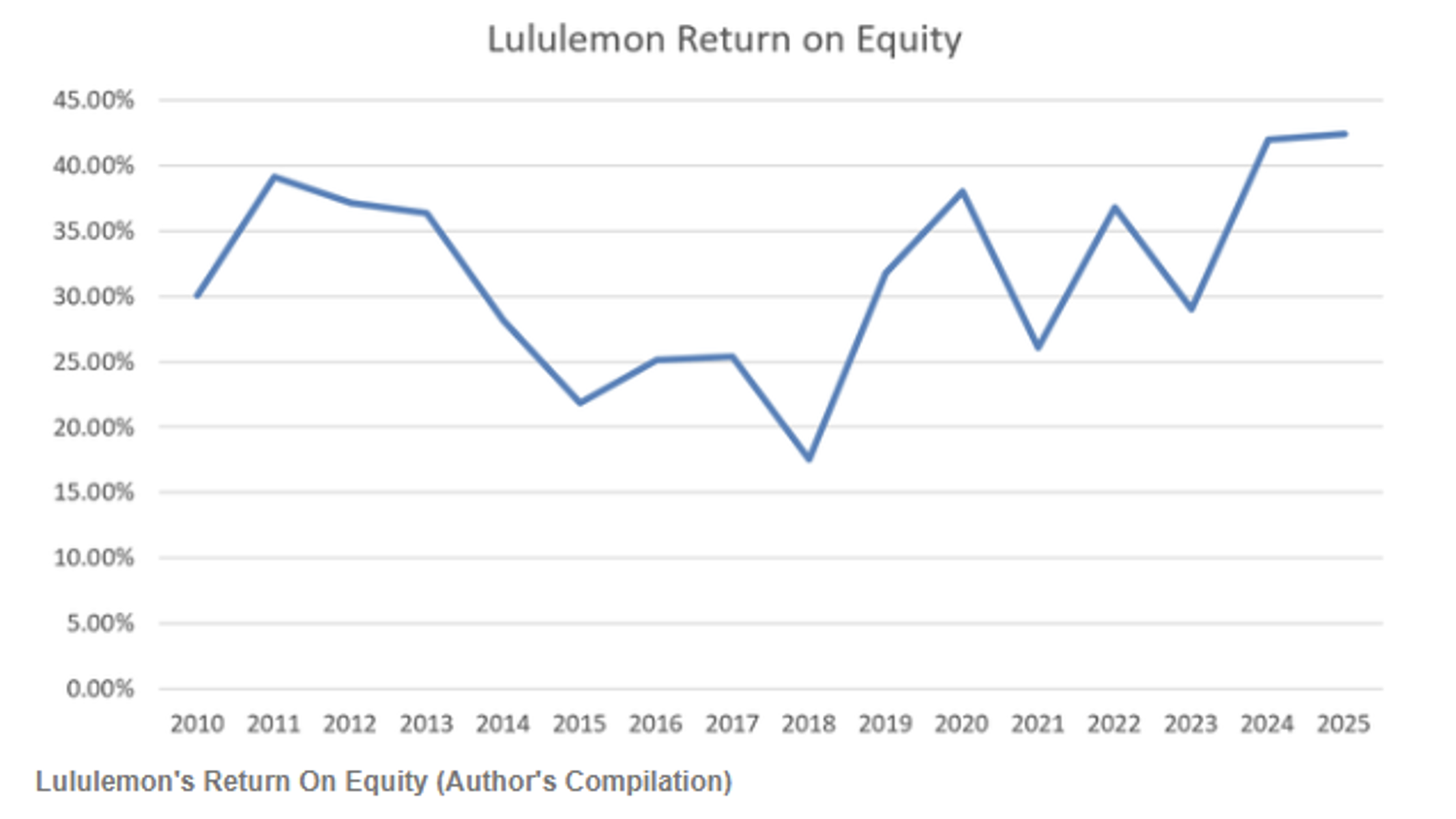

There’s another positive aspect I want to point out about Lululemon, and that’s its return on equity (“ROE”). As one Seeking Alpha analyst, Kevin Anthony D. Arroyo, pointed out:

Since 2010, Lululemon’s ROE has fluctuated between 20% and 30%-plus. While there’s clear wide fluctuation in the company’s ROE, there’s no doubt that Lululemon is doing something phenomenal that allows it not only to generate a high return on equity capital but also to maintain it.

Consistent high ROE for multiple years often indicates a sustainable business moat. Businesses that maintain their return on capital for an extended period of time possess durable characteristics that fend off competition to protect their profits.

{kind=link}

Source: Seeking Alpha

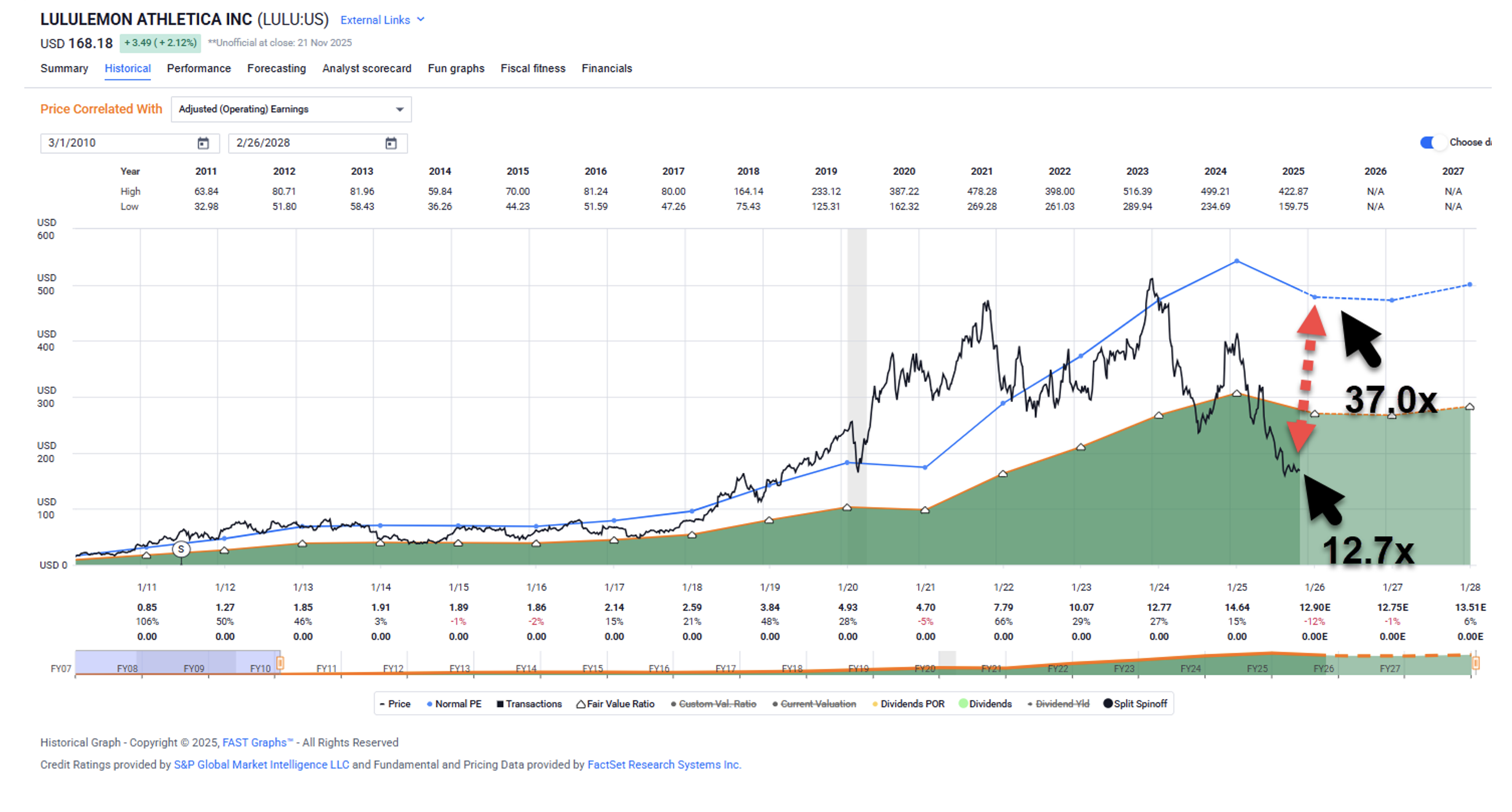

In terms of valuation, shares are a flat-out bargain. They’re trading with a 12.7 times price-to-earnings (P/E) multiple compared with a normal (historical) 36 times.

That’s a significant margin of safety.

{kind=link}

Source: FAST Graphs

Consider peers like Nike (NKE) and Under Armour (UAA). Both are trading at around 31 times while spending intense amounts of marketing money through big names like Carmelo Anthony, Tiger Woods, and LeBron James.

While Lululemon has recently begun signing on NFL players to its brand, it still very much relies on a much cheaper ambassador program that utilizes local influencers and outstanding yoga instructors.

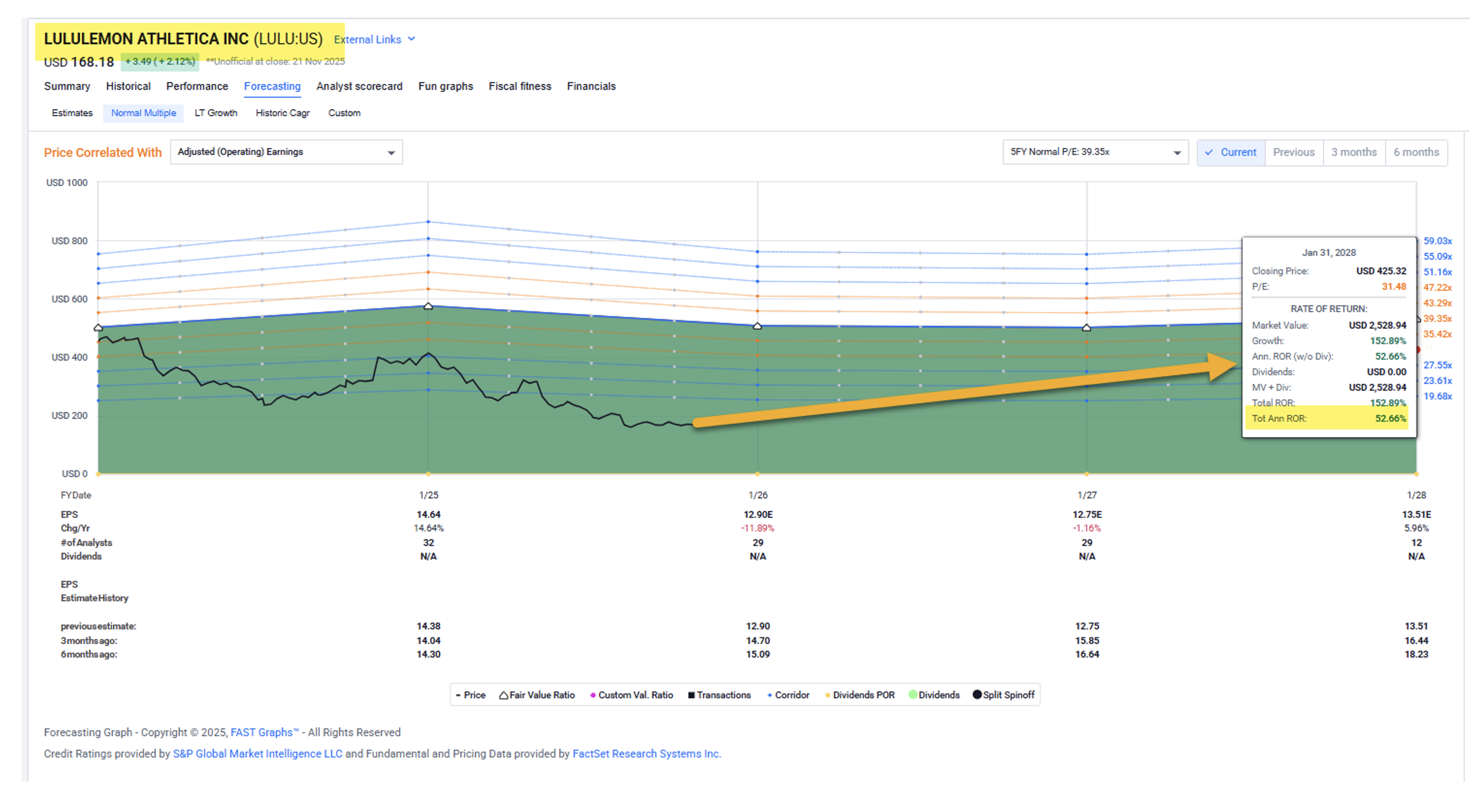

In short, I see value in this overly punished retailer. Shares have fallen 55% year to date, yet Lululemon’s earnings-per-share growth is down by just 12%. And based on consensus numbers, it should see only a modest decline in earnings next year of less than 2%, followed by a return to 6% growth in 2027.

The company is fully acknowledging its missteps and seems like it’s ready to turn a new leaf.

To be clear, I don’t expect a 36 times multiple again anytime soon, and neither should you. But 30 times seems reasonable, which translates into a total return setup of 50% on an annualized basis.

{kind=link}

I’m not a big fan of many retail brands right now. However, Lululemon has carved out a decent moat that’s worth considering.

As the father of four daughters, I am very familiar with the potential behind Lululemon. Let’s just say I’ve helped ring the cash register for them on more than one occasion.

Perhaps more than I want to count…

So, when I see it trading so low with such noteworthy metrics, I see a significant opportunity to recoup those losses.

That’s why I’m adding Lululemon to my Black Friday shopping list.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|