At first glance, farmland seems like a simple investment thesis…

You own productive land. You lease it to farmers. You collect rent that’s directly (or indirectly) tied to food production.

It sounds simple.

That’s because it is simple.

But that doesn’t mean it’s always easy.

Productive farmland is dependent on a global support system of technology, natural resources, and production. As such, it can and is negatively affected whenever there are:

-

War-driven energy shocks

-

Fragile agricultural economics

-

Private credit issues…

All of which we’re unfortunately seeing today.

The conflict with Iran, for instance, may or may not be winding down. We just don’t know yet. But it has already triggered one of the largest energy disruptions in modern history.

Agriculture relies on oil products for fueling farm equipment and transporting foodstuffs to manufacturers, storage facilities, and grocery stores. Plus, gas is a key ingredient in nitrogen fertilizer, which has nearly doubled in price in some cases.

In short, every stage of the food creation process has been affected.

This matters to the farmland real estate investment trusts (“REITs”) I follow. Naturally, if their tenants must pay more to grow what they grow, they have less money to put toward their rent.

And that’s not where the problems end for these landlords. Not when private credit markets have simultaneously begun to show signs of stress.

Stephen Hester gave his assessment on the private credit situation a few weeks back. But suffice it to say that the private credit industry lent heavily to software companies over the past several years. That latter industry is under stress, with fears that artificial intelligence (“AI”) will make their products obsolete. Fear is bleeding over into the private credit firms that lent to those software businesses.

Now, banking insiders are increasingly warning that any further geopolitical or market stressors could take private credit structures down a notch or two. None of that is the fault of farmers or agriculture landlords. But it is what it is.

That’s a topic I’ll be tackling soon. It’s too important to ignore.

But for today, let’s acknowledge that farmland is an attractive – but complicated – asset that needs to be studied carefully before we invest in it.

Gladstone Land: The Beverly Hills of Farmland

Within the U.S., there are approximately 874 million acres of farmland worth around $3.7 trillion. That makes it one of the largest real estate sectors the country has to offer.

The two publicly traded farmland REITs, however, represent less than one-tenth of 1% of that value. Farmland Partners (FPI) owns about 71,600 acres with a $478 million market capitalization, while Gladstone Land (LAND) has around 99,000 acres with a $420 million market cap.

Each one has its own focus, with LAND owning specialty, location-sensitive crops such as almonds, berries, and vegetables. The farms it features tend to be more productive per acre but also more dependent on water.

That latter aspect is a risk, of course. But on the plus side, LAND does tend to purchase sites – mostly in California and Florida – that are situated near significant population hubs. This gives it distinct logistics advantages in the form of easy access to fresh produce supply chains.

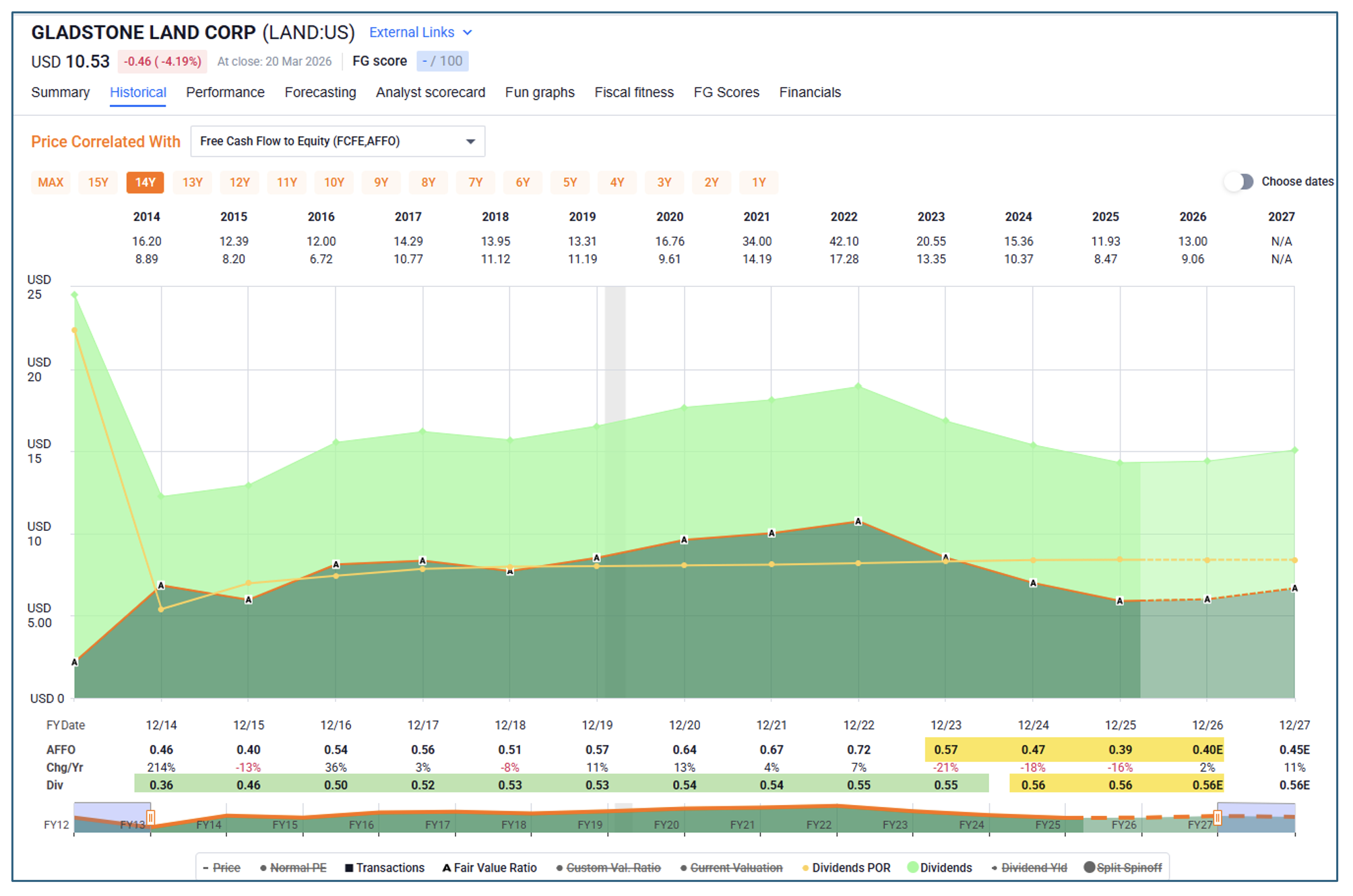

The REIT, which is externally managed by the Gladstone Companies, was founded in 1997 and had its stock market debut in 2013. It was able to grow its earnings in the form of adjusted funds from operations (“AFFO”) per share quite nicely, as shown below.

But, also shown below, that happy situation began to take a turn for the worse in 2023 – enough so to put its dividend at risk. And by the close of last year, its AFFO per share-based payout ratio had climbed to a very worrisome 140%.

{kind=link}

Source: FAST Graphs

That’s never a good look for any REIT, farmland or otherwise.

Wide Moat Research does understand that LAND’s 5.3% dividend yield might look a little tempting. But we are concerned that its current payout is unsustainable.

So we can’t in good conscience recommend it – even though we will continue to monitor its progress (or lack thereof) from here.

Farmland Partners: A Great American Farming REIT

Moving on to Farmland Partners, it was founded in 2007, went public in April 2014… and takes a different approach to agricultural “landlording” compared with Gladstone.

You could say it represents the more recent wave of farmland financialization since it focuses on row crops such as corn, soybeans, and wheat. Its portfolio, therefore, runs across both the Midwest and Southeast, where growing conditions are more optimal for such produce.

This might not be the flashiest way to farm, but FPI’s crops are deeply liquid with easily understood institutional value. It might not harness the power of premium pricing like LAND, but its business is based on scale, diversification, and resilience.

Or, to put it another way, you’re not betting on California strawberries when you invest in FPI. You’re backing global food production. This creates a different kind of defensive moat altogether, based on need rather than scarcity.

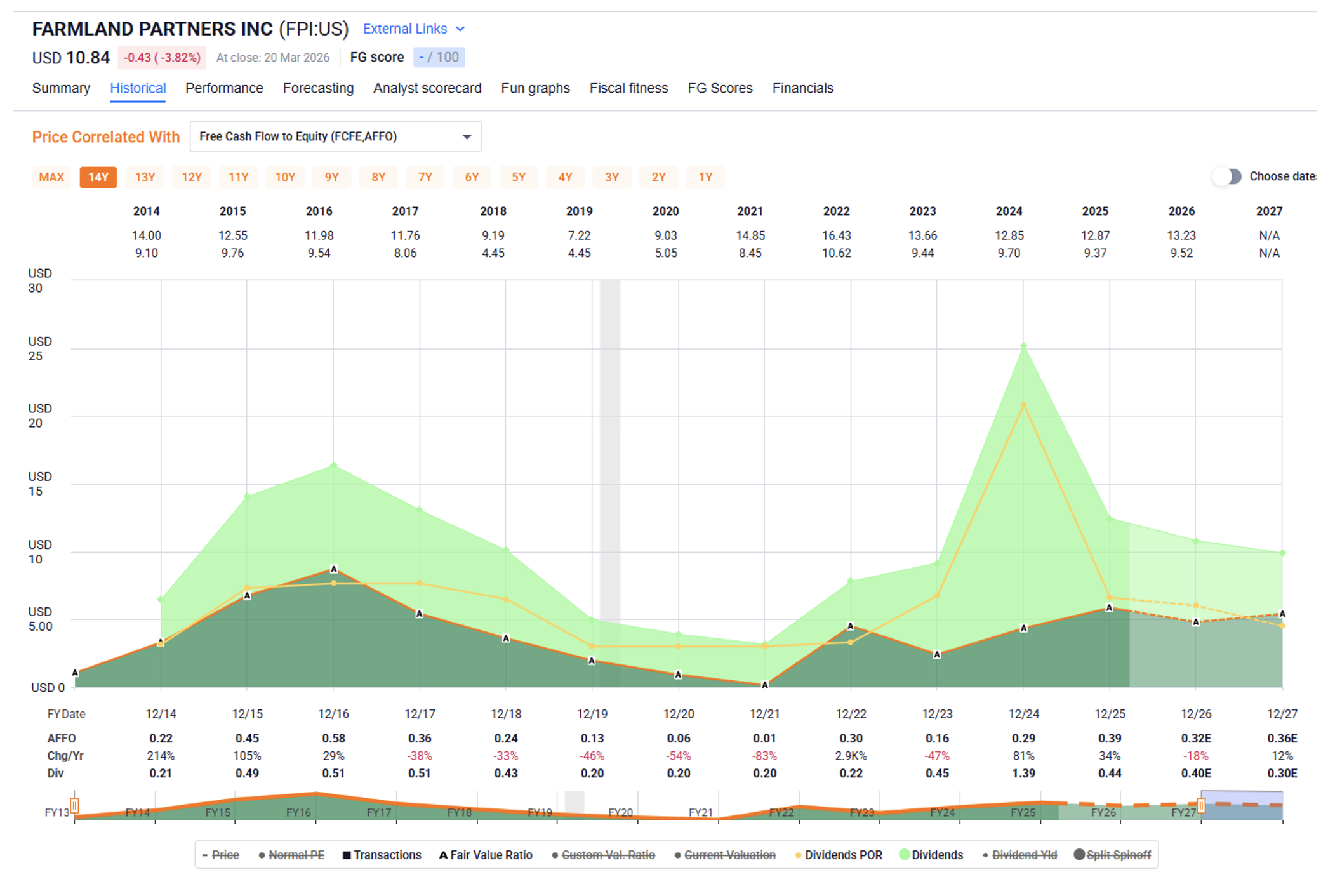

Now, it’s hard to talk about FPI without at least briefly mentioning the short-seller attack it faced around 2018. That was when an anonymous writer on Seeking Alpha accused it of inflating its farmland values and misleading investors on its net asset value (“NAV”).

This attack triggered a single-day 40% collapse in FPI’s share price that took it years to claw back. You could even argue that the fallout – which included a prolonged legal battle – is still affecting it today.

{kind=link}

Source: FAST Graphs

Still, Farmland’s most recent price decline is definitely due to increased fertilizer prices and tightened farm margins.

On the plus side, CEO Luca Fabbri reported last month that the REIT had a “very, very strong the fourth quarter in the context of a very strong year.” So much so that FPI boosted its quarterly dividend by 50% to $0.09 per share.

AFFO was $17.9 million for 2025, and $11.4 million for the quarter, or $0.39 and $0.26 per weighted average share, respectively. Both were higher year over year thanks to asset dispositions, increased variable rents, higher interest income, and lower overall operating expenses.

FPI provided its 2026 outlook with a forecasted net income range of $8.8 million to $10.9 million. Its AFFO range, meanwhile, was $14.4 million to $16.4 million, or $0.33 to $0.37 per share.

That would put its midpoint AFFO per share at $0.35. In which case, its dividend would be $0.36 with a 102% payout ratio.

We do consider FPI a buy today.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|