Editor’s Note: For interested readers, the team over at TradeSmith, a corporate affiliate, have just revealed what could be the biggest breakthrough in their company’s history. It’s an AI-powered tool that, through the company’s back test, had 85% accuracy at forecasting the direction of 2,335 stocks. It sounds almost unbelievable, but the team is demonstrating the new tool and giving all the details right here.

Every October for the past decade or so, I’ve written an article titled “Trick or Treat, My Favorite REITs,” where I profile several of my favorite REIT setups. I also write a corresponding piece on those that are dressing up as something they’re not.

Today, we’re going to start out with the treats. And fortunately, the real estate investment trust (“REIT”) space is full of great companies to choose from.

That makes sense considering how far the sector has come since its inception in 1960. REITs have evolved into a compelling asset class worth more than $1.47 trillion today.

This includes a growing range of property types, including hi-tech cold storage landlords like Americold (COLD) and Lineage (LINE). Both mission-critical parts of the global food supply chain have fallen out of investors’ favor due to tariff uncertainty and inventory carrying costs.

But that just means they’re trading at bargain prices. As I explained last week, they could provide very nice returns going forward.

And they’re not the only tempting treats out there.

REITs You Can Really Bite Into

There are also technology-based billboard landlords like Lamar Advertising (LAMR) and Outfront Media (OUT). Billionaire Warren Buffett’s Berkshire Hathaway (BRK-A)(BRK-B) scooped up 1.1 million shares of the former in the second quarter for $142 million.

(Incidentally, I wrote a letter to Warren Buffett a few weeks ago with even more REIT suggestions.)

Then there are mission-critical data-center REITs like Digital Realty Trust (DLR) and Equinix (EQIX) – artificial intelligence’s backbone. I recently explained that “the more technologically connected we become, the more we rely on these [data center] sites.”

I also have to point out how, last week, leading warehouse landlord (and data-center owner) Prologis (PLD) announced its third-quarter 2025 earnings. Shares surged almost 12% on rock-solid results fueled by record-setting leasing activity. The company boosted earnings growth this year from 5.3% to 5.7%, as measured by funds from operations.

Competitor Rexford Industrial Realty (REXR) rallied 11% after reporting its own record-setting leasing volume. As a result, it raised its 2025 earnings growth estimates from 2.1% to 2.6%.

And yet another warehouse REIT, First Industrial Realty Trust (FR), raised its 2025 funds from operations (“FFO”) per share estimate from 10.2% to a sector-leading 11.7%. That news set its shares surging 10%.

Moving on to the net-lease category, we have the pure-play USPS landlord Postal Realty (PSTL). As I mentioned last week, it’s not impacted by the government shutdown, promising to deliver dividends no matter the rain, sleet, or snow.

I’ve also covered farming REITs, casino REITs, hotel REITs, and apartment REITs recently here at Wide Moat Daily… to say nothing of the picks mentioned in my weekly YouTube channel, The Wide Moat Show.

But as tasty as they all are, there are two that stand out the most to me right now.

REIT Treat No. 1: EastGroup

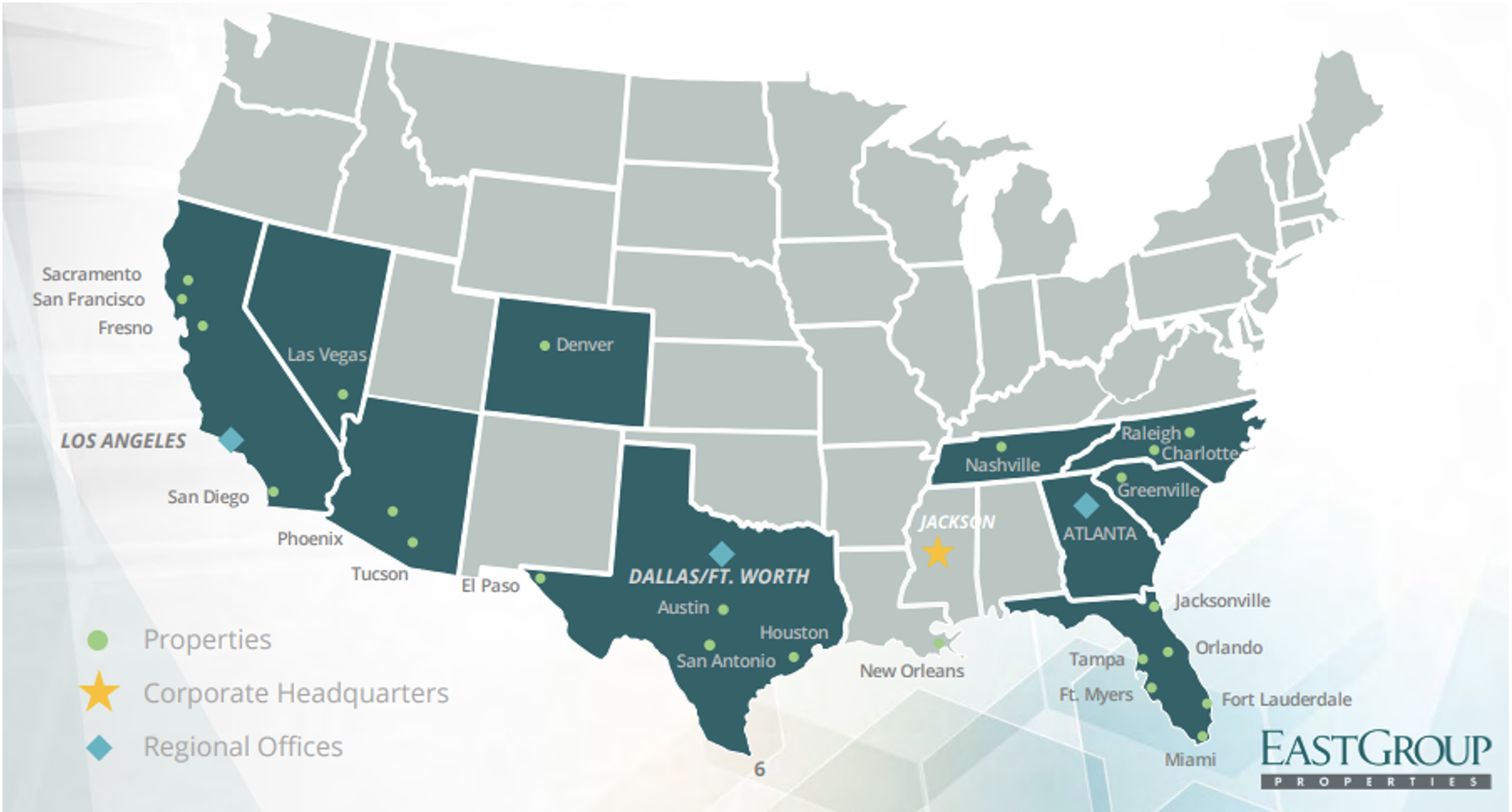

Based on the aforementioned results from Prologis, Rexford, and First Industrial… I expect similar outperformance from fellow industrial REIT EastGroup Properties (EGP), which focuses on high-growth states like Florida, Texas, Arizona, California, and North Carolina.

The landlord operates within a unique niche by providing functional, flexible, and quality business distribution space for location-sensitive customers – primarily those in need of space within the 20,000 to 100,000 square foot range.

EGP’s strategy for growth is based on ownership of premier distribution facilities generally clustered near major transportation assets in supply-constrained submarkets.

{kind=link}

Source: EastGroup Investor Relations Report

It has one of the safest REIT balance sheets across the board, with debt to total market capitalization of just 14.2%. Its unadjusted debt-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio is 3 times. And its interest and fixed charge coverage ratio is 16 times.

Although EastGroup hasn’t announced its third-quarter earnings yet, it estimates FFO of $2.22 to $2.30 per share, with an average month-end occupancy range of 95.3% to 96.1%. Also, back in August, the REIT announced a 10.7% dividend increase from $1.40 to $1.55 per share.

That’s pretty sweet.

As seen below, shares are now trading at a 25.5 times price to adjusted FFO (p/AFFO) multiple compared with its normal multiple of 30 times. Notably, analysts expect growth of 7% this year, 8% in 2026, and 9% in 2029.

This means there’s a very good chance that EastGroup continues to boost its dividend by at least 8% per year over the next few years.

My conservative model has shares topping $213 by the end of 2016… which translates into an annualized total return of 20%. But if shares revert to their normal valuation of 30 times, investors could see that figure hit 30%.

Plus, EGP’s dividend yield is 3.5%. So you get a nice bonus while you wait on Mr. Market to come to its senses.

{kind=link}

Source: FAST Graphs

REIT Treat No. 2: Equinix

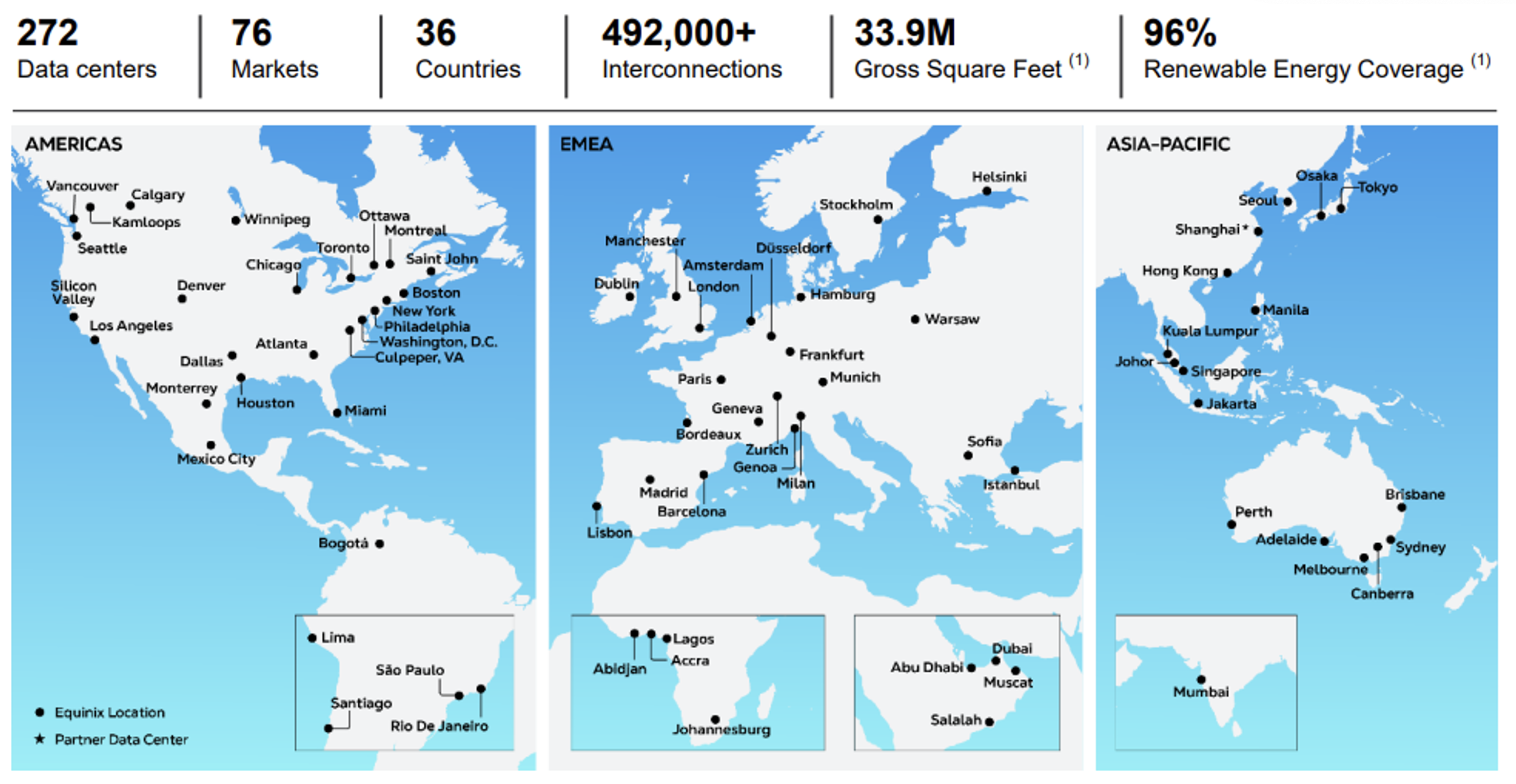

The already mentioned Equinix is one of the largest publicly traded REITS in the world – and a great way to play the AI trend on the infrastructure side. It operates 272 data centers and serves over 10,000 customers across more than 492,000 interconnections located in 36 countries throughout six continents.

The mission-critical nature of its infrastructure allows Equinix to embed annual price increases of 2% to 5%. These contracts are also quite lengthy, with an average lease maturity of more than 18 years, including extensions.

{kind=link}

Source: Equinix Investor Relations Report

As of the second quarter, Equinix’s net leverage was 3.5 times annualized adjusted EBITDA. And the company “fully expects net leverage to increase over the next several years to fund growth both from the cash generated in business and with the incremental debt” it plans to raise.

Through 2029, Equinix said it “continues to remain comfortable raising debt levels up to 4.5 times in support of this growth and to fund other strategic initiatives while maintaining its investment-grade rating (BBB+).”

At the end of the second quarter of 2025, it raised 2025 AFFO guidance by $28 million. That’s expected to grow 10% to 12% over 2024, while AFFO per share growth should be 7% to 10%.

As seen below, shares are now trading at 21.7 p/AFFO compared with its normal 24.8 times multiple. Notably, predict 9% growth this year, 6% in 2026, and 7% in 2029.

My conservative model has shares topping $970 by the end of 2016, which translates into an annualized 20% total return. If shares revert to their normal valuation, investors could see 25% annualized returns or more.

Equinix’s dividend yield is 2.3%.

{kind=link}

Source: FAST Graphs

If you think REIT dividends are juicy, you’ll love business development companies, which yield an average of 12%!

Just remember while you’re investigating these entities that there might be a few “too good to be true” dividend yields among them. That’s why you should be sure to check out my Wide Moat Daily article tomorrow, where I’ll be examining the sector and sharing my thoughts…

Happy SWAN (sleep well at night) investing!

Regards,

Brad Thomas

Editor, Wide Moat Daily

|