Every day, countless investors log into their brokerage accounts to check the price of the stocks they hold.

I get it… Green numbers make you feel good. And when the market is rallying like it has most of this year, that can give you peace of mind.

But as soon as a bear market arrives… the resulting red numbers can drive you crazy.

But what if I told you those red and green numbers showing share price don’t matter?

That there’s a data point you can use to make money… No matter how the stock market is performing.

To me, it’s the only one that matters.

There is one key, though. You must select the right kind of companies to benefit from that peace-of-mind number.

In today’s essay, I’ll tell you what this data point is that matters more than share price… Why it means you don’t need to worry about the day-to-day volatility in the stock market… And some great places to find these kinds of companies.

Share Price Is Not the Most Important Number

Let me use the example of one of my favorite stocks to illustrate what I mean: Lowe’s (LOW).

Lowe’s is a retail stock focused on home improvement. There’s nothing flashy about its lumber, plumbing, or garden offerings…

But Lowe’s operates more than 1,700 stores. And it’s one of the 10 largest box-retail stores in the country, along with Walmart, Costco, and Target.

Its size and scale, combined with a strong market share, has produced outstanding results over the decades.

Lowe’s generated more than $97 billion in sales last year. And that just continues a long streak of making profits.

Over the last 20 years, it’s grown its bottom line (measured by earnings per share, or EPS) 17 times.

Even more impressively, Lowe’s has produced double-digit EPS growth during each of the last 10 years.

Lowe’s shares are up by 367% during the last decade. Comparatively, the S&P 500 is up by 163% over the same period.

But the year ahead is causing concern for some investors.

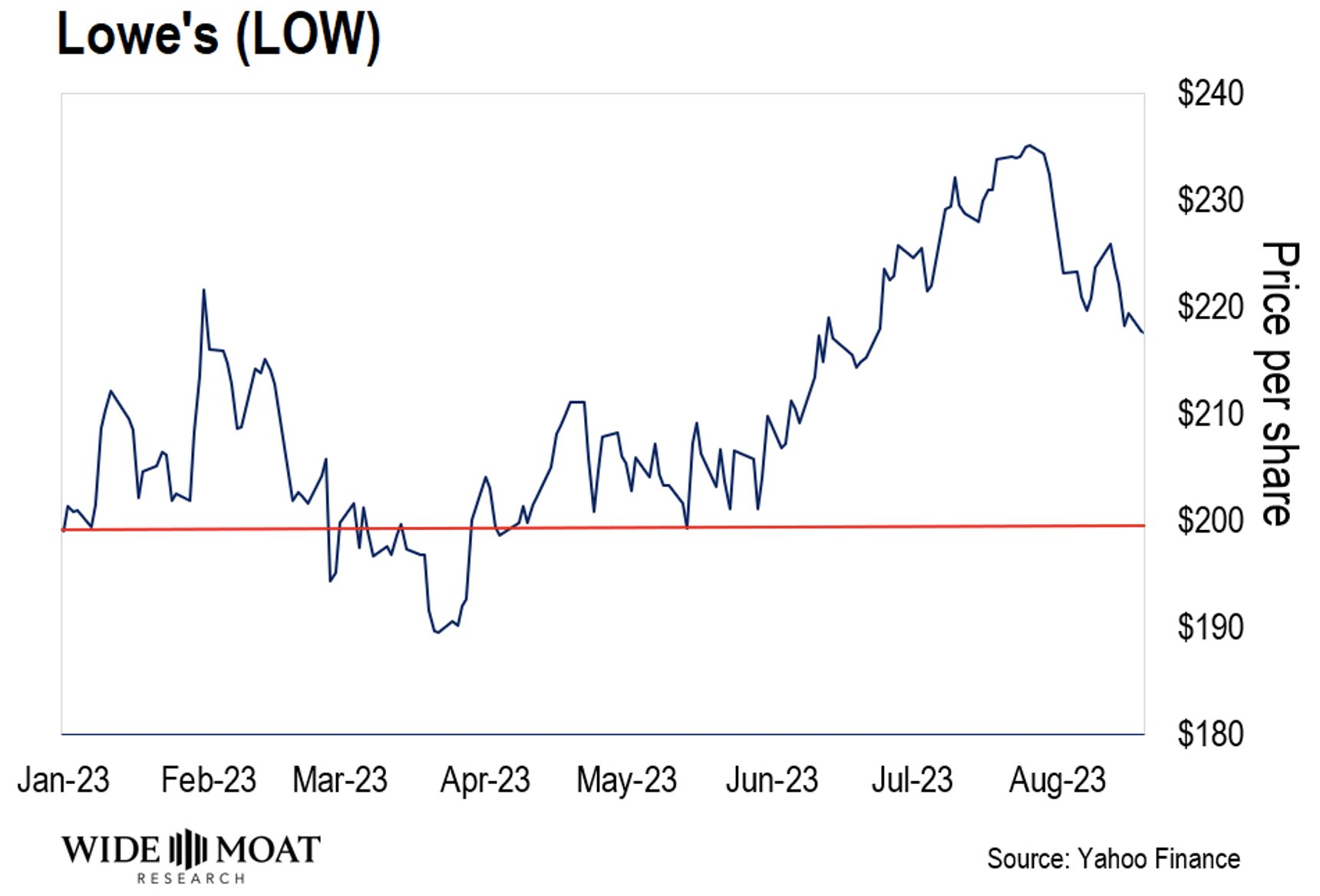

Lowe’s is expecting to see sales fall by roughly 9% this year due to higher interest rates hurting the housing/construction markets. That’s made its share price movements volatile this year.

It dipped below its 2023 opening price earlier this year. And although it’s risen in recent months, it’s predicted to dip below where it started the year again.

But investors who get caught up on one bad year will miss the bigger picture.

Here’s what is most important to keep in mind when it comes to a company like Lowe’s…

The Magic of Dividends

The best way we know to reliably make money from the stock market is not to try and time to highs and lows… But to buy and hold shares of great companies.

And it’s not because of their capital gains, but instead, because of their growing dividends.

That’s right, when you focus on dividend growth, share price doesn’t matter anymore.

Because you don’t just own a company like Lowe’s… you get paid to own it.

Right now, every quarter, Lowe’s pays $1.10 for every share. That’s around a 2% dividend yield. It may seem small now, but it adds up quickly – especially considering how much Lowe’s consistent performance has grown that dividend.

The company has raised its annual dividend now for 61 consecutive years. That’s longer than I’ve been alive…

Over the past two decades, it’s grown that dividend 25% annually – on average.

Lowe’s stock price goes up and down daily. But as you can see below, its dividend only trends in one direction.

Looking ahead, Lowe’s should continue to provide investors with double-digit annual dividend growth.

That’s why I don’t worry about Lowe’s relatively low 2% yield today – or a volatile share price.

Based on its trajectory, our yield on cost (that’s the dividend yield we will get based on today’s share price) will go much higher.

If Lowe’s grows its dividend at a 10% annual clip (which is a conservative estimate that’s less than half its long-term average)…

Then in 15 years, someone buying shares today will be looking at a yield on cost of approximately 8%.

And if it can maintain a 20% annual growth rate like we’ve seen in recent years… That would mean a 32% yield on cost in 15 years.

At that point, with dividends, Lowe’s pays you back almost one-third of your original investment every year.

Lowe’s is a proven company that’s been around for decades. And while I don’t expect its share price to go down 32% in the next few years… Its growing dividend gives investors a cushion to weather any kind of volatility.

And it’ll keep exponentially growing over time.

This is the kind of security I look for in sleep-well-at-night (SWAN) investments.

And it’s why I’d rather pay attention to the perfect stair-step pattern on Lowe’s dividend growth chart than its volatile share price movement any day.

Lowe’s is one of many companies we own in our Intelligent Income Investor portfolio that offers a 10-year-plus dividend growth streak.

Since launch, our dividend income has grown every year. And due to our focus on dividend safety and growth, we expect that to continue for years to come.

To get the names of our favorite dividend growth stocks to own today and stop worrying about seeing green one day and red the next… click here.

Happy SWAN investing,

Brad Thomas

Editor, Intelligent Income Daily