As I’ve said before, and I’m sure I’ll say again, avoid “sucker yields” at all costs.

For the uninitiated, a sucker yield is a dividend yield that looks too good to be true because – more often than not – it is. Put another way, it’s a dividend that’s just begging to be cut.

But that doesn’t mean that every high-yielding stock is a sucker yield.

The best high-yield opportunities typically occur when a company has durable cash flows and a disciplined balance sheet… but it has temporarily fallen out of favor for some reason.

In the case of real estate investment trusts (“REITs”), virtually the entire sector has fallen out of favor. The S&P Real Estate Sector came in dead last in 2025 – printing only 3.2% against the S&P 500’s 17.9%.

But here’s the good news…

That relative underperformance is concealing some strong companies. And the temporarily depressed share price means they have generous yields that are also reliable.

If we are in the early innings of a REIT Renaissance, then there’s a good chance these yields won’t be this high for long. Today, I thought we might have a look at some high-yielding REITs that can still let you sleep well at night.

What’s Up, DOC?

Healthpeak Properties (DOC) is a health care REIT that owns 673 properties, including:

-

524 outpatient medical office buildings (“MOBs”)

-

115 life-science properties

-

34 senior housing properties

The company recently announced it was spinning off that latter collection to form a new REIT called Janus Living. Healthpeak will retain a substantial majority ownership in this venture, making the remaining shares available in an IPO that will probably take place before July.

Healthpeak will also serve as Janus’ external manager. This involves a $10 million annual management fee under an initial three-year term, with successive one-year renewal periods after that… all while receiving a pro-rata share of regular distributions.

So it’s no wonder that Healthpeak sees no problem with continuing its annual $1.22-per-share dividend after the IPO.

Now, a primary reason for the spinoff is that, based on DOC’s current valuation, it isn’t being rewarded for its premium housing assets as-is. Shares currently trade at 10.2 times compared with 40.5 times for Welltower (WELL), a pure-play senior housing REIT.

That enormous difference doesn’t make sense considering how Healthpeak’s MOBs and life-science buildings generate steady and predictable income. The company just reported earnings last night.

In the fourth quarter of 2025, funds from operations (“FFO”) per share was $0.47, exceeding consensus estimates of $0.46. For fiscal year 2025, adjusted FFO (“AFFO”) per share was $1.69 compared with an annualized dividend amount of $1.22 per share (payout ratio of 72%).

For all of 2025, Healthpeak saw new lease executions of 562,000 square feet and renewal lease executions totaling 889,000 square feet with 72% retention and up 5% cash releasing spreads on renewal.

But, as I wrote two months ago concerning pureplay life-science landlord Alexandria (ARE)… the life-science space has been hit hard with oversupply, even causing that impressive company to cut its dividend last year. So Healthpeak is suffering from association.

What critics don’t realize is that it’s actually held up decently despite the drama. Not perfectly, mind you, but decently.

For the record, Healthpeak’s fourth-quarter earnings did beat expectations. But lab occupancy declined 390 basis points (“bps”) sequentially on a backend-loaded basis to 77.1%.

The REIT issued guidance for the year as well, missing The Street’s adjusted FFO projection by 5.5%. And same-store life science NOI guidance specifically is now down 7.5% year over year.

On the plus side, DOC expects lab occupancy to pick up in the second half of 2026 with around 1.5 million square feet of leasing in its pipeline.

As the FAST Graphs chart below shows, DOC trades at 10.2 times price to AFFO (P/AFFO) compared to its normal 16 times multiple. At least it was trading that way last night. I’m sure the earnings news will have a further negative impact on its shares.

However, this all represents an attractive margin of safety – and with a well-covered 7.1% dividend yield to boot.

Just keep in mind that the actual company isn’t expected to grow much either this year – or next. As such, my best-case forecast is that DOC will return 20% in 2026 between its dividend and price appreciation.

{kind=link}

Source: FAST Graphs

I plan to interview Healthpeak’s management team later this week, information I’ll exclusively share with my Wide Moat Letter members.

Never Bet Against Vegas

VICI Properties (VICI) is a net-lease REIT with a target niche investing in experiential properties. Since Caesars Entertainment (CZR) spun VICI off during its bankruptcy reorganization, it’s become quite the growth story.

A world-leading gaming and experiential REIT, it boasts:

-

54 gaming properties

-

39 other experiential properties

-

13 tenants

-

Eight additional financing partners

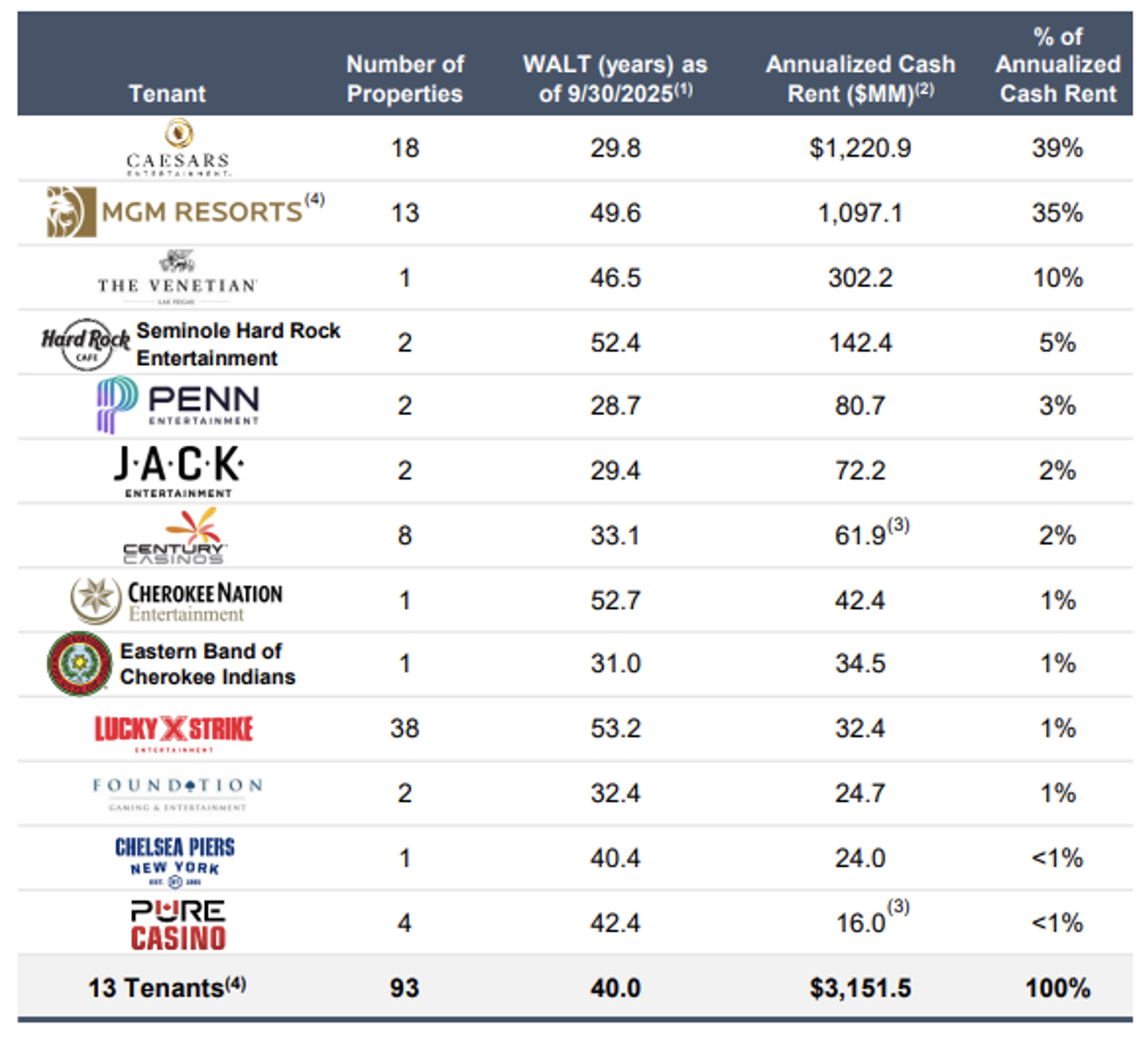

As shown below, VICI has a diversified asset base, though with outsized exposure to three large gaming tenants. Caesars generates 39% of its revenue, MGM Resorts (MGM) accounts for 35%, and The Venetian another 10%.

{kind=link}

Source: VICI Properties

So it does face concentration risk. However, it also boasts multiple holdings in one of America’s most valuable, supply-constrained locations: The Las Vegas Strip.

This space is built out. You cannot create new comparable assets there without knocking something else down.

VICI owns 10 trophy assets on the Strip, including 660 acres of underlying land, 41,400 hotel rooms, and 5.9 million square feet of conference, convention, and trade show space.

It also owns 26 acres of undeveloped land strategically located adjacent to The LINQ and behind Planet Hollywood, as well as seven acres of Strip frontage property at Caesars Palace. All of these are subject to and part of a master lease with Caesars.

Here’s another thing going for VICI: Whether in or outside of Vegas, gaming licenses create regulatory barriers that keep competitors at bay. Casino operators must obtain state gaming licenses and comply with strict approval requirements… conduct background checks… and undergo regulatory oversight.

Put simply, you can’t just open up a new Caesars Palace across the street.

Also, VICI’s leases are typically signed for 30 to 50 years. They’re triple-net, too, which means the tenant pays taxes, insurance, and maintenance. That gives the REIT bond-like income, inflation protection, and minimal landlord responsibility.

In fact, VICI’s general and administrative expenses (G&A) as a percentage of revenue were just 1.6% in the third quarter of 2025. That’s the lowest you’ll find among its net-lease REIT peers.

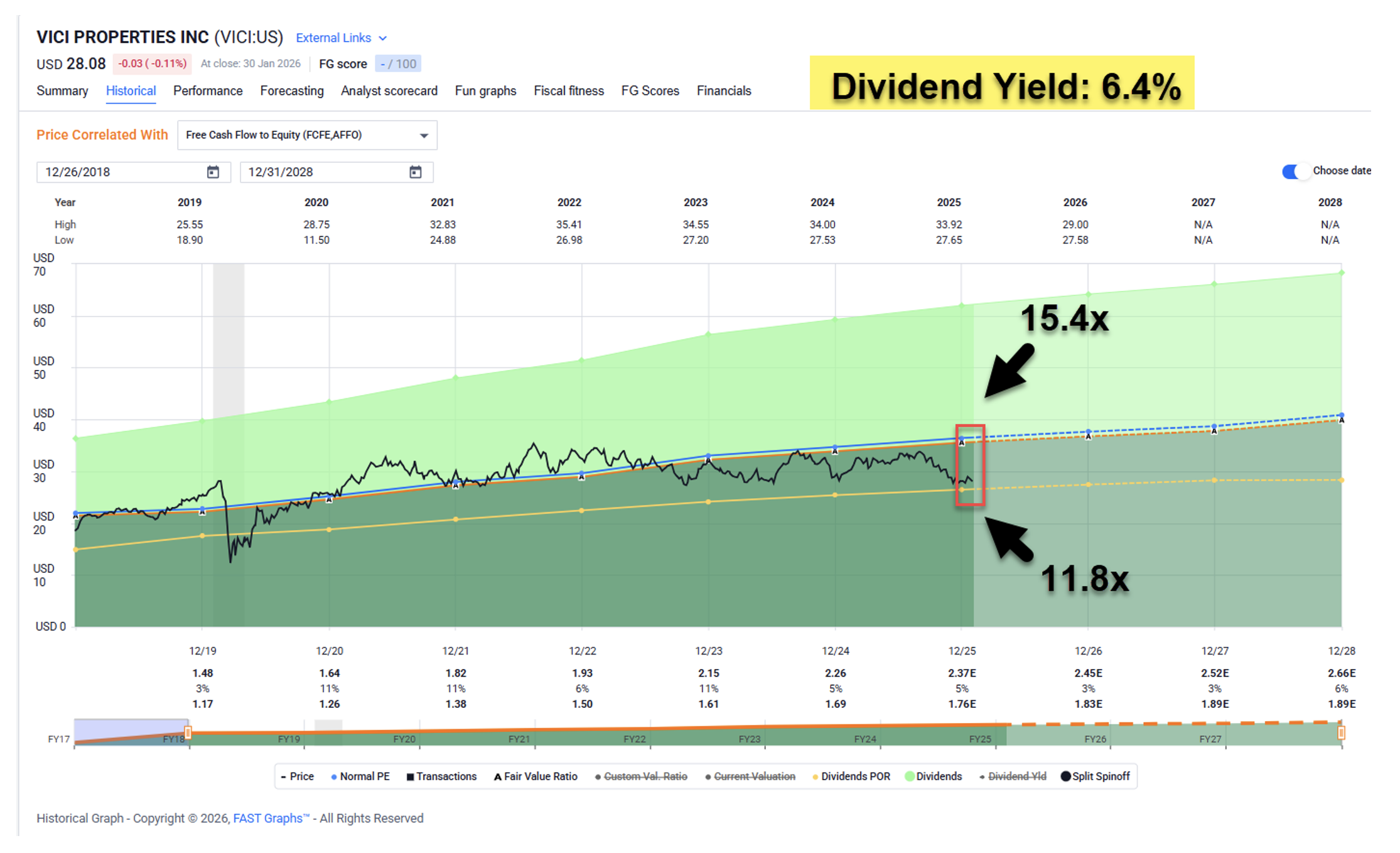

Yet VICI shares are underperforming, trading at 11.8 times compared with their normal 15.4 times. This gives it a 6.4% dividend yield with a 75% payout ratio (using AFFO per share).

The primary reason for this devaluation is because of consumer sentiment in Las Vegas. Specifically, Ceasars has experienced a 28% decline in earnings before interest, taxes, depreciation, amortization, and restructuring or rent costs ("EBITDAR") since 2021. Compared with 13% rent increases, coverage ratios have declined to 1 times.

That has left many investors nervous about where its landlord stands.

I visited VICI’s headquarters in New York City a few weeks ago to meet with the management team about all of this. As they pointed out, the leases in question are master-leased and corporately guaranteed by Caesars Entertainment.

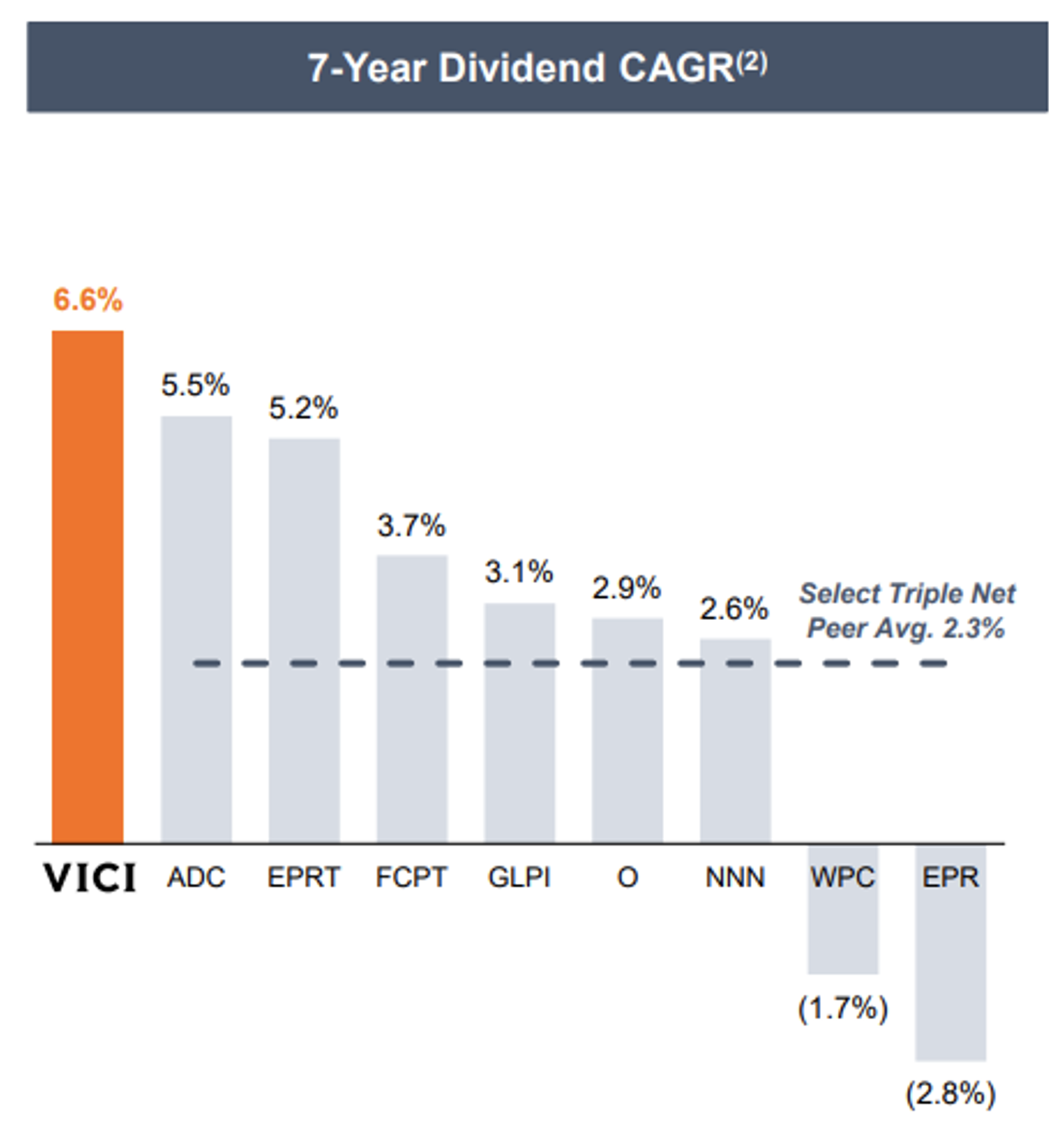

Plus, VICI has taken prudent steps to maintain a disciplined balance sheet (rated BBB- by S&P and Fitch, and Baa3 by Moody’s). It’s also proud of the fact that it has consistently grown its dividend at a 6.6% compound annual growth rate (“CAGR”) since inception – the highest in the net-lease REIT sector.

That’s a track record it takes very seriously and works very hard to build upon.

{kind=link}

Source: VICI Investor Presentation

As a result, I believe VICI’s underperformance is a buying opportunity. Analysts forecast growth of 3% in 2026 and 2027. Between that, its 6.6% yield, and 15% discount, we estimate shares could return 25% over the next 12 months.

{kind=link}

Source: FAST Graphs

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Tune into the Wide Moat Show on YouTube this week. My co-host, Nick Ward, and I will feature five high-yielding opportunities in all that you won’t want to miss.

|