Real estate investment trusts (“REITs”) are on the rise!

I know I’ve been touting them these past three years, even as their share prices dropped and then stagnated. I know some of you are sick of hearing me talk about how it’s almost their time to shine again.

But the numbers are in, and it’s officially true.

They’re finding mainstream investment favor once again.

We’re now learning that commercial real estate (“CRE”) lending rose significantly last quarter as interest rates fell. CBRE’s Lending Momentum Index rose 112% year over year to 1.04 in the third quarter. That’s the highest level it has hit, not just since the pandemic – but since 2018!

CRE Daily notes that:

The surge was fueled by a 36% increase in permanent loan financing and strong September activity, signaling a broad debt market rebound. Easing financing terms, tighter bid-ask spreads, and the selective return of core capital are helping close the gap between buyers and sellers.

It’s a major quarterly change as well. Just back in July, traditional banks still frowned on CRE financing. To quote commercial mortgage banker Slatt Capital, lenders were “demanding more robust underwriting, including third-party market studies, pre-leasing commitments, and detailed exit strategies” before they would sign any contracts.

Anyone who couldn’t go that extra distance need not apply.

But capital is officially flowing back into construction projects, brightening the 2026 outlook. “Debt markets are open” again, CRE Daily writes, “and risk appetite is returning.”

Don’t mistake me: Many REITs have been worth holding well before this breakthrough thanks to their consistently growing dividend payments.

But, at long last, it looks like share price appreciation is now back on the table.

It’s a REIT Earnings Wrap

With the rate policy finally headed lower, most companies will now be able to lower their cost of capital and generate wider investment spreads. In turn, earnings and dividends alike should continue to accelerate.

We now know that REITs generated overall solid results in the third quarter, leading to a 2.5% share-price gain since October 13, when the earnings season began. The S&P 500, meanwhile, is up only 1.1%.

Some sectors are still struggling, especially:

-

Self-storage, down 7.1% (see my masterclass article)

-

Offices – including Alexandria Real Estate (ARE), which we also wrote about recently – down 5.1%

-

Cell towers, down 2.8%

But that’s more than made up for by:

-

Health care, up 11.3%

-

Industrial, up 9.1%

-

Lodging, up 7.2%

It’s no surprise to see industrials shine. They got an added kick from a leasing rebound and tariffs pause. We’ve been bullish on picks like Prologis (PLD) and Rexford Industrial Realty (REXR) for a while – both of which posted solid earnings with ample runway for dividend growth.

And while the larger residential sector saw modestly disappointing third-quarter results as rent growth decelerated… I remain bullish about manufactured housing, where rents are actually on the rise. My top pick there is Sun Communities (SUI) since it recently raised its full-year 2025 guidance by $0.04 per share to between $6.59 and $6.67.

Moving on to data centers, they remain compelling as AI demand continues to fuel robust pricing power. Digital Realty’s (DLR) third-quarter funds from operations (“FFO”) hit a record $1.89 per share, up 13% year over year. And Equinix (EQIX) now expects 5% – or higher – FFO growth next year.

(See my latest article on Digital Realty here, as well as an update on the newest data-center REIT, Fermi (FRMI). The latter’s IPO valued it at $13 billion… with just a blueprint to its name!

Retail REITs – such as the shopping centers I recently wrote about – also posted solid results, with average same-store net operating income growing 3.9% year over year. FFO, meanwhile, rose a robust 7.3%.

Finally, net-lease REITs continue to gain steam with accelerated acquisition volumes that set up a strong 2026 earnings season. I favor consolidators with scale advantage, including:

-

Realty Income (O), which I recommended to my mom a few days ago

-

Agree Realty (ADC)

-

VICI Properties (VICI), which I included in my gaming REIT analysis here

-

Essential Properties Realty Trust (EPRT)

But I wanted to go a step further today in identifying “forever” REITs that have been, still are, and should continue to pay off going forward. To do so, I employed my iREIT® screener. It uses our automated, fundamental data-driven algorithms to identify the highest-quality picks trading at a wide margin of safety.

Here’s what it found…

The Crème de la Crème

Equinix (EQIX) is a data-center REIT that owns 273 data centers in 36 countries and 77 markets. Its 34.2-million-square-foot portfolio has over 499,000 interconnections. And over 84% of its recurring revenue is generated by either owned properties or properties where lease expirations extend to 2040 and beyond.

One of the reasons this REIT scores high on the quality model is because of its balance sheet. S&P recently upgraded Equinix’s credit rating to BBB+ and increased its leverage tolerance by 0.5 times, providing greater financial flexibility.

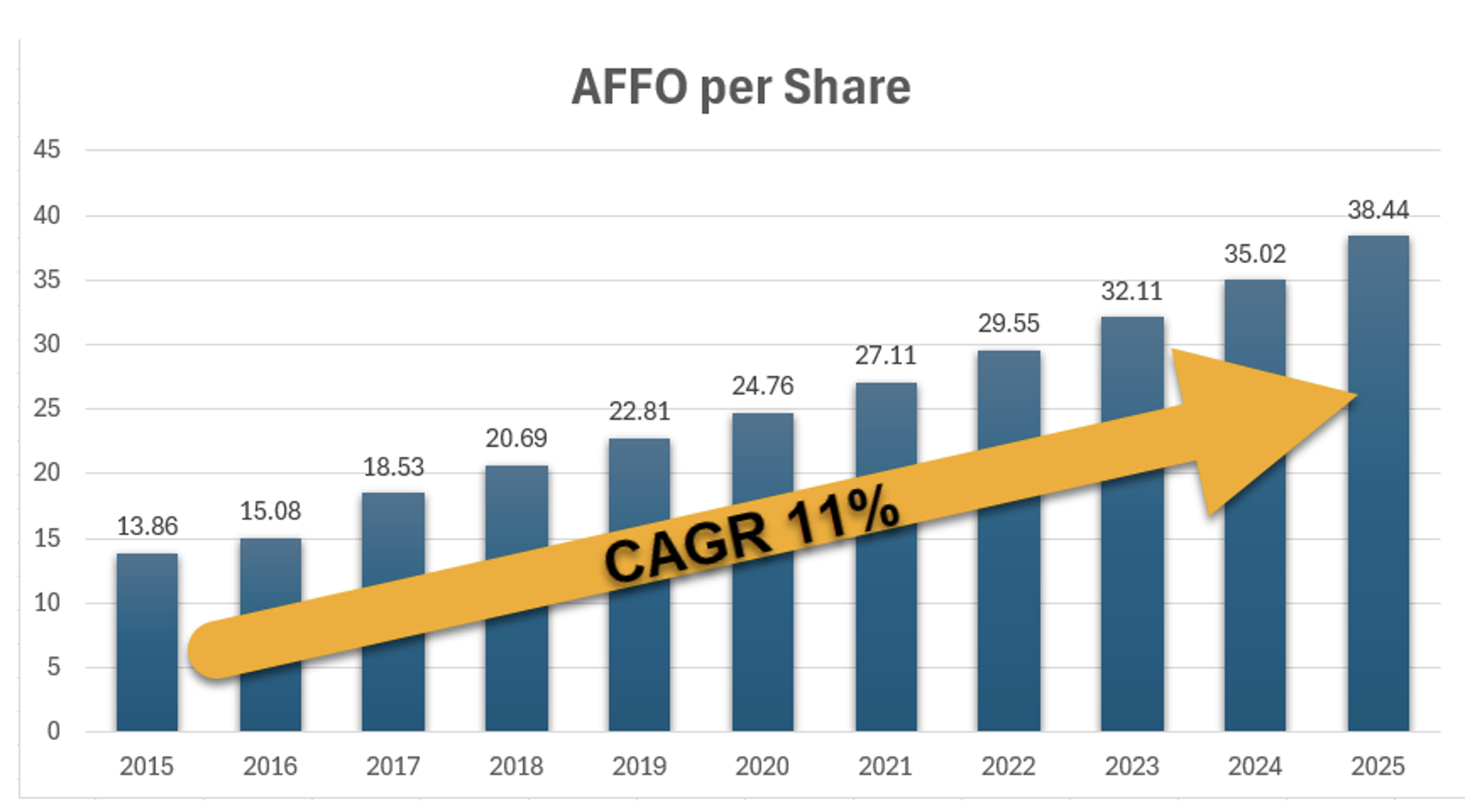

In addition, EQIX has maintained a solid record of earnings – measured by adjusted FFO (“AFFO”) per-share growth – of more than 11% compound annual growth rate (“CAGR”) over the past decade.

{kind=link}

Source: Wide Moat Research

Shares are still trading at 21.6 times, below their normal multiple of 24.8 times – thereby offering a margin of safety. And the dividend yield is 2.3% with an extremely low payout ratio of just 48%.

Analysts expect growth of around 6% in both 2026 and 2027… which makes this data-center REIT quite attractive with a total 12-month return estimate of 25%.

Our other top pick is industrial REIT EastGroup Properties (EGP). It owns around 64.4 million square feet of multitenant “flex” space located in Texas, Florida, California, Arizona, and North Carolina.

EGP focuses on holding premier distribution facilities that are generally clustered near major transportation hubs in supply-constrained submarkets. This helps it stand out from its peers, better aiding its growth goals.

Its customer base is diversified, with its top 10 tenants representing only 6.9% of overall annualized base rent. In addition, 75% of revenue is generated from tenants that lease under 100,000 square feet.

Another quality factor is EGP’s balance sheet, with just 14% debt compared with 86% in equity. This makes it the lowest leveraged REIT in the industrial sector.

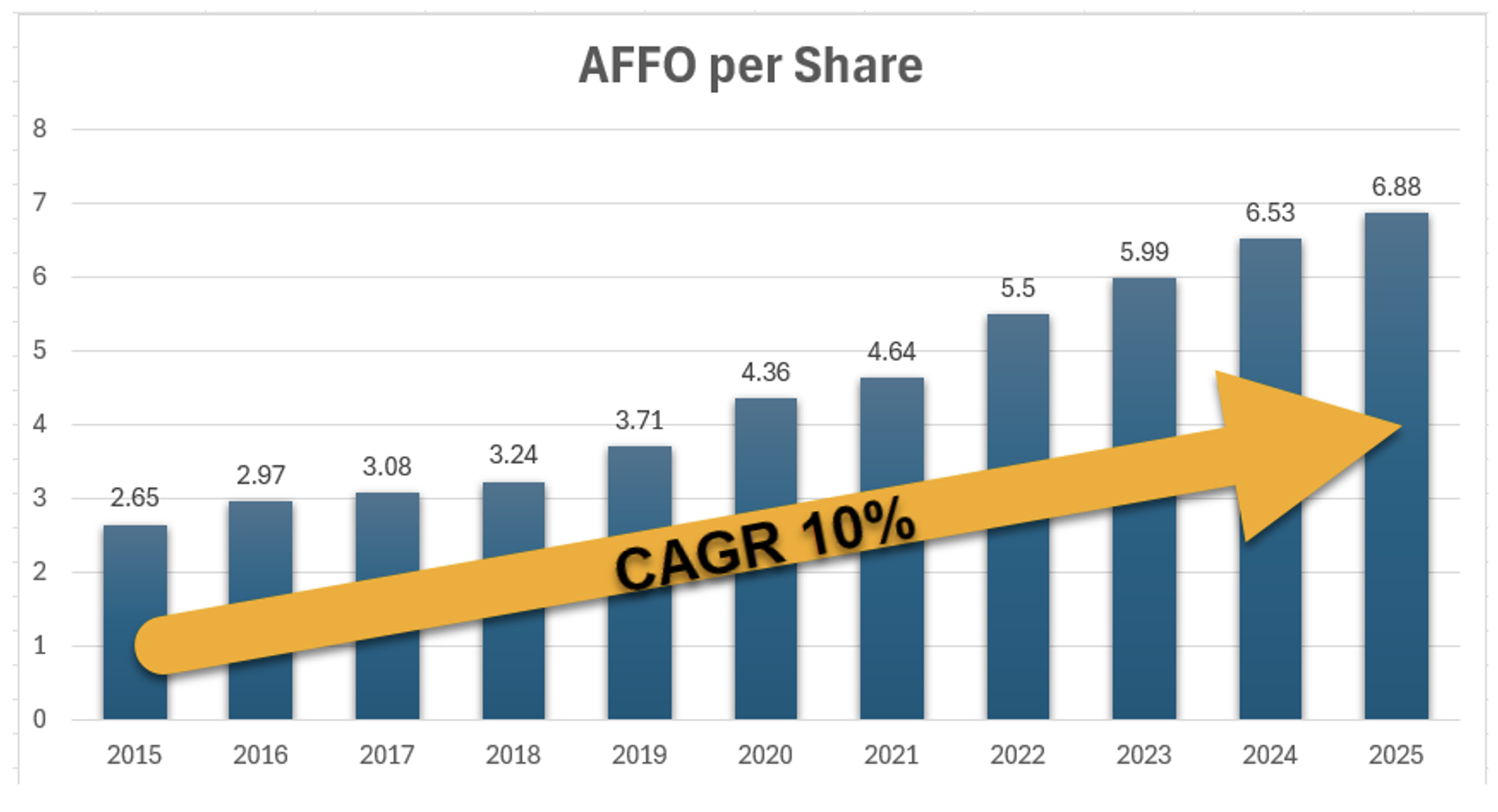

EPG’s growth metrics are equally attractive, with 10% CAGR AFFO per share gains over the past decade.

{kind=link}

Source: Wide Moat Research

Shares are trading at 25.9 times compared with their normal multiple of 28.4 times.

The REIT’s dividend yield is 3.5%. And it recently increased that payout by 11%.

Analysts expect 9% growth in both 2026 and 2027. So shares could return a whopping 20% over the next 12 months.

I think we’ll see much more optimistic and even enthusiastic REIT coverage overall from here. But I think you can see why EGP and EQIX stand out especially.

They’re very well situated to take advantage of the REIT revival that’s finally starting to show.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|