Editor’s Note: Within the next two weeks, you’ll begin receiving your regular Wide Moat Daily e-mails from:

widemoatresearch@mail.beehiiv.com

widemoatdaily@mail.widemoatresearch.com

You can view instructions on how to white-list those addresses by clicking here.

As I write this on May 6, 2026, at 1:58 p.m., an impressive 177 out of the S&P 500’s 503 stocks have risen double digits on a year-to-date basis.

The index itself is up by 7.28%, meaning that a fairly wide swath of companies is outperforming. And well over half (289) have posted positive returns across a wide variety of sectors and industries.

All of this points toward a healthy-looking market. Yet what I hear investors talk about is:

-

The narrow breadth of the rally that’s only being driven by big-tech stocks

-

How fragile the double-digit recovery we’ve seen since the March 30 lows is

-

How we’re doomed for a significant selloff because of rampant speculation and circular financing in the artificial intelligence (AI) space.

It’s true the year’s biggest winners so far are almost exclusively tech or AI-adjacent. However, that isn’t necessarily negative.

If anything, the secular tailwinds at play have the potential to boost equity returns for years – if not decades.

I believe the AI revolution is still in its early innings. And that, as it progresses, trillions of dollars will be spent on related infrastructure across the globe.

So, no, I’m not frightened by the pace of the recent rally. On the contrary, I remain bullish on the market’s long-term future.

And I can detail exactly why.

The Mag 7 up close and… sensible?

Because the S&P 500 is a market capitalization-weighted index, its largest members have a greater impact on its performance. Therefore, it does make sense to focus on those largest members’ fundamental health.

So people who highlight the index’s top-heavy nature are correct. They’re just wrong in then demonizing huge market caps.

Looking at these companies’ fundamentals, I don’t think the market is acting irrationally overall. I’ll admit it’s difficult to wrap my head around Tesla’s (TSLA) valuation… but there are strong arguments to be made that most of the other stocks listed below are trading at – or even below – fair value.

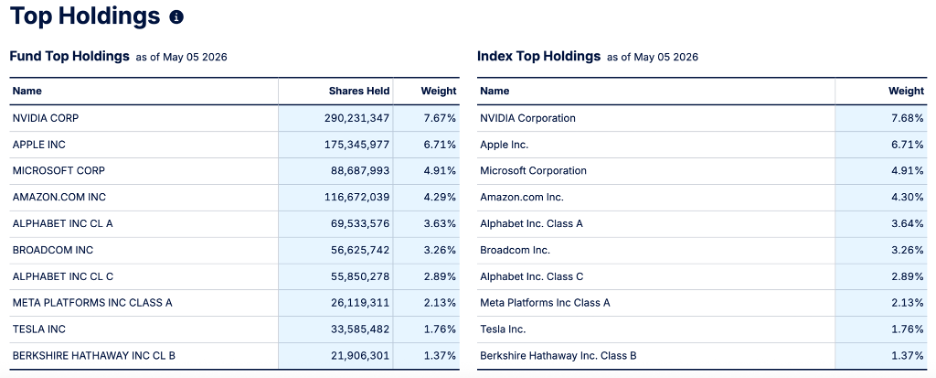

{kind=link}

Source: SPY Investor Relations Website

As you can see, outside of Berkshire Hathaway (BRK.B), each of the Top 10 holdings from the State Street SPDR S&P 500 ETF (SPY) is a technology company.

(Brad Thomas and I discussed big-tech valuations in yesterday’s episode of TheWide Moat Show. If you’re interested in seeing that analysis, click here.)

The so-called Magnificent 7 stocks – Nvidia (NVDA), Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG), Meta Platforms (META), and Tesla – make up about 24.2% of the overall S&P 500…

Whereas entire sectors like consumer staples, energy, utilities, materials, and real estate have low-single digit weightings.

So, yes, Mag-7 earnings results are driving the S&P 500’s performance. But, no, that’s not a bad thing.

Because they’re actually boosting other members as they do.

The big (tech) are getting bigger

There’s no denying that Big Tech companies posted amazing results during the first quarter.

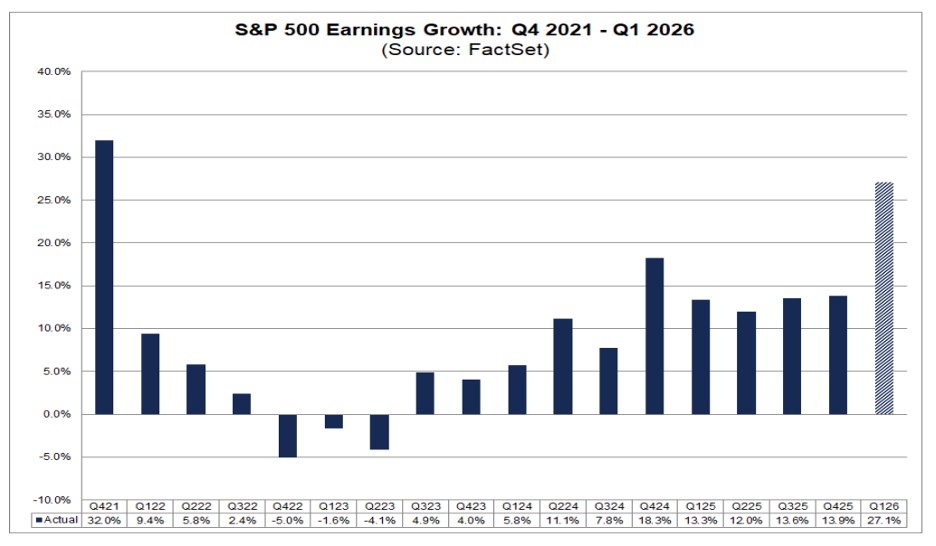

Factset updated its Earnings Insight data on May 1 to account for new Mag-7 data. And that research shows how, during the prior week, the S&P 500’s blended earnings per share (EPS) growth jumped from 15% to 27.1% – largely on the heels of strong earnings reports from Amazon, Alphabet, and Meta.

These three were responsible for 71% of the week-over-week earnings increase.

Factset noted that if that 27.1% increase holds… it will be the strongest earnings growth rate we’ve seen since Q4-21.

{kind=link}

Source: FactSet

Admittedly, a recent Goldman Sachs report pointed out that much of Q1’s progress came not just from Big Tech firms… but more specifically from Big Tech reporting unrealized gains on investments, especially in OpenAI and Anthropic.

But here’s one very valid way to look at that additional information…

Those private companies are growing rapidly, so there’s no reason to believe their lofty valuations will prove irrational. Plus, Goldman noted that even without those paper gains, the S&P 500’S Q1 EPS would have grown roughly 16%.

This still would have represented one of the strongest quarters in years. And it still would reasonably support the market’s current valuation multiple.

What’s most interesting to me about all this is that the S&P 500’s forward price-to-earnings (P/E) ratio right now is 20.9. That is above its trailing five- and 10-year averages of 19.9 and 18.9, respectively. However…

On a price-to-earnings growth (PEG) basis, we’re looking at a sub-1.0 ratio.

Value investors know that a sub-1.0 PEG ratio usually represents a bargain. So there’s a good chance markets continue to climb even higher throughout the rest of the year.

Yet this is not a zero-sum game. Because of the Mag-7 performance, the overall stock market’s earnings growth is the strongest it’s been in years, justifying the double-digit stock market rally we’ve seen these past five weeks.

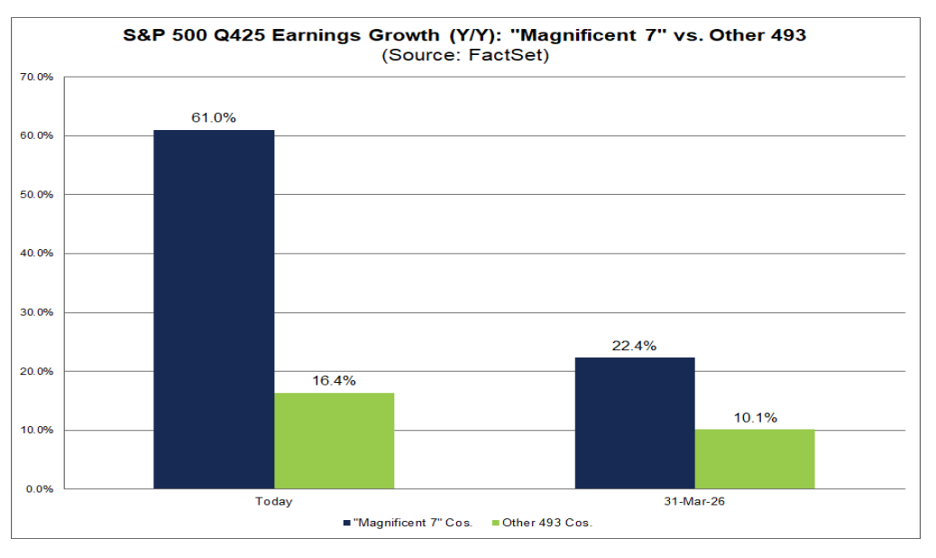

{kind=link}

Source: FactSet

As shown above, Big Tech wasn’t the only group to beat Q1 estimates. So far, most of the non-Mag 7 companies have done so as well.

Not at the same magnitude, mind you, but they’re still looking good.

Earnings Insight data shows that, as of May 1, 63% of the S&P 500 companies had reported Q1 results. An impressive 84% of them posted positive earnings surprises, and 81% of them beat revenue expectations.

What’s driving many of these beats? That would be AI-related capital expenditures (capex) from the Mag-7 stocks.

In short, these companies are actively enabling smaller companies to grow as well.

The capex trickle-down effect

To be clear, capex spending isn’t the only positive force at play. But when you look at the 25 best-performing stocks from the S&P 500 index, it’s clear that companies involved in the global AI infrastructure buildout are the biggest beneficiaries of today’s economic trends.

{kind=link}

Source: Slickcharts.com

This is the trickle-down effect of hyperscalers spending hundreds of billions of dollars on AI investments every quarter.

That understandably worries some people who wonder what will happen if Big Tech reins in its spending. But after reading through the big-tech earnings reports last week, it very much appears that investors should stay bullish.

Because those numbers just continue to rise…

-

During its Q1 report, Meta increased its 2026 capex guidance from between $115 billion and $135 billion to $125 billion and $145 billion.

-

Alphabet raised its guidance range by $5 billion to a low of $180 billion and a high of $190 billion.

-

Microsoft now expects around $190 billion – a 61% increase from the year before.

-

Amazon is projecting $200 billion – about a 50% increase over 2025.

Put together, these four companies could spend more than $700 billion on AI projects in 2026. And since Amazon, Alphabet, and Microsoft alone are seeing a combined cloud backlog of $1.3 trillion even now…

Capex could pass the $1 trillion mark as well next year.

We’re still in the early innings

All things considered, this appears to be a Field of Dreams situation in terms of data centers and demand for compute capacity. “If you build it, they will come.”

Many of the best and brightest people on Earth work for these companies. And I highly doubt they’d be spending hundreds of billions of dollars if they weren’t confident these investments would pay off.

Moreover, this isn’t just circular financing, as has been alleged. That $1.3 trillion is coming from hundreds, if not thousands, of clients across the globe.

Sure, the big names like OpenAI and Anthropic are at the front of the line with their mega orders. But even if their allocated data center/cloud capacity becomes available to buy, you don’t think others won’t scoop it up immediately?

Theres no denying we’re in a global race toward artificial general intelligence (AGI) right now. The world’s largest companies – and countries – can’t afford to miss this trend. And they know it.

People can point to the dot.com boom and subsequent crash if they want. But there are clear differences in the current tech buildout.

The hyperscalers driving this momentum today are some of the strongest, most profitable companies on Earth. They were all highly capitalized coming into the AI boom. They’re already reaping the rewards…

And there’s every indication those rewards will keep pouring in.

Kind regards,

Nick Ward

Analyst, Wide Moat Research

|