Editor’s Note: Within the next two weeks, you’ll begin receiving your regular Wide Moat Daily e-mails from:

widemoatresearch@mail.beehiiv.com

widemoatdaily@mail.widemoatresearch.com

You can view instructions on how to white-list those addresses by clicking here.

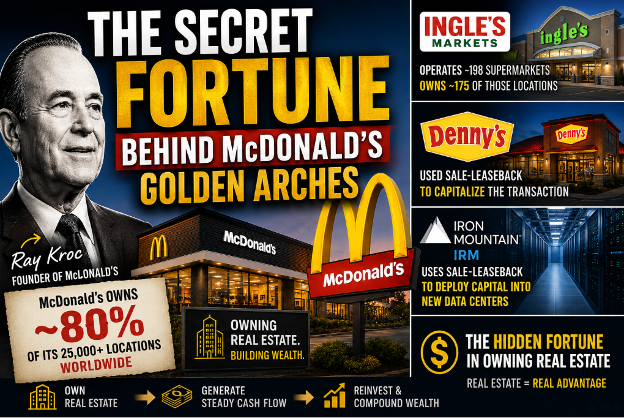

Almost everyone thinks of McDonald’s (MCD) as a fast-food joint. Certainly, that’s what Ray Kroc, McDonald’s first CEO, marketed it as: a place hungry consumers could get hamburgers, fries, sodas, and shakes served lickety-split.

But believe it or not, McDonald’s is also an enormous real estate success story.

Kroc, you see, turned the burger business into a franchise, selling the brand name and business model… while often still owning the underlying land and buildings. As such, he got franchise royalties, property appreciation, and rent all at the same time.

Considering how McDonald’s owns roughly 80% of its more than 45,000 branded stores worldwide – 2,276 of which it just opened last year – that adds up. For 2025, McDonald’s reported:

-

About $22.8 billion in net property and equipment under franchise arrangements, including $7.1 billion of land after depreciation and amortization

-

Around $26.8 billion in revenue

-

Approximately $8.5 billion in net income.

In short, Ray Kroc’s empire is living proof of how powerful real estate can be – even when it doesn’t steal the show.

I’m usually quick to recommend real estate investment trusts, or REITs, whenever I bring up property values. After all, their entire business model is built around bringing out the most in real estate.

I wrote about several of them just last week, including Realty Income (O), the branded and copyrighted “Monthly Dividend Company”…

Federal Realty (FRT), the only REIT dividend king in the world, having raised its dividend for 58 years in a row…

And VICI properties (VICI), a much more recent player that still knows how to conquer the landscapes it enters.

{kind=link}

Source: ChatGPT

Today though, I want to switch gears to McDonald’s-like businesses that keep real estate as their secret weapons. These companies are capable of accomplishing much more than they’re given credit for as a result.

And the same goes for their shares.

Ingles Markets: a Wide Moat Confidential success story

One of the top picks at my small-cap service, Wide Moat Confidential, is Ingles Markets (IMKTA).

At first glance, it looks like a regional grocery chain. One that does very well with its customers, mind you, but a regional grocery chain nonetheless.

Most investors would stop at that assessment, but Wide Moat Research went digging further into its balance sheet. That’s how we found that Ingles owns quite the pretty portfolio of real estate as well.

As I explained in the January 2025 Confidential copy:

Ingles is not just a grocery store. It is that, yes. But it is also a landlord and real estate giant in its corner of the world. Anybody who looks at this business as “just” a supermarket chain is making a mistake.

It owns 175 of the 198 supermarkets it operates, leasing the remaining 23. And while most are freestanding stores, some are entire strip malls.

So along with the money Ingles makes from selling produce, drinks, meats, dairy, and snacks, it also collects rent. That’s a big deal few of its competitors can claim.

This setup creates hidden yet rising value considering how all its grocery-anchored properties are located squarely in Sunbelt markets. And those are getting more and more attractive as people keep fleeing higher-taxed, more heavily restricted states elsewhere.

I’m not actually saying Ingles should sell its real estate, only that it could do so – from a position of significant strength – if it wanted.

If it ever wants or needs to, Ingles could unlock value through strategic sale-leasebacks, selling its properties and using the capital to defend its home turf (since Publix is growing rapidly). Or it could expand its empire by acquiring chains like Lowe’s Food. Other options include property-level financing and redevelopment.

That was one of the reasons we were confident IMKTA had further to run… even while the rest of the market overlooked it as a sleepy grocery store operator.

Sure enough, it’s up 37% since we first recommended it last January. And we still think it has more room to run even now.

How Denny’s hidden real estate became obvious money

Denny’s is another excellent example of how much real estate can add to a company’s bottom line. Back when it was still publicly traded under the ticker symbol DENN, we realized it had a lot more going for it than its menu.

Gone are the days when Denny’s was a hotspot for hungry college students and budget-conscious families. Everyone knows the chain has been struggling, as have its shares.

Normally, that devaluation would make sense. But we saw that Denny’s had meaningful real estate beneath its restaurant properties and corporate headquarters (located in my hometown of Spartanburg, South Carolina).

Approximately $150 million worth of real estate, to be precise. So we opened a position on June 18, 2025.

On November 4, a private equity company came in and bought the business out. And to fund the $620 million deal, these new owners monetized the properties by completing a $145.5 million sale-leaseback transaction.

That’s simply how sophisticated investors tend to think. They don’t just consider earnings before interest, taxes, depreciation, and amortization (EBITDA). They also look at ways to unlock value by utilizing real estate – just like Ray Kroc did when he began expanding McDonald’s.

Since that’s the exact same mindset we have here at Wide Moat Research, we were able to capture 47% gains in around six months.

Iron Mountain’s mission-critical infrastructure

My final McDonald’s-like play is, admittedly, a REIT. However, Iron Mountain (IRM) is a REIT that investors didn’t treat like a REIT for years.

Many still don’t even today.

For those who don’t know, Iron Mountain gives shelf space to government entities, corporations, and wealthy individuals who want to keep their valuables vaulted up. In short, it was glorified self-storage throughout much of its 75-year history.

Fair enough. Except that it was glorified self-storage with several side businesses like document shredding… and massive amounts of real estate.

For years, I’ve argued that the market underestimated those property holdings. In one such article, published on Seeking Alpha in July 2020, I noted how it still had “$2.5 billion of owned real estate at its disposal” that it could easily monetize.

Since that time, Iron Mountain has made multiple sale-leaseback transactions that – sure enough – have helped deploy cheaper capital into more profitable data center sites that don’t jeopardize its REIT standing.

Recognizing how important information storage is becoming compared to its traditional physical storage centers, Iron Mountain is building out its high-tech holdings intensely through:

-

Data centers

-

Cloud infrastructure

-

Digital storage

-

Mission-critical information management

-

Secure logistics.

Once the market began recognizing Iron Mountain as far more than a paper-storage company, the results have spoken for themselves… with shares climbing over 400% since July 2020.

That’s what can happen when you look beyond a company’s obvious business: its burgers, groceries, breakfast platters, or document storage. All of a sudden, you start to see the hard assets quietly compounding value underneath.

As Ray Kroc recognized decades ago, real estate doesn’t have to be the headline business to pay off by supporting durable cash flows, strategic flexibility, and overall shareholder value.

That’s exactly why we continue searching for opportunities where the market sees an ordinary operator… but the balance sheet tells a more valuable story altogether.

Regards,

Brad Thomas

Editor, The Wide Moat Daily

|