The housing crash of 2008 was brutal. I would know… I lost almost everything in that crisis.

Home prices plunged, foreclosures soared, and entire businesses shut down – mine included. Those were hard times. But some institutional investors saw opportunity.

In 2010, a record of approximately 3 million homes were foreclosed on. And given the dire straits of the economy, not many individual buyers were stepping up to claim them.

So, institutional investors stepped into the mess by buying distressed single-family homes (“SFHs”) at very attractive prices and renting them. Very often, they’d rent them back to the former owner who was still living there.

This continued for years. By 2012, select corporations began buying SFHs in bulk through systematic acquisition platforms.

Take Blackstone (BX), one of the largest institutional asset managers in the world. It bought thousands of homes through its affiliate, Invitation Homes. That venture went so well – amassing nearly 50,000 homes by 2017 – it went on to list as a real estate investment trust (“REIT”) on the New York Stock Exchange in 2017 under the ticker symbol INVH.

This IPO raised around $1.5 billion, one of the largest market debuts for a REIT at the time.

Billionaire Wayne Hughes – who had already founded Public Storage (PSA), which I wrote about on Thursday – started another REIT, American Homes 4 Rent (AMH), in 2012. It was the same playbook. By the following August, it had about 10,000 homes.

Today, that number is over 61,000.

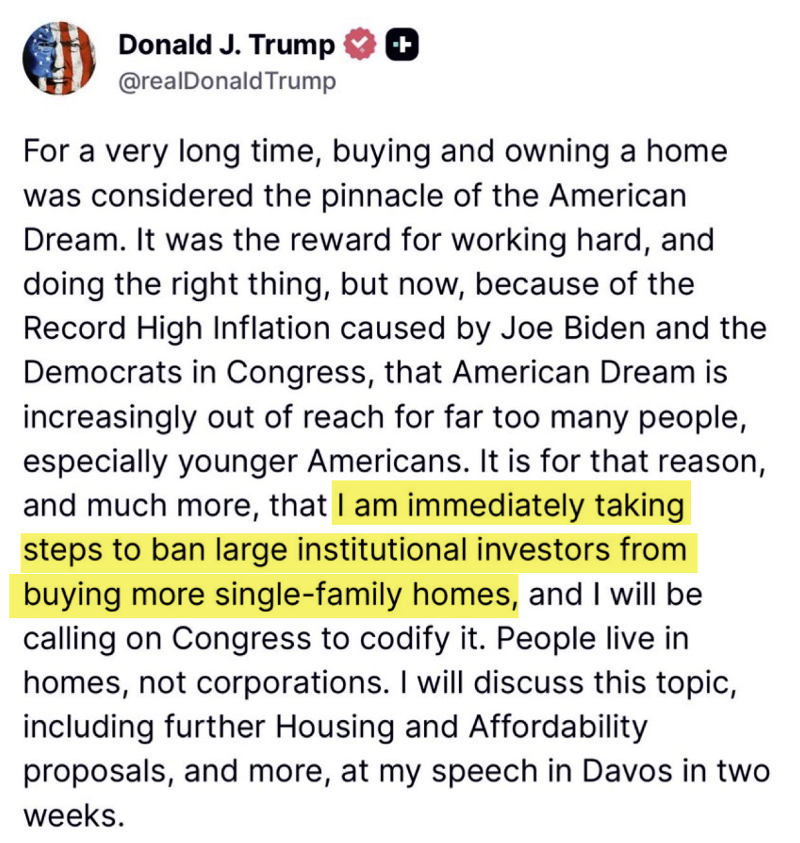

Both single-family rental (“SFR”) REITs have done very well under current housing market conditions, where buying homes remains too expensive for most. But then President Trump posted this on Trust Social last week (emphasis added):

{kind=link}

Source: Truth Social

Just like that, the markets lost confidence in SFR REITs, sending them down about 6% in a single day. Even Blackstone had a knee-jerk sell-off before rebounding.

I understand the instinct behind something like this. As I’ve written in the past, housing affordability is anything but right now. And there’s an urge to “do something” on behalf of would-be homebuyers.

But this won’t do it. And to understand why, you have to look under the hood of the American housing market.

The Truth About Single-Family Rental REITs

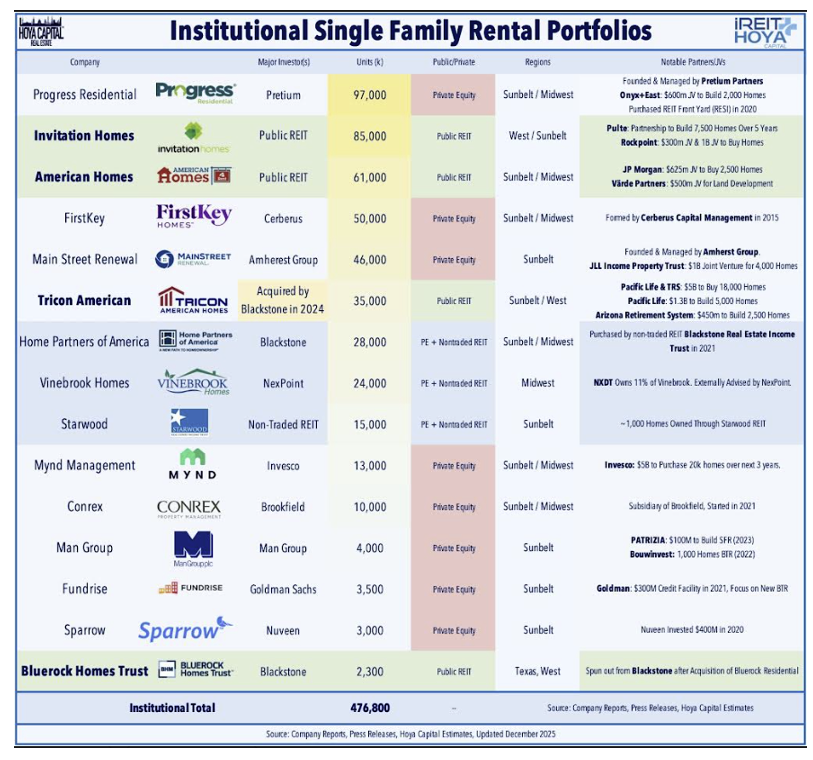

Two other publicly traded REITs invest in SFHs apart from Invitation Homes and American Homes 4 Rent. NexPoint Diversified Real Estate Trust (NXDT), which listed in 2006, owns around 3,000 homes; and Bluerock Homes (BHM), which listed in 2022, owns roughly 2,000.

Collectively, these four own around 173,000 homes, which is a very small percentage of the U.S. housing stock. And that impact remains small even after you include private owners such as:

-

Pretium, owner of Progress Residential, with its 97,000-plus homes

-

Cerberus, owner of FirstKey Homes, with around 50,000

-

NexPoint, with around 24,000 through VineBrook Homes

-

Brookfield, with around 10,000 through Conrex

Altogether, institutional investors with more than 2,000 homes in their portfolios account for less than 0.5% of the U.S. single-family housing stock.

{kind=link}

Source: HOYA Capital

I know we heard a lot about these companies and how they were buying up properties left and right during the pandemic years. In doing so, the allegation goes, they jacked up prices astronomically.

But the truth is individual owners and sellers were just as responsible in setting and paying exorbitant prices. The number of homes available was limited, demand had skyrocketed, and the entire market reacted predictably.

Really, undersupply is the core issue behind today’s housing unaffordability. This was driven by a decade of underbuilding after the 2008 crash and compounded by a host of headwinds that have driven up the cost of land and construction more recently.

I also want to be clear that, since the Great Recession, institutional investors – including SFR REITs – have provided liquidity to the housing market. Plus, they’ve become capital takeout buyers for many homebuilders by creating partnerships in build-to-rent communities.

Most of you are aware that I know the president personally. But on this point, he’s wrong. Banning institutional investors from the housing market won’t make houses more affordable. That assumes, of course, that he can even get it done.

A Better Idea

As The Wall Street Journal noted after that Truth Social post broke, “It isn’t clear if Trump can carry out the ban without congressional approval.” And considering the president is “calling on Congress” to codify the ban, I think he knows that, too.

If he does try to act on his own, the companies fight back. A company like Blackstone has all the capital, resources, and motivation to engage in a legal battle over this… for years, if need be.

And even if Congress ends up backing him, it would take months or even years for them to pass anything on the subject – only for SFH institutional investors to fight back anyway through the courts.

As such, I think Mr. Market’s reaction Wednesday against SFR REITs was too reactionary. Especially when there are far better solutions to the housing market problem.

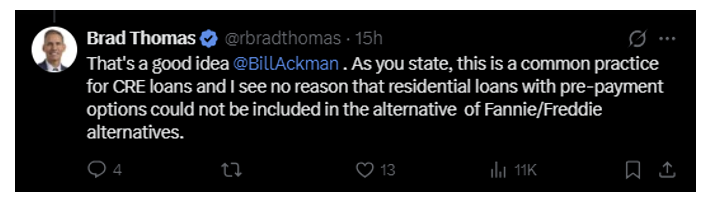

One of them came from billionaire hedge fund investor Bill Ackman over the weekend. He took to X to present a “simple idea on how to lower mortgage rates and spreads” to Trump and Treasury Secretary Scott Bessent.

It involves Fannie Mae and Freddie Mac offering mortgages with prepayment penalties.

The penalty-less prepayable feature “is attractive for homeowners,” Ackman acknowledges. But “it comes at a significant cost” to everyone involved. “Buyers of mortgage-backed securities (‘MBS’) require a significant increase in spread” as compensation, which means that most home loan holders pay a higher price.

When Ackman asked “an expert and large investor in MBS what the estimated savings today would be on a 30-year Fannie/Freddie mortgage if the borrower” had to pay a fee for prepaying, the expert “estimated that the savings would be about 65 basis points.” In which case, home loan applicants could be offered a choice:

Obtain a 30-year prepayable mortgage at today’s [roughly] 6% rate or at a 5.35% rate, but with the obligation to pay a prepayment penalty if he/she refinanced in the future…

While the ability to prepay is a valuable option, locking in the 65 [basis point, or bps] savings upfront over the life of the mortgage may be the difference between the borrower being able to afford the home and not being able to.

With all due respect to President Trump, it sounds like a much better plan, which is why I responded with:

{kind=link}

Source: @bradthomas on X

Single-Family REITs Still Have Room to Run

Donald Trump is a real estate man by trade. And he has shown he’s willing to pivot to better policy if an idea turns out to be untenable. That’s why I predict he’ll eventually abandon this idea of an institutional investor ban and look for a better path forward.

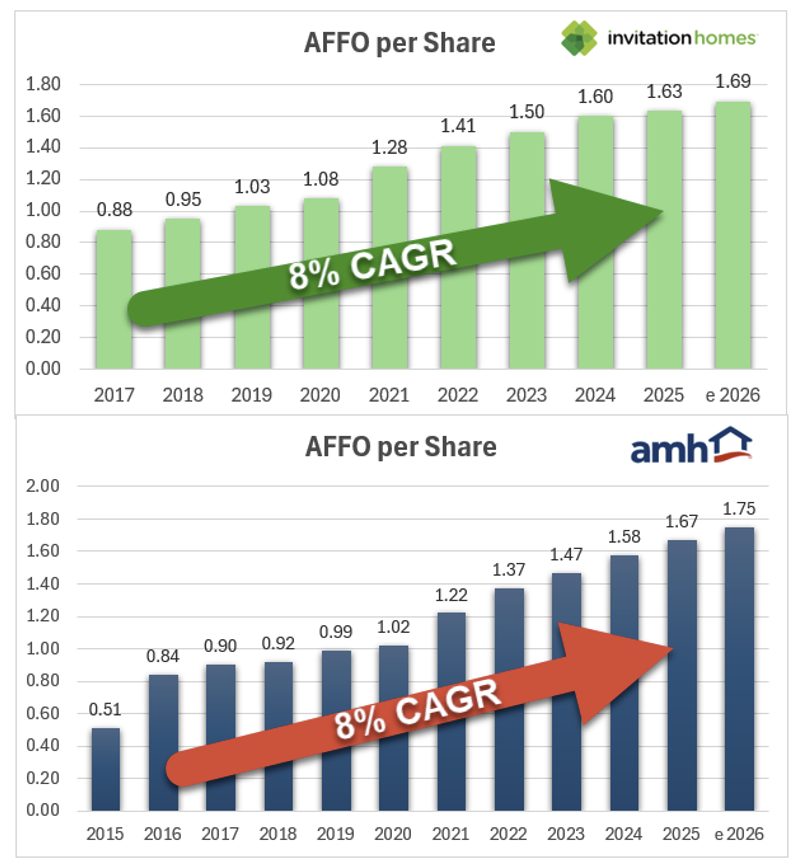

But in the meantime, both Invitation Homes and American Homes 4 Rent are still well off their pre-announcement highs. But under the hood, these are still sound businesses.

{kind=link}

Source: Wide Moat Research

As you can see above, both single-family rental REITs have consistently increased earnings in the form of adjusted funds from operations (“AFFO”) per share by an 8% compound annual growth rate (“CAGR”).

I’ll be diving further into both on the Wide Moat Show on YouTube this Thursday, along with a few other housing ideas.

Incidentally, I’ll also be participating in NYSE’s opening-bell ceremonies that same day for the newly listed Truth Social American Red State Fund (TSRS). It seeks to provide investment results that correspond to the price and yield performance of the MarketVector – iREIT® Red State Index, which I helped create. Both Invitation Homes and American Homes 4 Rent are included in the index.

For the time being, keep an eye on the SFH REIT sector. The president delivered a body blow with his announcements, but these businesses are too strong to stay down for long.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|