Usually, not much happens in Saline Township.

Located in Washtenaw County, Michigan, it’s about 35 miles outside of Detroit and home to some 2,300 residents. Saline is mostly agriculture, quiet streets, and not much else…

It’s not the sort of place you’d expect to be a flash point for major controversy. But last year, that’s exactly what it was. In November 2025, citizens of Saline packed the modest township hall. And they were furious.

One resident didn’t mince words:

Nobody is here to protect us! I am angry. And maybe you can’t do anything about it, but I am angry that you didn’t fight harder.

They were all there to protest a new data center set to be built in their quiet little town. A big concern was rising electricity costs.

Saline is not alone.

Monterey Park, California is about 7 miles east of downtown Los Angeles. Approximately 58,000 people call it home. Like Saline, residents flooded into the city hall recently. Also, like Saline, they were furious about a proposed data center.

I could go on…

The AI backlash is well and truly here. And while the economic benefits will almost surely outweigh the concerns, these residents do have a point…

Under Strain

Last year, executives from tech giants OpenAI, Microsoft (MSFT), CoreWeave (CRWV), and Advanced Micro Devices (AMD) told the Senate that the U.S. power grid is incapable of handling AI’s soaring energy demands.

Microsoft president Brad Smith put it this way:

America’s advanced economy relies on 50-year-old infrastructure that cannot meet the increasing electricity demands driven by AI, reshoring of manufacturing, and increased electrification.

They emphasized how slow permitting processes and outdated grid infrastructure are already hampering deployment for data centers and related infrastructure.

In short, we need more energy production if we’re going to stay competitive.

That’s why utilities are the hot stocks now. This typically sleepy industry is ramping up capital spending to meet growing demand.

Yet utilities still remain a lower-risk way to play the AI boom. And they come with tidy dividends to boot.

Here are a few I’m keeping an eye on…

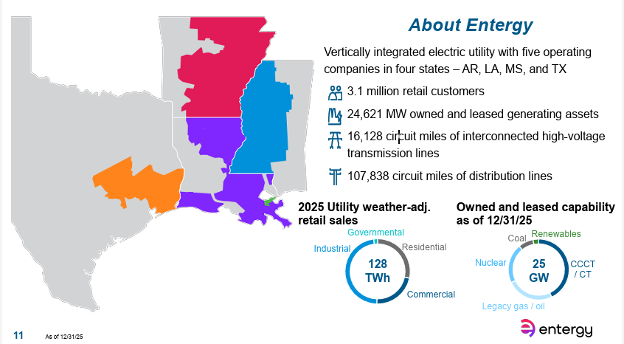

Entergy: The Industrial Engine of the Gulf South

{kind=link}

Source: Entergy Q4 2025 Earnings Presentation

First up is Entergy (ETR), a regulated utility that serves approximately 3.1 million customers in Arkansas, Louisiana, Mississippi, and Texas. Like other parts of the U.S., this region is experiencing an industrial gold rush driven by data centers.

Meeting this growing demand is precisely what led management to unveil a $43 billion capital spending plan through 2029 – mere months after proposing “just” $41 billion. Entergy knows the demand is there.

It also knows how profitable this build-out can be. That’s why it reiterated its guidance for 8%-plus annual adjusted earnings-per-share (EPS) growth through 2029, off a 2025 base of $3.91.

ETR boasts a BBB+ S&P credit rating with a stable outlook, which gives it better access to low-cost capital. And it offers a 2.4% dividend yield, which comes in at about double the S&P 500 Index’s 1.1% yield.

Its dividend is backed up by an adjusted EPS payout ratio that’s likely to be in the high- 50% range this year, allowing it to extend its 11-year growth streak.

Trading at a forward 12-month price-to-earnings (P/E) ratio of 22.3x from its current $104 share price, shares are probably a bit rich after rallying 13% so far in 2026. But we’ll be watching it closely to see if any hiccups take it down closer to 20x.

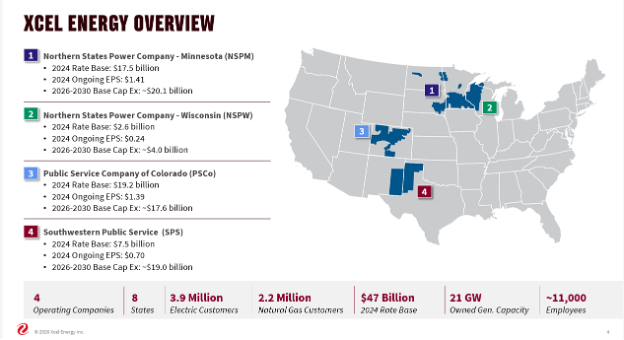

Xcel Energy: A Multiregional Powerhouse for the AI Era

{kind=link}

Source: Xcel Energy January 2026 Investor Presentation

Xcel Energy (XEL) is a regulated electric and natural gas utility that serves millions of customers in eight states. As with ETR, this electric and gas utility is cashing in on the AI and data-center infrastructure bonanza.

Late last year, XEL revealed a $60 billion capital investment plan for 2026 through 2030… in addition to a $10 billion (and counting) pipeline of infrastructure investments. This was a pronounced increase from the prior $45 billion five-year capital spending plan.

Behind this capex explosion is:

-

2 gigawatts (GW) of data centers either contracted or under construction

-

Another 4 GW of highly probable data centers

-

More than 20 GW of additional data-center opportunities in the pipeline.

That’s why XEL thinks it can deliver 9% average annual ongoing diluted EPS growth through 2030.

The utility sports a BBB+ S&P credit rating with a stable outlook and a 2.8% dividend yield. Its ongoing diluted EPS payout ratio is poised to be in the high-50% range in 2026 to support that payout.

Incidentally, XEL has already established a 22-year dividend growth streak, meaning it’s well on its way to becoming a Dividend Aristocrat at 25 years.

At just under $81 a share, it looks like a decent value despite its 9% rally year to date. Shares are trading at a forward 12-month P/E ratio of 19.3x, which is below the 10-year average of 20.6x. It’s also about 4% under our fair-value estimate of 20x, or $83 per share.

NextEra Energy: The Dividend Aristocrat Powering the AI Boom

{kind=link}

Source: NextEra Energy December 2025 Investor Presentation

As the country’s largest electric utility, NextEra Energy (NEE) remains the heavyweight of its industry. Its Florida Power & Light (“FPL”) subsidiary alone, which accounts for about two-thirds of its operating revenue, serves over 6.1 million customer accounts.

The other third is derived from NextEra Energy Resources. This wholesale energy provider is a world leader in renewables, selling much of its power to other utilities, municipalities, and large companies across North America.

NEE estimates that every GW of demand is equivalent to another $2 billion of capital expenditure (“capex”). This earns 9.95% to 11.95% return on equity, the same as other FPL investments.

Florida’s economic and population growth, combined with NEE’s data center build-outs, bode well for the utility’s future. It anticipates that adjusted EPS through 2032 will grow at an 8%-plus rate, and it’s targeting the same expansion through 2035.

Better yet, NEE has the balance sheet to shape this vision into a reality with a stable A- S&P credit rating.

The company hiked its quarterly dividend 10% earlier this month, which currently makes for a 2.4% yield. That means it has boosted its dividend for three full decades now. And we expect that streak to continue under NEE’s low-60% payout ratio range for the year.

Our only issue is that, after a 15% year-to-date rally, NEE is no longer a bargain. Then again, it’s not excessively expensive, either.

At its current share price of $93, it’s sitting at a forward 12-month P/E ratio of 22.8x. This is still a bit below its 10-year average P/E ratio of 24.2x.

So, our assessment here at Wide Moat Research is that while you wouldn’t be foolish to buy it where it’s at… we’re going to wait for a pullback before we dive in.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|