Investors don’t like regional banks right now. Actually, they haven’t for years. And I understand why.

These financial institutions have been hit hard from all sides. Rising interest rates, deposit competition, and concerns over commercial real estate exposure – especially with office buildings – have created the perception that they’re bad investments.

It came to a head in 2023 during the regional banking crisis. There were several old-fashioned runs and the failure of three banks. Regional banks have languished ever since.

In many cases, that perception is correct. But in typical Wall Street fashion, the markets have gone overboard on the idea, missing out on some great opportunities in the process.

Nowhere is this truer than in the Sun Belt.

Texas, Florida, the Carolinas, Georgia, Arizona… States like these are experiencing significant population growth and job creation as more and more corporations migrate south – complete with their employees and those employees’ families.

This has been going on for over a decade now. And recent news from places like California, Massachusetts, and New York indicates that the trend isn’t fading.

Mark Zuckerberg, for instance, is only the latest Californian billionaire to relocate. Last month, he purchased a new primary residence in Florida, likely in response to the threat of even higher taxes to come.

Meanwhile, it was recently reported that Massachusetts lost over 180,000 residents between April 2020 and July 2025. And since Boston just raised its property tax rate by 13%, I don’t see too many people jumping to fill those lost spots.

As for New York City, Mayor Zohran Mamdani just announced the city’s first-ever pied-à-terre tax. This will impose an annual fee on luxury properties worth at least $5 million if their owners don’t live there full-time.

More on that tomorrow. For now, let’s just say that’s a great way to encourage even more business growth – in completely different states.

Regional banks in the Sun Belt are proof of how true that is.

Regional Bank Play No. 1: Prosperity Bank

Let’s start in the great state of Texas, where everything is big – and getting bigger – including the population.

In 2000, Texas boasted 20.9 million residents, according to Census.gov. By mid-year 2025, that number was up over 31.1 million, marking a 48.8% increase.

That’s in part thanks to the 200-plus companies that have relocated their headquarters to the Lone Star State since 2020, including SpaceX, Hewlett-Packard, Caterpillar, and Coinbase.

While South Carolina is the fastest-growing state by percentage points, Texas wins out in the sheer numbers game. So there’s a steady stream of business for its regional banks like Prosperity Bancshares (PB).

Headquartered in Houston with a $38 billion asset platform, it has more than 300 branches spread across the state and into Oklahoma. But it’s not just Prosperity’s scale that’s impressive… its consistency stands out as well.

The bank operates with a conservative, community-oriented philosophy. It focuses on disciplined acquisitions, where it makes sure it has a solid grasp on both its balance sheet and each local market it aims to reach.

In fact, Prosperity is a top pick for underwriting loans due to its knowledge of the areas it operates in. Add that corporate commitment to Texas’ population boom, and you get:

-

Steady loan demand across residential development

-

Plenty of small business lending

-

Commercial projects tied to population growth

In the fourth quarter of 2025, the bank generated strong earnings, including net income of $543 million. That’s a 13.2% increase over fourth-quarter 2024’s $480 million. And I look forward to seeing what Prosperity can do from here, considering how it’s officially acquiring Stellar Bancorp (STEL) on July 1.

That will make it one of the largest banks in Texas.

Management said it expects earnings of $7.34 per share in 2027. And shares now trade at a forward multiple of 12 times. Assuming that figure jumps to 13 times, the stock would be valued at around $98, generating 25% annualized returns.

{kind=link}

Source: FAST Graphs

Regional Bank Play No. 2: Southern First Bank

I have absolutely no problem promoting a Texas investment. But my regular readers know my heart belongs to South Carolina.

So I’m happy to include this next Carolina-focused bank as well.

In 2000, my home state featured just over 4 million residents, according to Census.gov – a number that jumped 39% to almost 5.6 million residents as of last year. Business is booming here, with both new companies emerging and already existing corporations expanding into South Carolina.

A few examples of the latter include:

-

Boeing moving all of its 787 Dreamliner final assembly operations to the state

-

Walmart investing $220 million into a new direct import distribution center

-

Google investing $9 billion to expand its cloud and artificial intelligence (“AI”) infrastructure

-

Vendr, a Boston-based Software-as-a-Service (“SaaS”) buying platform, building a significant second hub in Charleston.

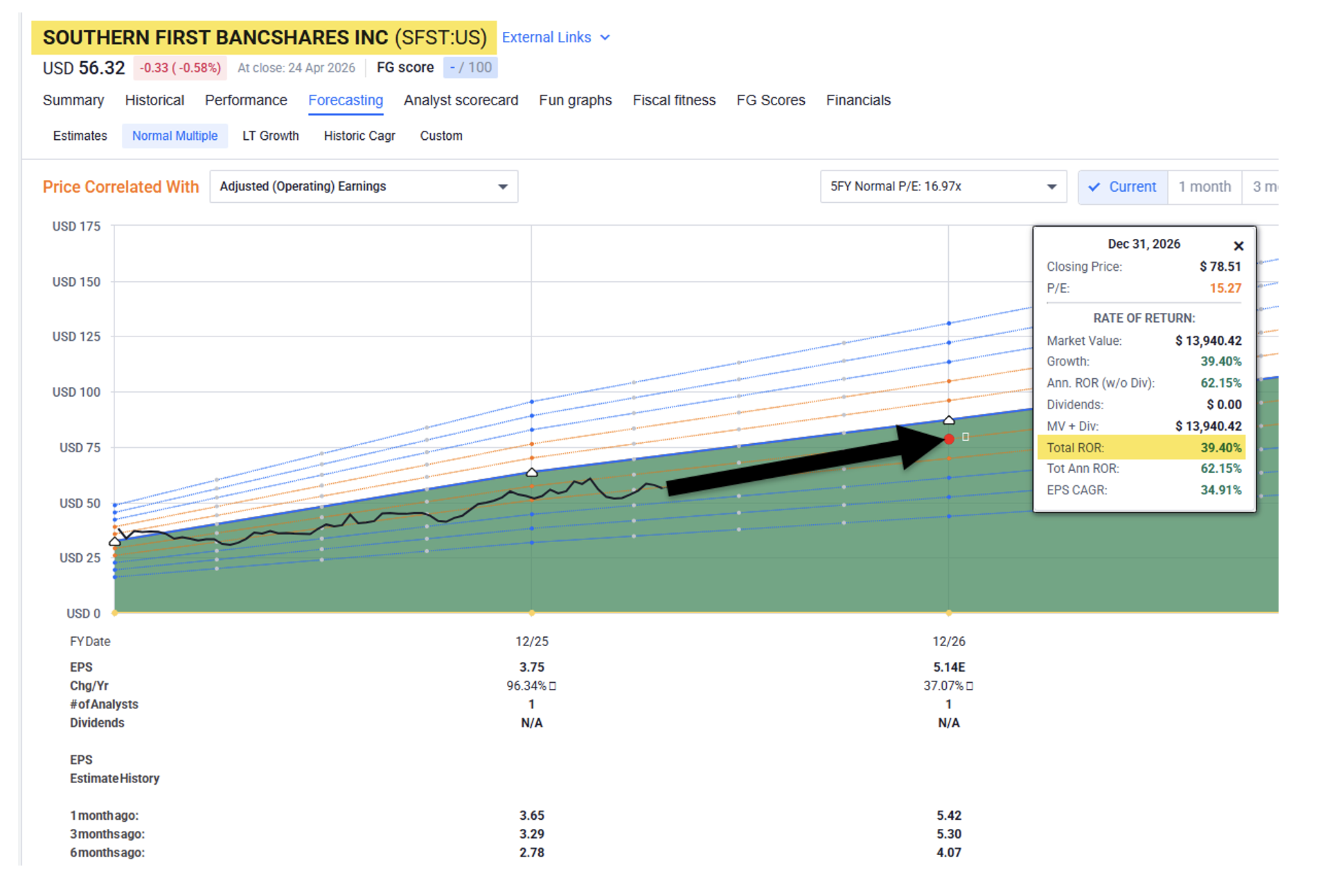

This is all good for Southern First Bancshares (SFST), which is headquartered in Greenville, South Carolina. It holds roughly $4 billion to $4.4 billion in assets throughout the Southeast, including in major growth markets like Atlanta, Georgia; Charlotte, North Carolina; and Raleigh, Virginia.

Southern First’s banking model is different than Prosperity’s but just as compelling. It has built its franchise around assigning dedicated banking teams to the business owners, developers, and other professional clients it works with.

This “relationship banking” approach tends to attract higher-quality borrowers who value consistency. And this, in turn, tends to produce stronger loan performance.

Admittedly, it’s more difficult to offer that kind of attention on a large scale, which is why Southern First doesn’t have the level of diversification some of its peers do. However, it does an excellent job of working with the assets it does have, generating outsized returns as a result.

Last week, the company announced first-quarter 2026 results, including earnings per share (“EPS”) of $1.19 and revenue of $33.8 million. Net income of $9.9 million was 88% higher than the same quarter last year. And retail deposits came in at $3.4 billion, up $207.8 million, or 27% (annualized), from the fourth quarter of 2025.

Shares have returned around 14% since I recommended the bank last November. Yet I still find them attractive, as they’re trading at 13.5 times when their normal multiple is 15.5 times.

Analysts are forecasting 37% growth this year, which would translate into 30% returns from today’s price point.

{kind=link}

Source: FAST Graphs

Regional Bank Play No. 3: Huntington Bank

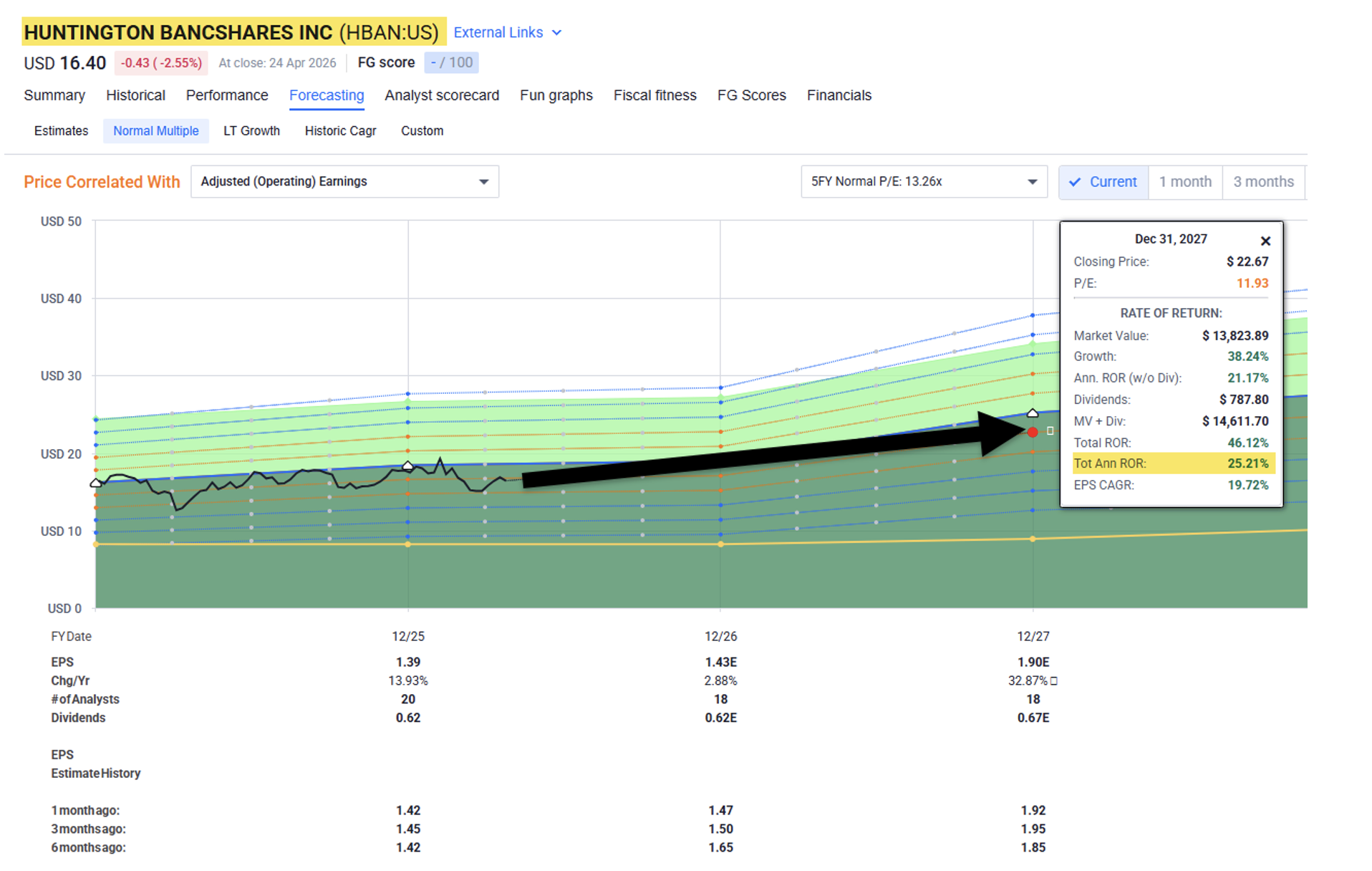

Finally, we have Huntington Bancshares (HBAN), which represents a different but still viable angle into regional financial plays.

A comparatively larger bank with over $200 billion in assets, it’s traditionally focused on the Midwest. But Huntington knows a good thing when it sees one.

So it’s aggressively expanding into the Sun Belt, including in Texas and South Carolina.

Its merger with Cadence Bank on February 1 has definitely helped it fast-track those efforts, giving it immediate scale in some of the most attractive banking markets in the country. Huntington can now put its strong balance sheet and capital market access to work where economic growth is truly surging.

The bank already delivered strong results in the first quarter, with EPS of $0.25. And excluding acquisition-related expenses and other notable items, it was $0.37, up 9% year over year.

Net interest income, meanwhile, increased $301 million, or 18.7% sequentially. That was up 33% year over year.

Here’s another reason to like Huntington: It’s been active in sublet expansion, acquiring two banks (Veritex and Cadence Bank) this past quarter. Both were wise purchases that should result in outsized growth in the years ahead.

Shares of HBAN are trading at 11.7 times, far lower than their normal 16 times. And analysts expect 33% growth in 2027.

As shown below, we believe shares could return 25% annually.

{kind=link}

Source: FAST Graphs

Regards,

Brad Thomas

Editor, Wide Moat Daily

|