Over 31 years ago, Alexandria Real Estate (ARE) was formed to capitalize on the biotechnology revolution. This real estate investment trust (“REIT”) decided to focus exclusively on providing lab and office space for life-science companies.

It was something nobody had done before. But Alexandria did it so well, it was able to go public just three years later. And for a long time, it was an incredible stock to hold.

{kind=link}

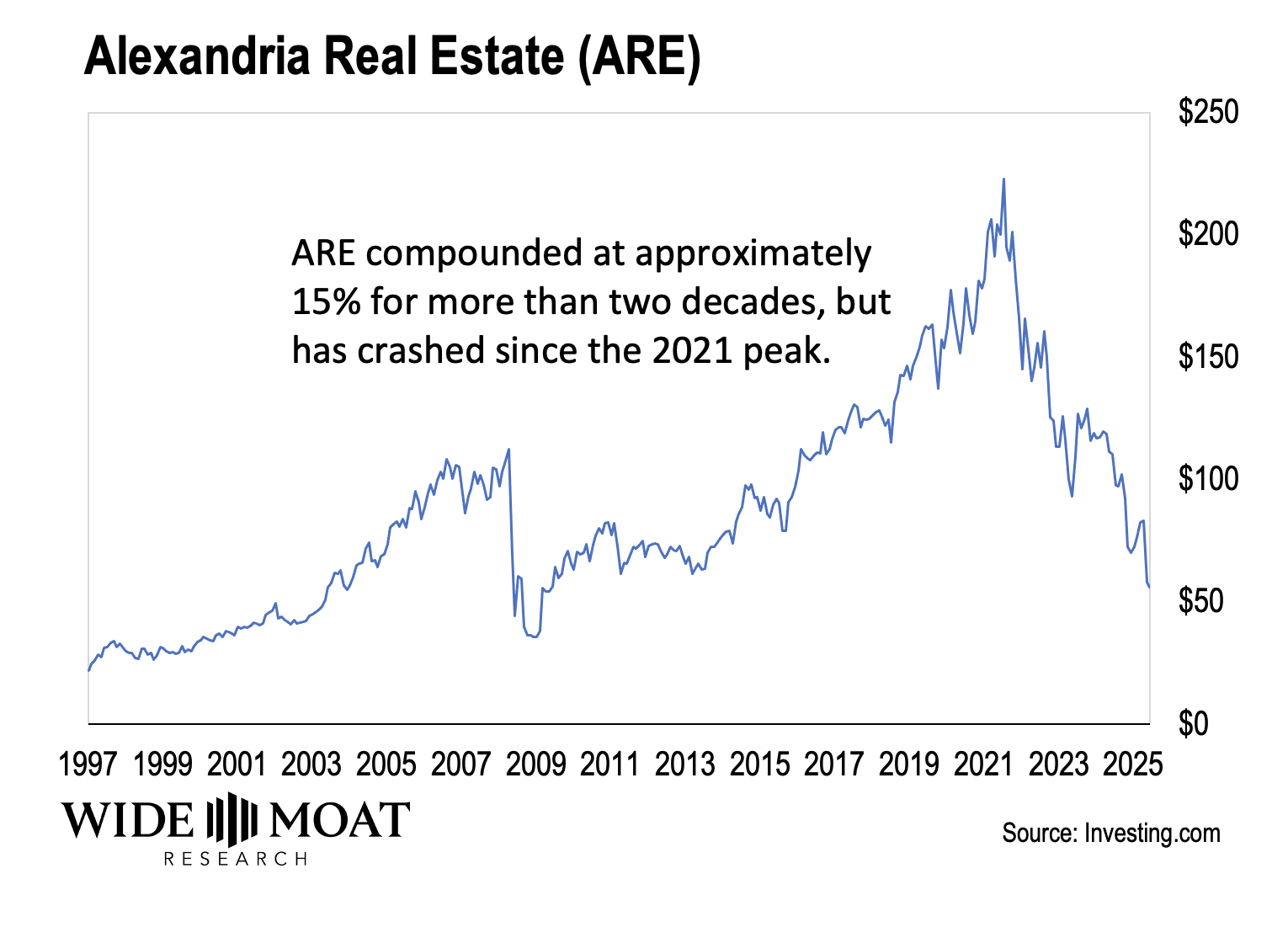

From 1997 to ARE’s peak in late 2021, the stock returned just over 2,800%. That would be approximately 15% annualized.

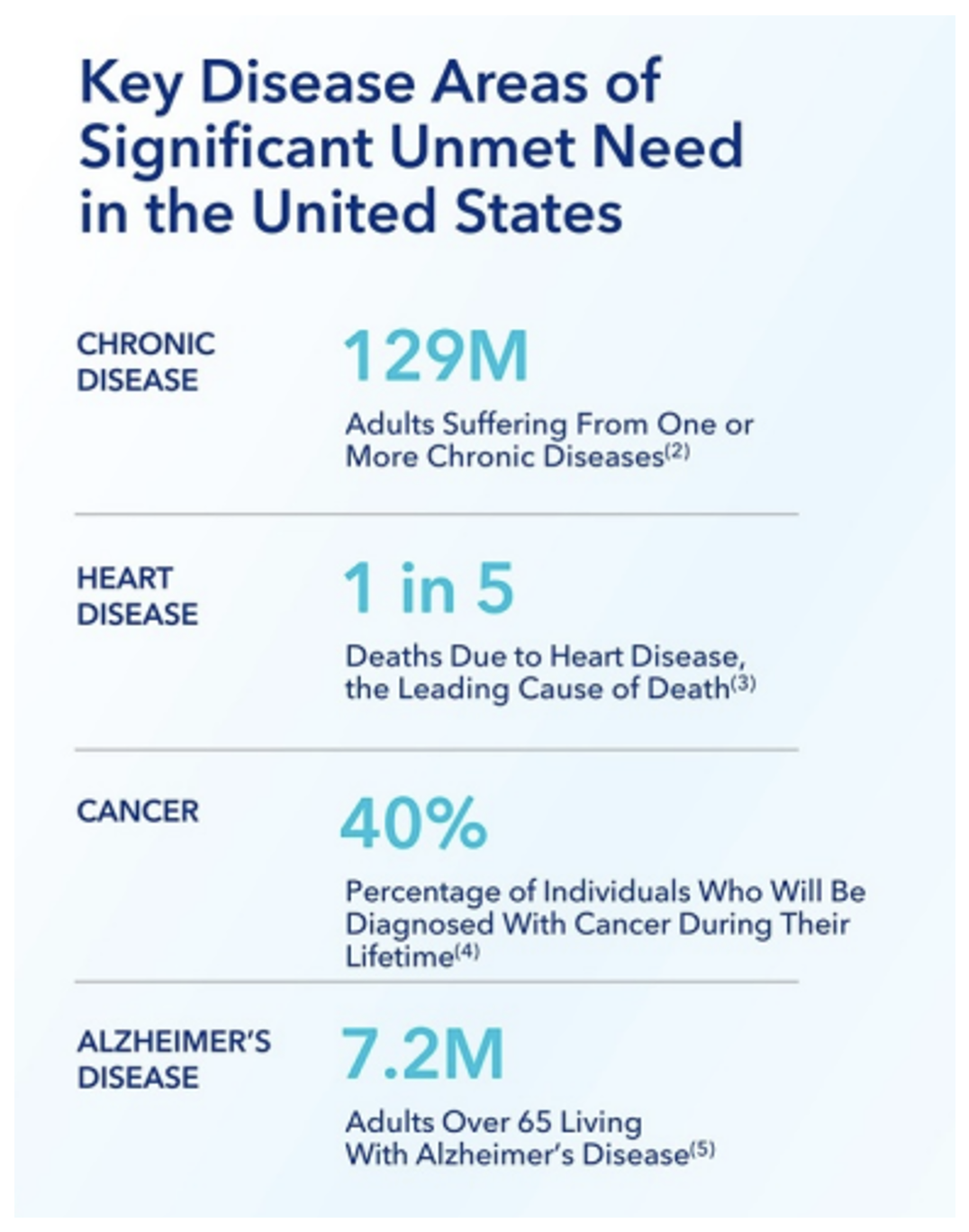

This only makes sense considering how mission-critical its clients are. There are more than 10,000 diseases known to humankind, many of which are debilitating or outright deadly.

Biotechnology and pharmaceutical companies have made significant inroads over the past 50 years. Yet there’s still so much for them to do. And Alexandria’s facilities are an important piece of that process.

So far, they’ve been able to address less than 10% of the long, long list of medical issues troubling humanity. Which means they – and their landlords – have a whole lot of shelf life left.

{kind=link}

Source: Alexandria Real Estate

We certainly saw that during the pandemic, as everyone raced to find a solution to COVID-19. And the AI-fueled technology wave has since become another dynamic catalyst that’s driving breakthrough discoveries, accelerating drug development, and producing unprecedented insights into complex medical challenges.

That heightened activity increased demand for biotech facilities, prompting developers to increase supply. Problem is, they got greedy…

So much so that nearly half the lab space completed between 2022 and 2024 remains empty today.

Even the most responsible life-science landlords have suffered as a result of that kind of foolishness. And it shows in the stock price. From its peak, the stock is down nearly 74%.

Yet Alexandria still has my vote of confidence.

In fact, I’ve rarely seen it looking so good as it does right now. And after such a bruising drawdown, it looks like a bargain at current prices.

Let’s have a closer look.

Zombie Buildings

My regular readers know I try to keep my investment analysis and advice grounded in reality. And that means acknowledging both the bad and the good.

First up is the bad.

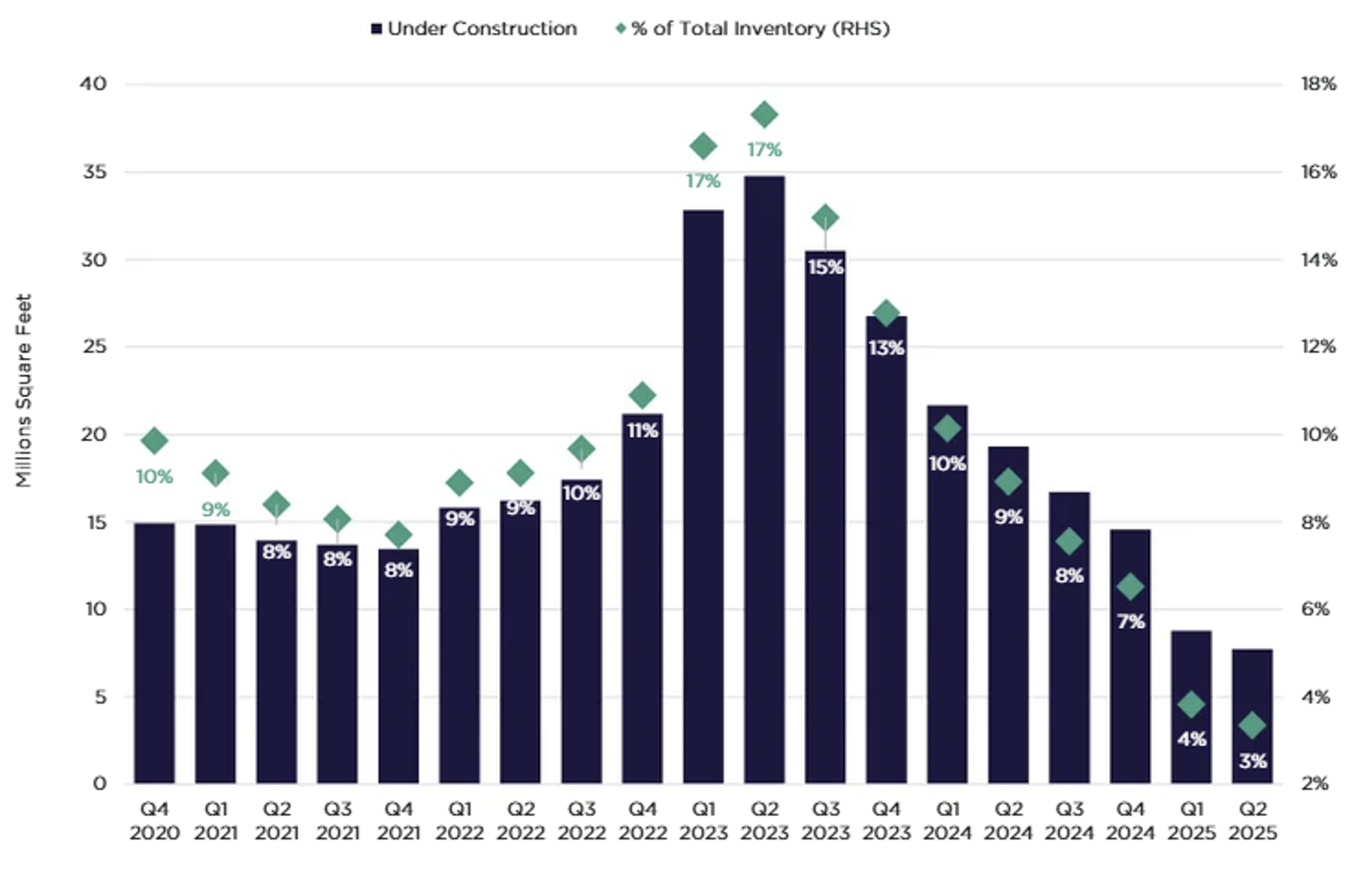

The sector’s construction pipeline peaked in the second quarter of 2023, when activity totaled 17% of existing inventory. And those numbers have been slipping ever since.

As of the second quarter of 2025, the pipeline has contracted to just 3%.

{kind=link}

Source: Cushman and Wakefield

If that seems like a shocking difference, it’s not just overbuilding at play. As Joel Marcus, CEO of Alexandria REIT, pointed out on his company’s third-quarter earnings call:

A very low-interest-rate environment went along with that, which incentivized really foolish speculation by financially motivated real estate companies and their even more foolish capital partners…

This has never happened in this niche before. But they’re learning painful lessons that this real estate niche is unique and different from all others.

It’s a straightforward argument. The COVID-19 era seemed like a gold rush for life-science properties. Combined with near-zero interest rates, and the industry got way over its skis. Too much supply was catering to too little demand. And that’s how even great operators like Alexandria were brought low.

Marcus refers to these dark life-science properties as “zombie buildings” that will have to be repurposed altogether.

He also said the life-science sector is, perhaps surprisingly, enduring the fifth year of “a biotech bear market.” And that is being exacerbated by the ongoing government shutdown, where “the impact to the FDA is pretty serious.”

You see, along with so many other federal facilities, the FDA is currently closed. So are many offices of the National Institutes of Health, which is already $5 billion behind on grant disbursements compared with 2024. Even worse, venture capital into the biotech space has dropped to its lowest level since before the pandemic.

During the first half of 2025, U.S. life-science companies raised roughly $12.7 billion in venture capital funding. But volumes declined 26.1% over the subsequent quarter and are roughly 20% off from the totals reported during the first half of 2024.

The startup pipeline, which is the lifeblood for leasing in these mission-critical innovation properties, has been throttled as a result. And this, in turn, could curtail even more new clinical trials, leading to slower development of new therapies.

As Marcus explained, this quarter “is a critical juncture and time for this industry. On the one hand, [we have] the greatest prospect ever for innovation in our time. On the other, the relentless… government shutdown.”

Yet he’s ultimately optimistic, declaring that the biotech bear market is “starting to turn the corner.” In which case, life-science landlords are headed into healthier times, too.

Alexandria’s Current Situation Isn’t Pretty

There are several publicly traded REITs with access to life-science properties. But my eyes are still on Alexandria Real Estate with its first-mover advantage.

The largest landlord in the biotech space, its portfolio includes 39.1 million square feet of rentable space and 4.2 million square feet under construction. That involves 700 tenants, with 90% of its top 20 being investment-grade or publicly traded large-cap companies.

As is the case for most life-science properties, ARE’s buildings are close to colleges and universities, which provide a steady pipeline of qualified employees. The REIT has a notable presence in San Diego, the San Francisco Bay area, greater Boston, New York City, Maryland, and the Research Triangle in North Carolina.

{kind=link}

Source: Alexandria Real Estate

Admittedly, those superior locations didn’t stop it from suffering these past few years – even more than expected. You might remember how we had to sell out of our position in The Wide Moat Letter in February after it hit our stop loss.

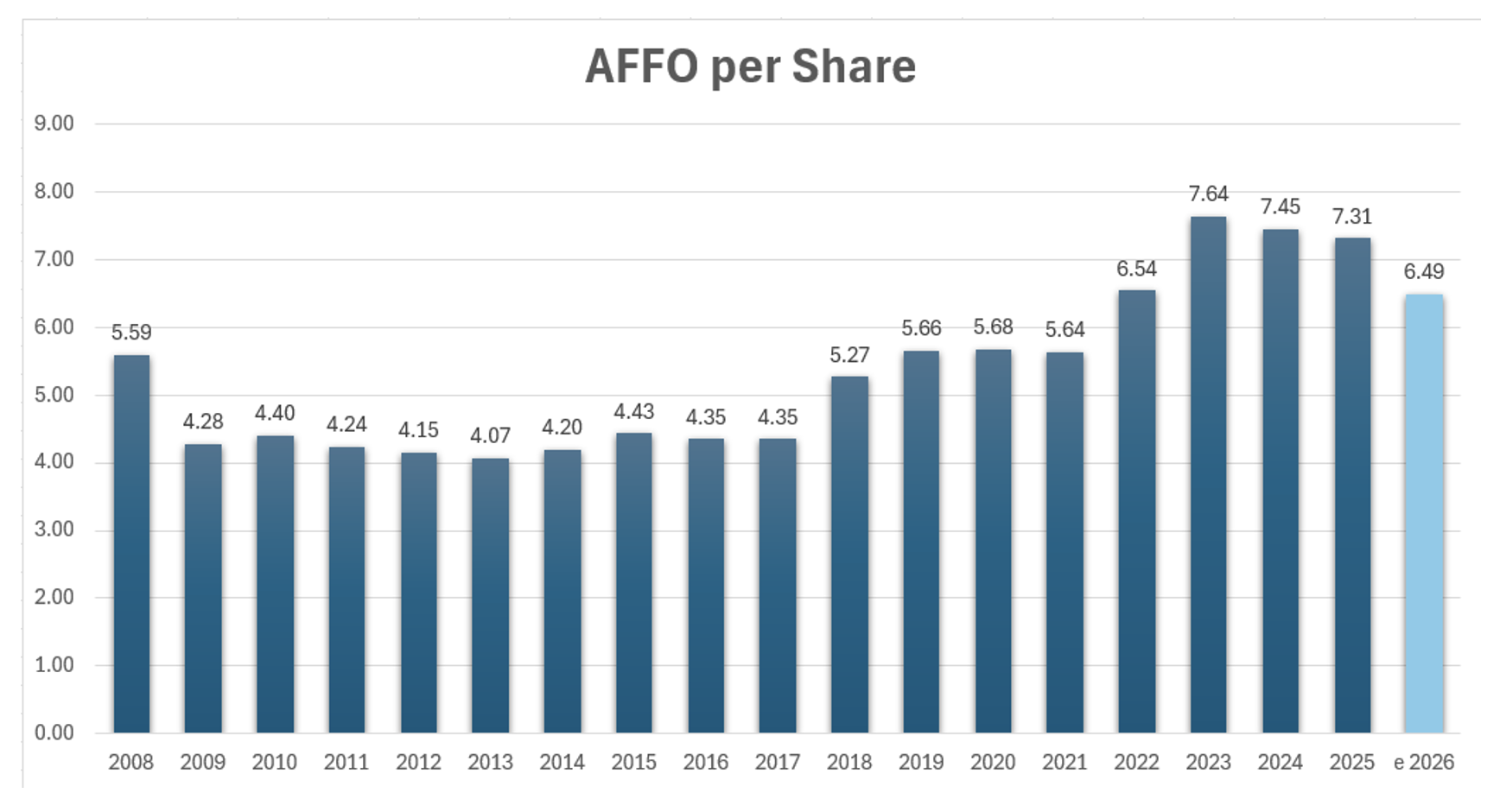

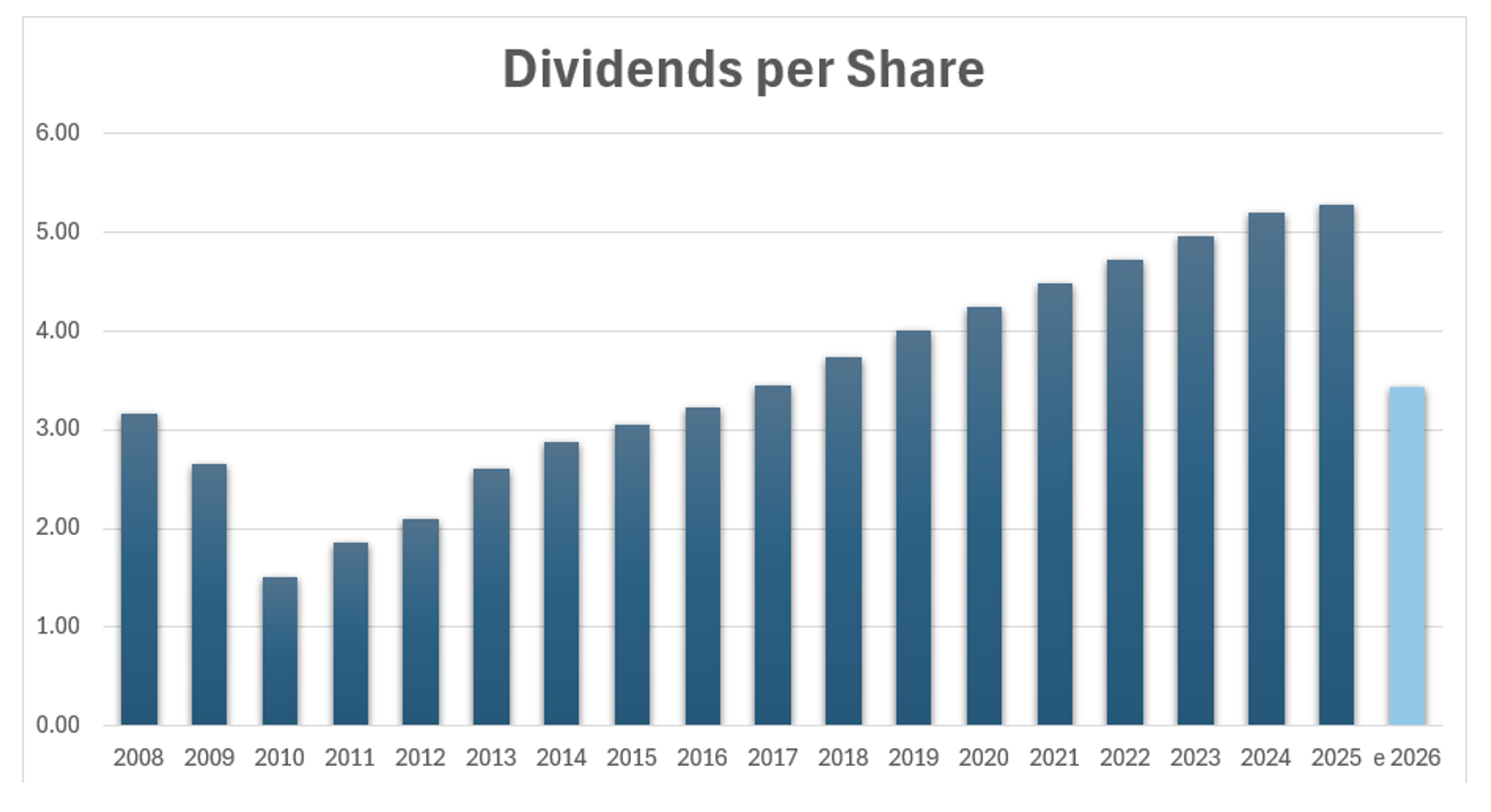

Truth be told, ARE’s third-quarter earnings weren’t any more optimistic, with funds from operations (“FFO”) per share coming in at a mere $2.22. Management also reduced its year-end FFO guidance by $0.25 to $9.01, down 5% year over year, primarily due to lower investment gains, occupancy, and same-property performance.

In addition, the company has released its 2026 guidance of $6.55 at the midpoint. That’s a 27.3% reduction over this year and far below the previous consensus of $8.24.

Here’s a snapshot of our adjusted FFO (“AFFO”) per share model to consider:

{kind=link}

Source: Wide Moat Research

That puts its dividend safety at serious risk, which Marcus fully admitted to:

… the cumulative growth in dividends and FFO has been highly correlated since 2013. Given the factors that we described in our press release that are expected to impact 2026 earnings and cash flows, we anticipate that our board of directors will carefully evaluate future dividend levels accordingly.

Translation: With earnings slowing down, ARE will evaluate its dividend in 2026 to remain aligned with per-share FFO and maintain capital for core operations. Here at Wide Moat Research, we estimate a 35% dividend cut would preserve the REIT’s $315 million in annual cash flow.

{kind=link}

Source: Wide Moat Research

It wouldn’t be pretty, but sometimes a company’s gotta do what a company’s gotta do.

As my longtime readers know, I’m a big proponent of reliable dividends. And I’d typically recommend avoiding companies that are forced to cut the dividend.

But, in the case of Alexandria, I might be willing to make an exception. The company’s predicament has nothing to do with management (which is excellent) or the underlying business model (which is very sturdy). Alexandria was the victim of a market dynamic nobody could have seen coming.

The company will work through this rough patch. And once it does, I’m sure it will once again become the wonderful compounder it was for decades.

And if that’s the case, shares might be worth a look today. That’s because they’re dirt cheap.

Alexandria’s Future Looks Bright

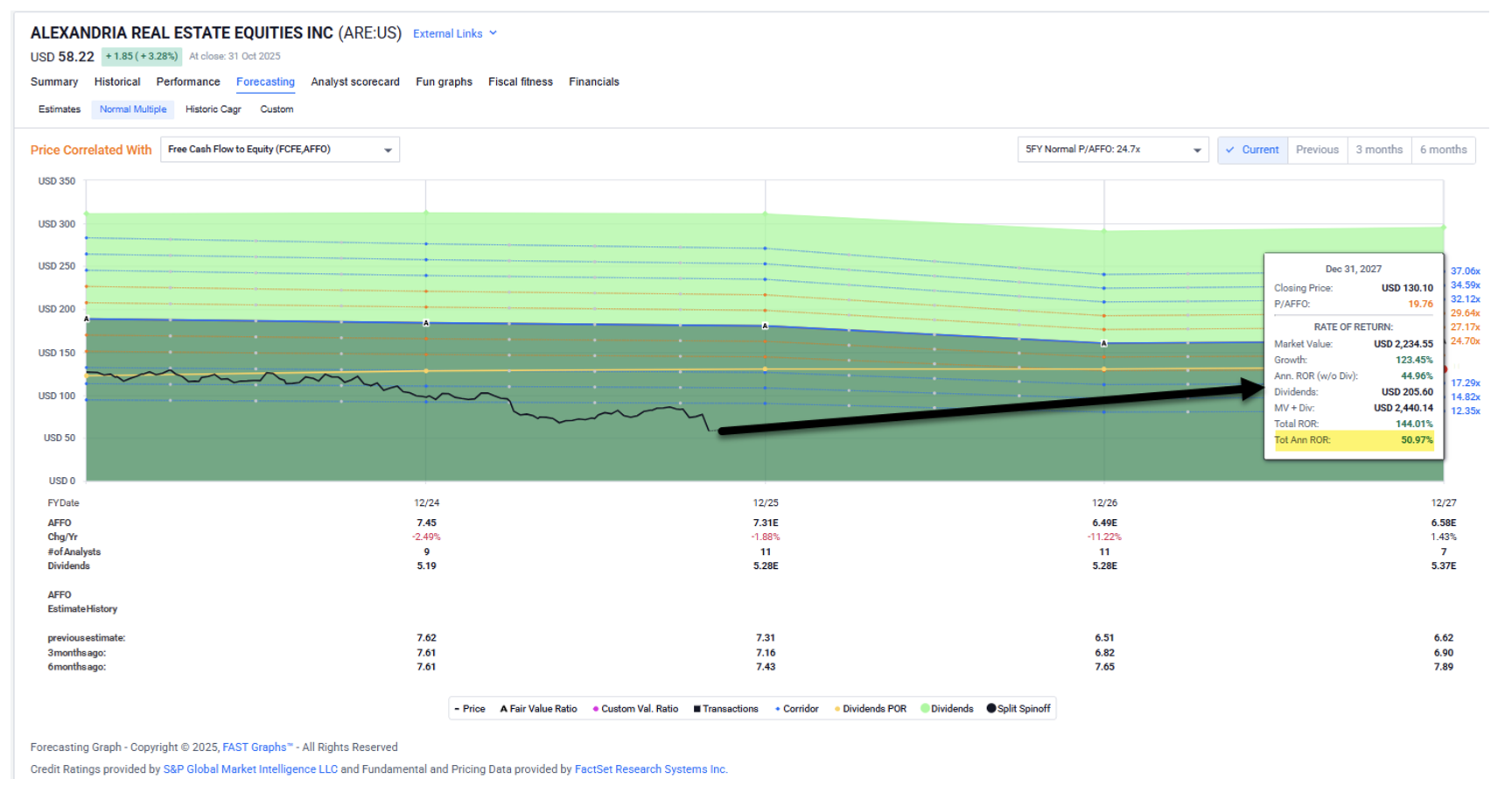

In terms of valuation, ARE’s shares have pulled back by over 25% since its latest earnings release. They now trade at 7.9 times price to AFFO compared with its normal (historical) 20.8 times. In fact, ARE hasn’t been this cheap since the Financial Crisis in ’09.

{kind=link}

Source: FAST Graphs

Maybe this is the result of a life-science real estate bubble that has popped. But in my view, it’s more of a demand issue from low leasing activity, hence the “zombie” buildings Marcus mentioned.

Yet even with all this against it, Alexandria still enjoys the highest-quality portfolio possible. So, I’m confident that demand will reset as rates decline and new technologies are introduced.

Catalysts for its recovery include capital formation within biotech and drug discovery trends. It’s only a matter of time before tenants need more space under improving conditions. And while life-science real estate continues to grapple with an acute supply and demand imbalance, the supply pipeline has officially begun to recede from post-pandemic highs.

In which case, ARE’s well-known and well-respected position as the industry leader should serve it well.

All told, I believe the market has largely priced in all of Alexandria Real Estate’s bad news. I consider it to be a great buy with huge potential – possibly 50% annual returns over the next 12 to 24 months.

{kind=link}

Source: FAST Graphs

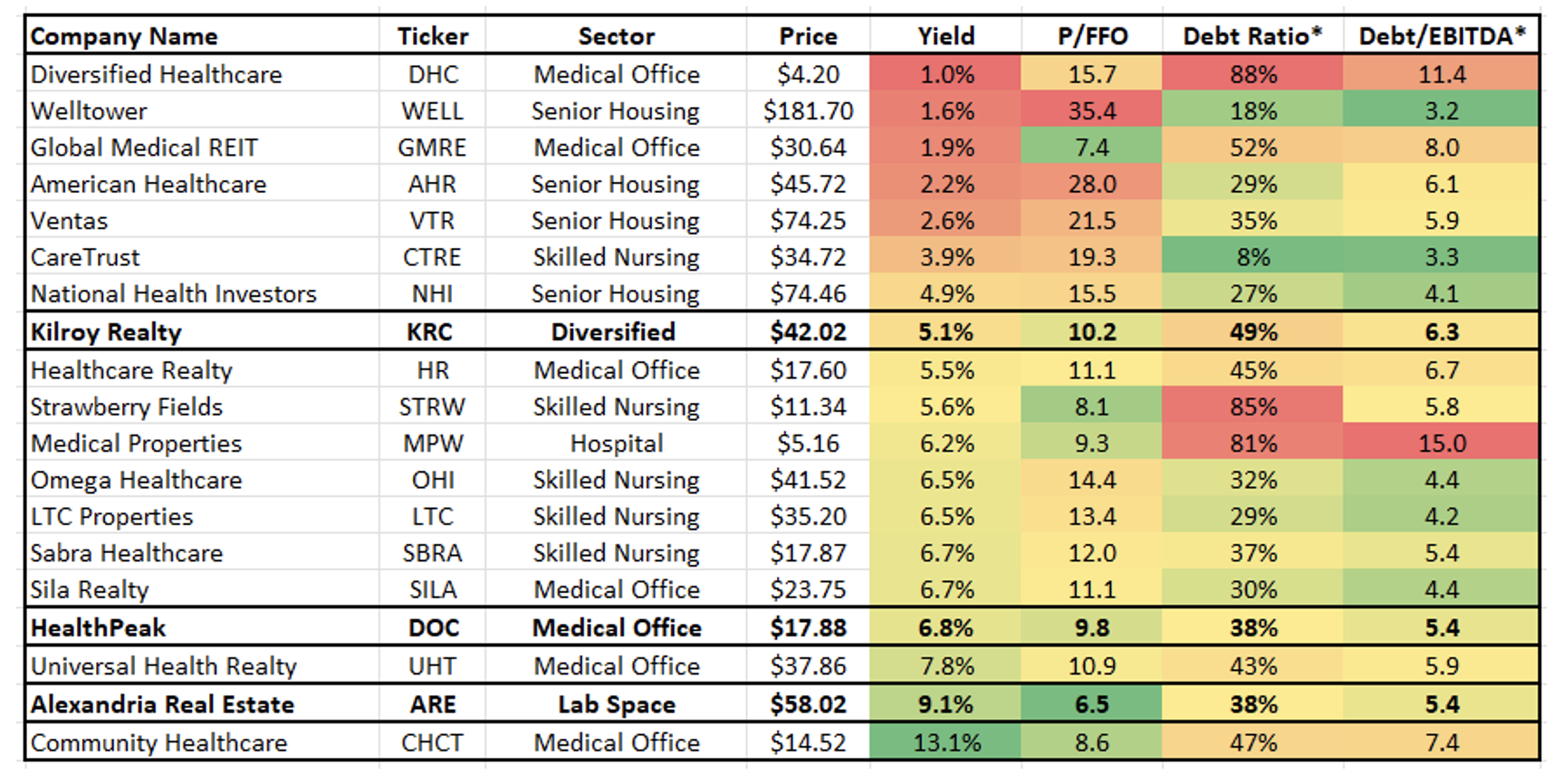

I plan to speak with Alexandria’s CEO, Joel Marcus, today. And I’ll let you all know what he says on Thursday’s Wide Moat Show – right along with my assessment of other life-science REITs like Kilroy Realty (KRC) and Healthpeak (DOC).

Make sure to subscribe here to help guarantee you’re one of the first to get the details… and be able to act on them.

{kind=link}

Source: Wide Moat Research

Regards,

Brad Thomas

Editor, Wide Moat Daily

|