‘Tis the season to get a bit nostalgic.

It’s the end of the year, so it’s natural to think over everything that has taken place over the past 11 months. But today, my memories are going much further back than that… to over 25 years ago, when I was a young real estate developer.

That’s when I was building free-standing properties for customers who wanted visibility, high traffic, and no direct neighbors.

Unlike shopping centers, free-standing buildings are typically customized by the tenant. This is often down to the last detail, including identifiable branding and signage.

For example, I built dozens of video stores for chains like Blockbuster Video, Hollywood Video, and Movie Gallery back then – all once prominent retail chains that were easily identified by their color schemes and logos.

Dollar stores like Dollar General, Dollar Tree, and Family Dollar… auto-parts companies like Advance Auto Parts… big-box chains like Walmart, Barnes & Noble, and PetSmart… restaurants like IHOP, McDonald’s, KFC, and Outback…

I helped them expand their portfolios while I gained valuable experience in site selection, corporate finance, lease negotiations, and brand building. These are essential skills I still use today here at Wide Moat Research.

This was also the time I learned to appreciate net-lease properties. Most of these free-standing properties were on a triple-net lease. And that meant the landlord could avoid the aggravation of the three Ts: taxes, toilets, and tenants.

You see, when tenants sign a triple-net lease, they automatically take on the burden of paying property taxes and insurance, and handling their own maintenance and utilities, including snow removal and fixing the toilets. Better yet, they tend to do so long term: 10, 15, or 20 years, with options to renew. That means the landlord doesn’t have to hunt for and sign a new tenant every year or two, which can be common in residential and multifamily properties.

That means the net-lease real estate investment trust (“REIT”) sector is one of the most stable, predictable ones you’re going to find. So much so that I refer to it as “the ultimate sleep-well-at-night” trade.

And today, we’ll give them a closer look.

The Growing Story of Net Leases

The net-lease sector has done a lot of evolving since I actively built for it. It now includes categories such as:

-

Casinos

-

Data centers

-

Sports facilities

-

Hospitals

-

Skilled-nursing properties

-

Amusement parks

-

Health/fitness facilities

That means the addressable universe of free-standing properties in the U.S. alone is around $5.5 trillion – of which publicly traded REITs own just 4%. The property sector is one of the most fragmented and, therefore, the ripest for consolidation.

We’re already witnessing a rapid increase in volume within the sector. I covered yesterday how asset managers like Blue Owl (OWL) are leasing back massive data centers to Big Tech players like Meta Platforms (META).

But mortgage REITs, or mREITs, are also getting in on the action. Consider Blackstone Mortgage (BXMT) and Starwood Property Trust (STWD), both of which are lining up deals to capitalize on the explosion in the net-lease sector.

The wave of deal flow can be measured further by the latest third-quarter earnings, with Realty Income (O) – the dominant player with 15,500 properties – increasing its annual acquisition guidance from $5 billion to $5.5 billion. It says it already sourced around $97 billion in 2025, eclipsing its last record of $95 billion, set in 2022.

The smaller but still formidable Agree Realty (ADC) also increased its 2025 investment guidance to between $1.5 billion and $1.65 billion. This represents more than a 65% increase over 2024 at the midpoint.

All the same, we never want to look at a sector and think it’s all investable. There will always be winners and losers, and we want to align with the winners. Obviously.

Always insist on quality and value whenever you want to truly sleep well at night. That’s our motto, and we’re sticking with it.

Two Net-Lease REITs to Avoid

At Wide Moat Research, one of the things we do best is separating the wheat from the chaff. And two of the best indicators of quality in the net-lease REIT sector are earnings and dividends.

(Incidentally, Monday’s article explained the best methodology for analyzing REIT earnings: adjusted funds from operations, or AFFO.)

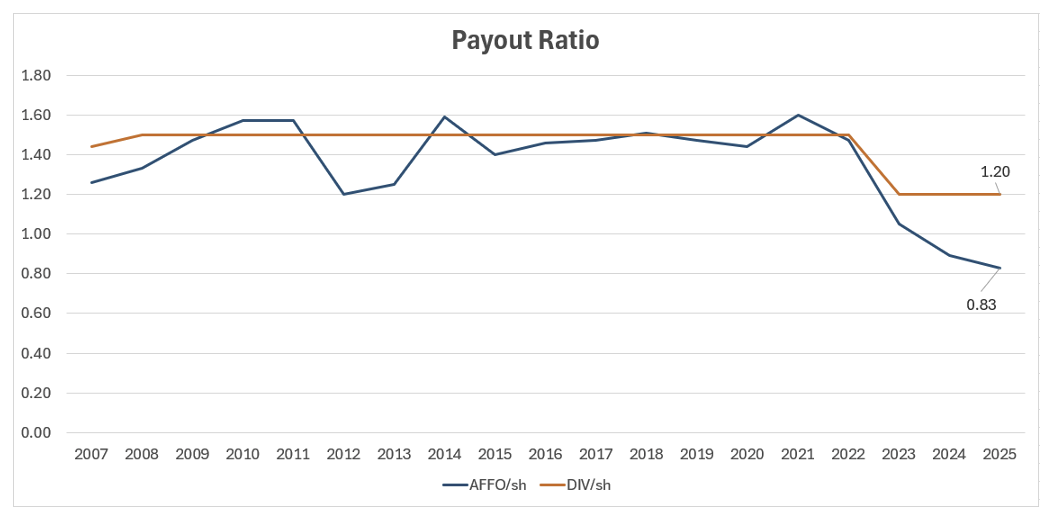

Unfortunately, neither look good for Gladstone Commercial (GOOD), a smaller net-lease landlord that has done very little in creating shareholder value. It has generated no earnings growth and zero dividend growth, as represented by the blue and orange lines, respectively, in the graph below.

{kind=link}

Source: Wide Moat Research

The company cut its dividend in 2023 and is right back on our dividend-cut watchlist today, given its elevated payout ratio. While its 10.6% dividend may seem attractive, we suggest avoiding this “sucker yield.”

It’s just not worth it.

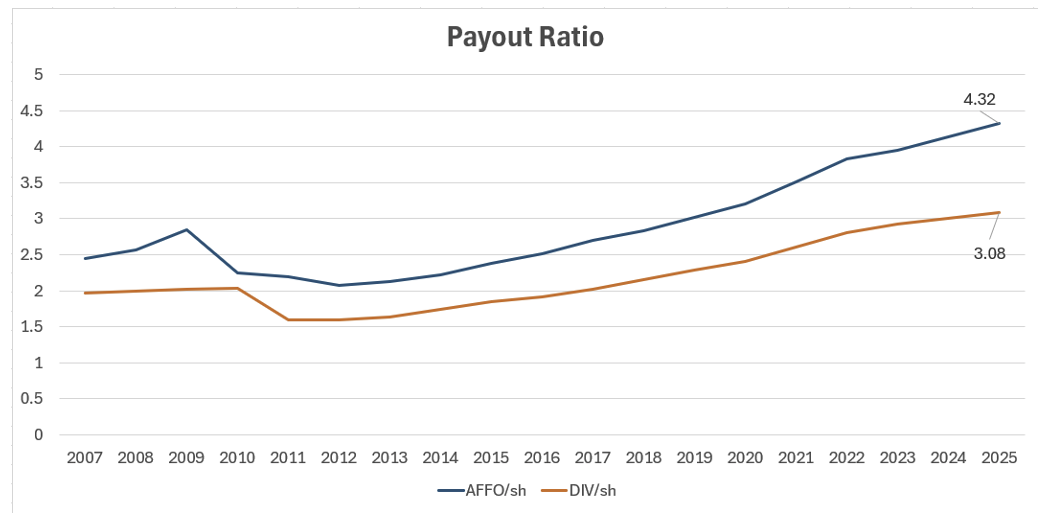

The same goes for Global Net Lease (GNL), which has a market cap of around $1.7 billion. Founded in 2015, it’s been an absolute train wreck, with deteriorating earnings (blue line) and a chronic history of dividend cuts (orange line).

{kind=link}

Source: Wide Moat Research

Once again, GNL’s 9.7% dividend yield may look tempting. But I see no indication that there’s any value creation thesis here that warrants investor capital.

Again, I’m avoiding it at all costs.

Stick With the Winners

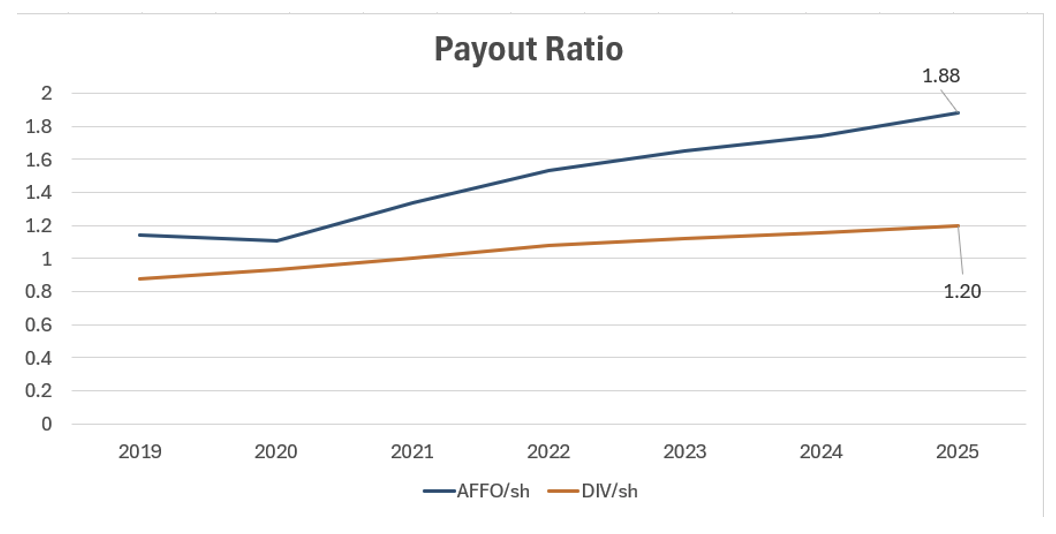

Agree Realty, however, is the net-lease sector’s “comeback kid.” Though it cut its dividend in 2010, it has since reincarnated into a highly diversified REIT with a rock-solid balance sheet.

I credit management for becoming disciplined and rewarding investors with sector-leading growth. And that comes complete with a 4.7% dividend yield and one of the lowest payout ratios in the sector.

{kind=link}

Source: Wide Moat Research

Essential Properties Realty Trust (EPRT), meanwhile, listed in 2018 and continues to generate sector-leading growth. It maintains a respectable balance sheet while generating the widest investment spreads.

And while its dividend yield is just under 4%, EPRT has the lowest payout ratio (64%) in its peer group. So that dividend is about as safe and secure as can be.

{kind=link}

Source: Wide Moat Research

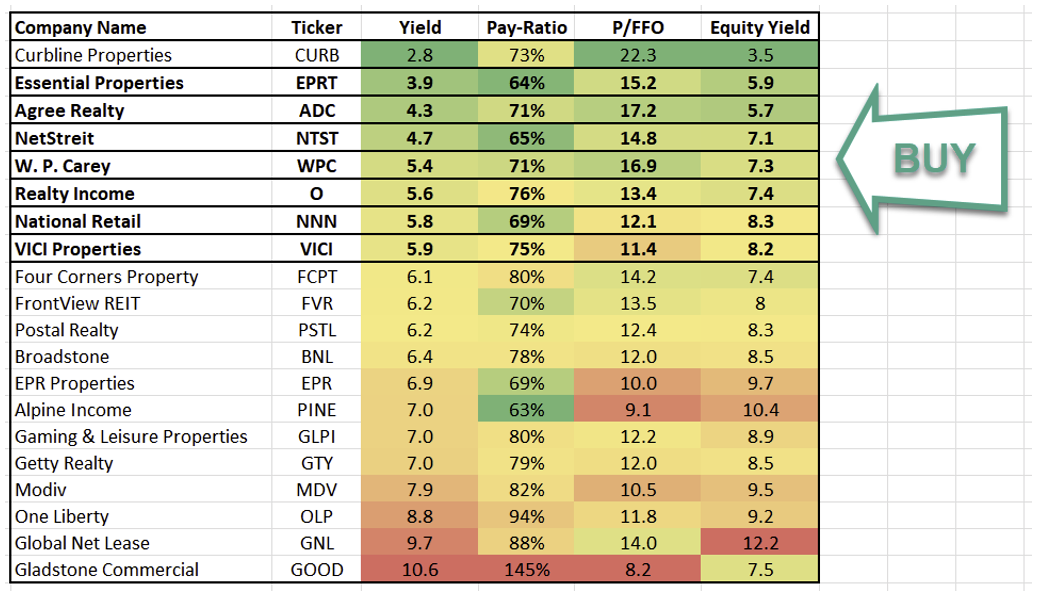

The larger net-lease REIT sector looks very investable right now, especially as interest rates decrease, reducing their cost of capital. Wide Moat Research considers now an optimal time to allocate capital into this space.

Just as long as you don’t get too cute by chasing unsustainable yield. In which case, this last chart should help you out with that.

{kind=link}

Source: Wide Moat Research

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. I recently interviewed Chris Volk, a leading expert in net-lease investments. He founded and ran three different publicly traded REITs, and once even convinced Berkshire Hathaway (BRK.A)(BRK.B) to invest in Store Capital before the company eventually went private.

Be sure to watch my entire interview with Volk tomorrow on my YouTube channel, The Wide Moat Show.

|