It’s not often you pick a fight with a massive hedge fund, but that’s what I did back in 2013.

At the time, Highfields Capital wasn’t impressed with Digital Realty Trust (DLR), a data center-specific real estate investment trust (“REIT”).

“Pricing is going lower,” Highfields’ founder and then-CEO Jonathon Jacobson told members of the 18th Sohn Investment Conference that May. “Competition is increasing, and the company is tapping into capital markets as aggressively as they can.”

This was the leader of one of the world’s biggest hedge funds speaking at the so-called “Superbowl of investing conferences.” So it was a very big deal.

But I wasn’t impressed.

Hedge funds had a bad habit of dumping on REITs back then, seeming to have no idea how they worked. Jacobson specifically asked attendees if they really wanted “to pay three times book value” for Digital Realty back then.

That alone showed his ignorance on the subject.

In response, I wrote an article titled “Highfields Capital Is Wrong… This Digital Cloud REIT Ain’t Going Nowhere but Up.”

From that write-up:

In REIT-dom, book value (and related price-to-book ratios) are… virtually useless for REITs. A more common metric is net asset value (NAV) since this valuation is a much better estimate of market value. Furthermore, an intelligent investor would also consider the most common way of calculating a REIT stock: P/FFO (or price to funds from operations).

That’s because real estate needs to be handled and calculated very differently from other assets. There are different considerations and, in the case of REITs, different legalities they operate under.

As for Digital Realty specifically, it was “a massive railroad of this generation, providing the infrastructure to support the global economy.” And data centers in general were only going to get more relevant, I argued in 2013. It was foolish to bet against the movement.

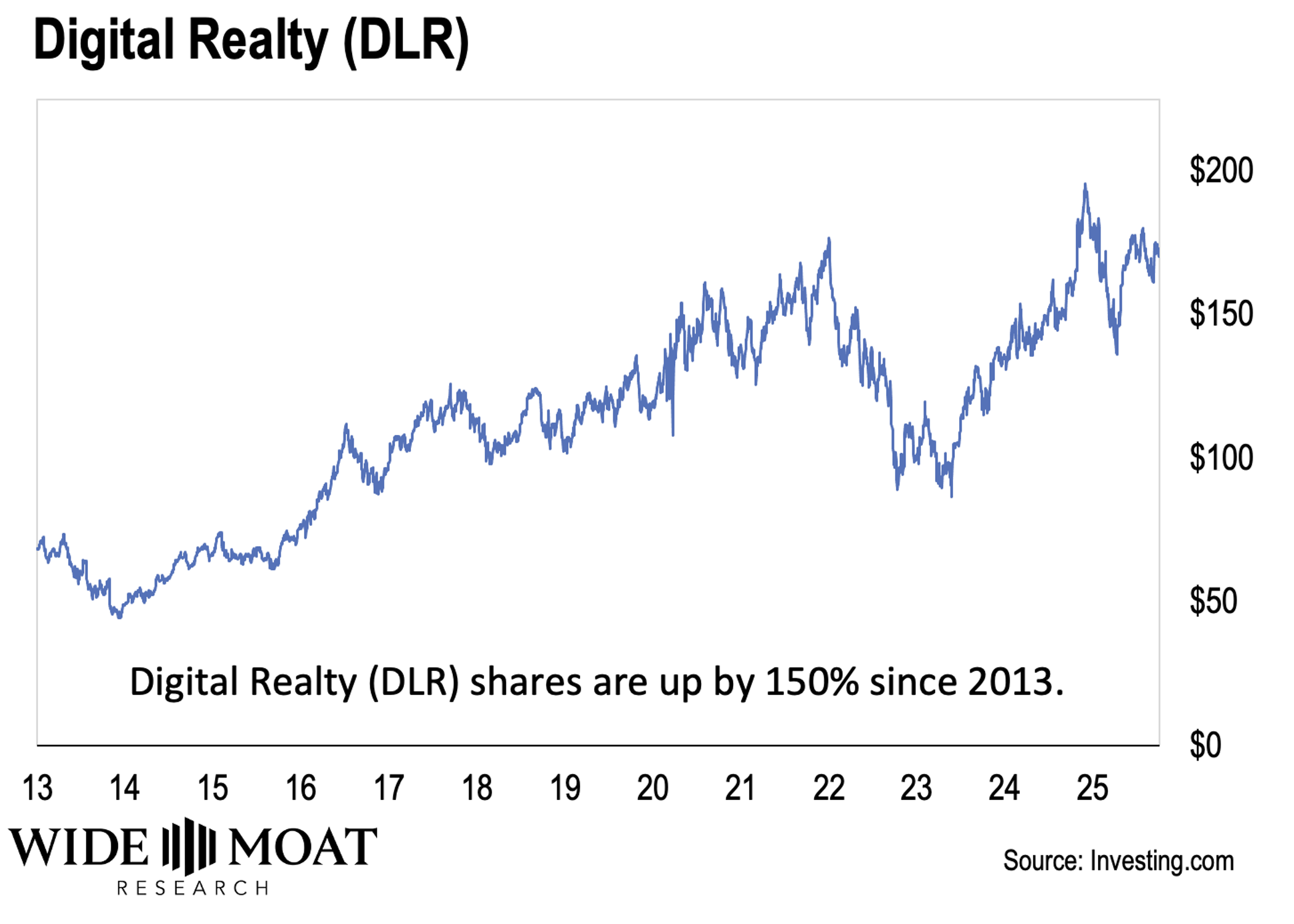

Now 12 years later, it’s very clear how right I was.

The Data-Center Basics

Today, data centers are front and center for investors’ minds. That’s largely thanks to the buildout of artificial intelligence. But for anybody paying attention, this was a trend that should have been spotted over a decade ago. The adoption of cloud-based applications in the 2010s could only mean one thing – more data centers. And that’s why I’ve been following the space for more than a decade.

My 2021 book, The Intelligent REIT Investor Guide, explains how:

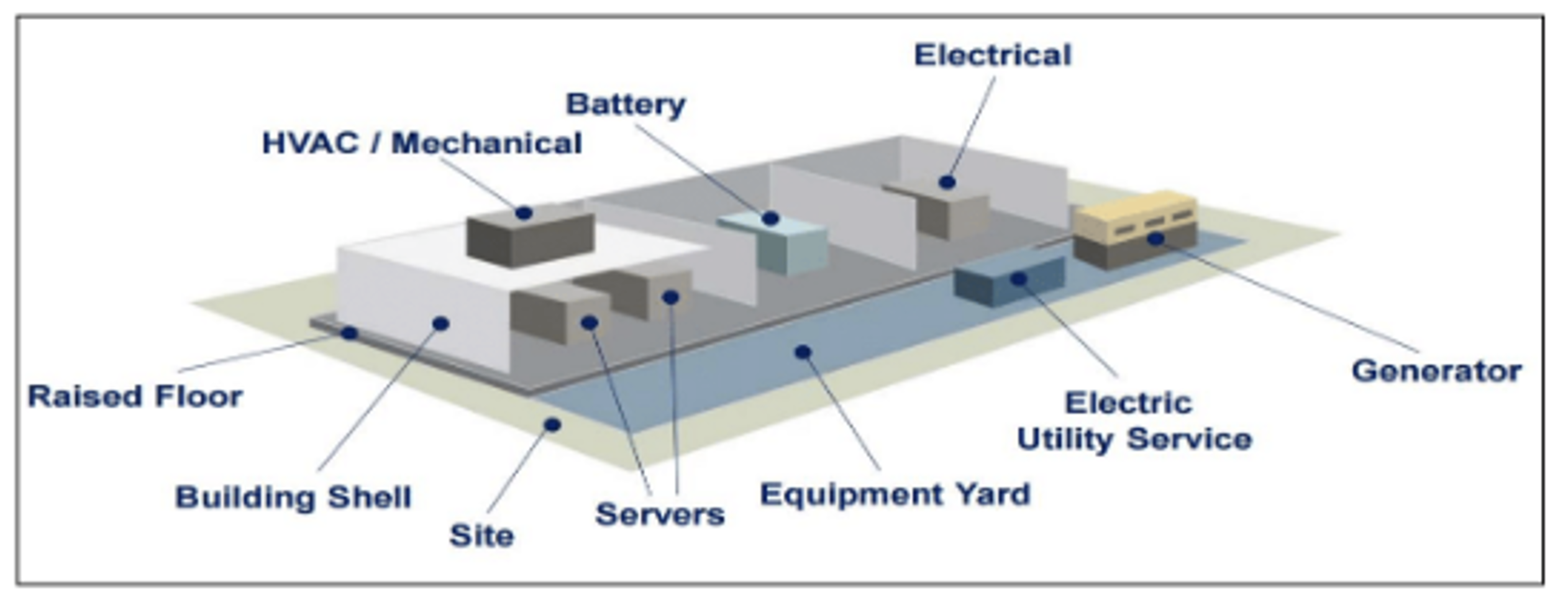

Data centers are very specialized real estate facilities that house computer servers and network equipment within a highly secure environment. They come complete with redundant mechanical cooling, electrical power systems, and network connections. You can think of them almost as microwaves to “cook” all the data that’s generated.

In other words, these data center landlords own the building, the power, and the cooling infrastructure, and exchanges and cross-connections, while their customers provide their own servers, storage, and networking equipment.

Source: Data Center Components/Wide Moat Research

They’ve played an important and growing role in societies around the world for decades. (The first data center was actually built in 1945.) But the more technologically connected we become, the more we rely on these sites.

Artificial intelligence, has driven data-center demand more than ever. To quote my June 26 article, “The REIT Way to Own Mission-Critical Data Centers“:

Artificial intelligence requires enormous amounts of data and compute to operate. And while the data AI consumes in its quest to “learn” already exists, it then produces even more.

That information needs to be processed and stored somewhere… which is why McKinsey Quarterly predicts global data-center demand could almost triple between now and 2030.

‘The rise in AI workloads could propel about 70% of this demand,’ it explains. ‘To handle these loads, data centers will need more than $5 trillion in capital expenditures.’

That also means big, big business for data center REITs and the rising number of other REITs looking for their piece of that pie. As Highfields Capital noted all those years ago, yes, competition is growing in this field.

It’s just that demand is growing even faster.

So, if you feel like you might have missed out on the data-center investment trend, I promise you haven’t. And there are a handful of data-center REITs that every investor should know about.

The Pure-Play Data-Center REITs

The already introduced Digital Realty was the first data-center REIT to complete an IPO in 2004. But even then, that was as a C-corporation. It didn’t make the legal conversion into a REIT until January 1, 2014.

Regardless, Digital Realty has grown steadily by developing new sites, acquiring properties, and enacting mergers. This includes purchasing:

- A smaller REIT known as DuPont Fabros for $7.6 billion in 2017

- Latin American data-center holder Ascenty for $1.8 billion in 2018

- European data-center provider Interxion for $8.4 billion in 2019

- Telx Computers for $1.9 billion this year.

Source: Wide Moat Research

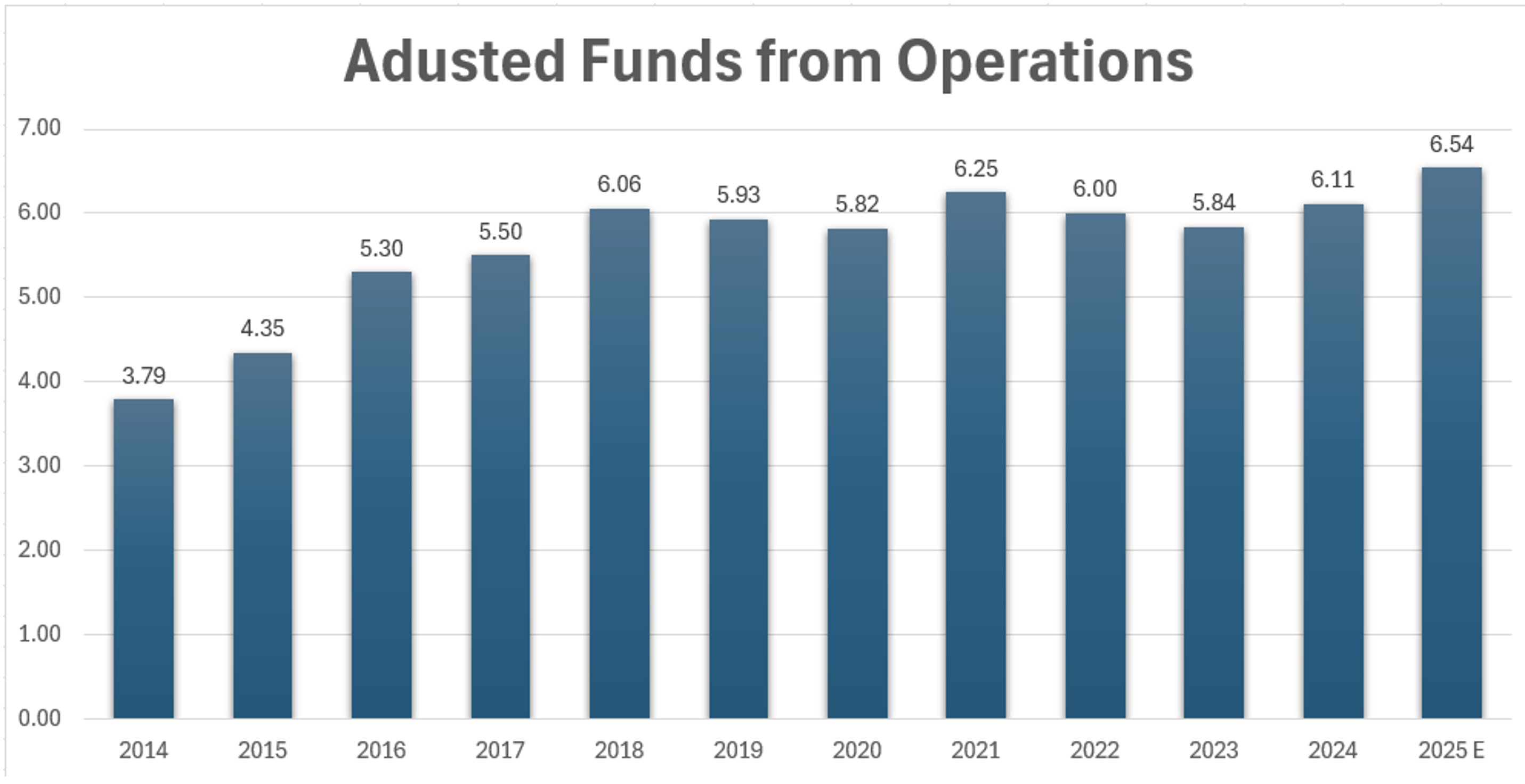

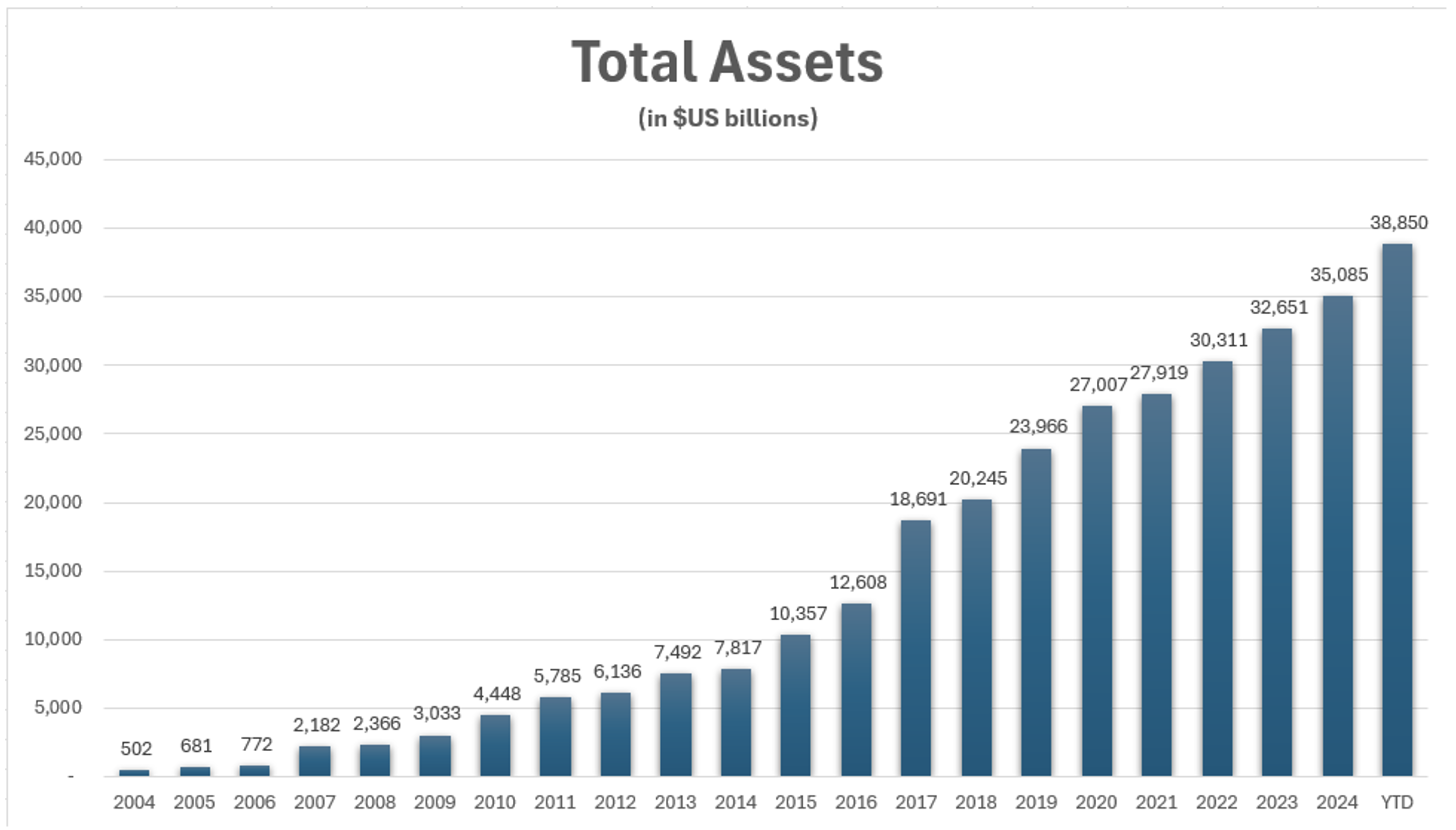

Since 2014, Digital Realty has generated steady adjusted funds from operations (“AFFO”), increasing at a 5.4% compound annual growth rate (“CAGR”). Analysts are forecasting a greater 8% in 2026 and 10% in 2027.

Source: Wide Moat Research

You’ll also want to know about Equinix (EQIX), which became a REIT on January 1, 2015. Since that time, it has completed numerous mergers and acquisitions, including:

- TelecityGroup in 2015 for $3.8 billion

- Metronode in Australia in 2018

- GPX India and Bell Canada in 2020

- Main One in West Africa in 2021

Source: Wide Moat Research

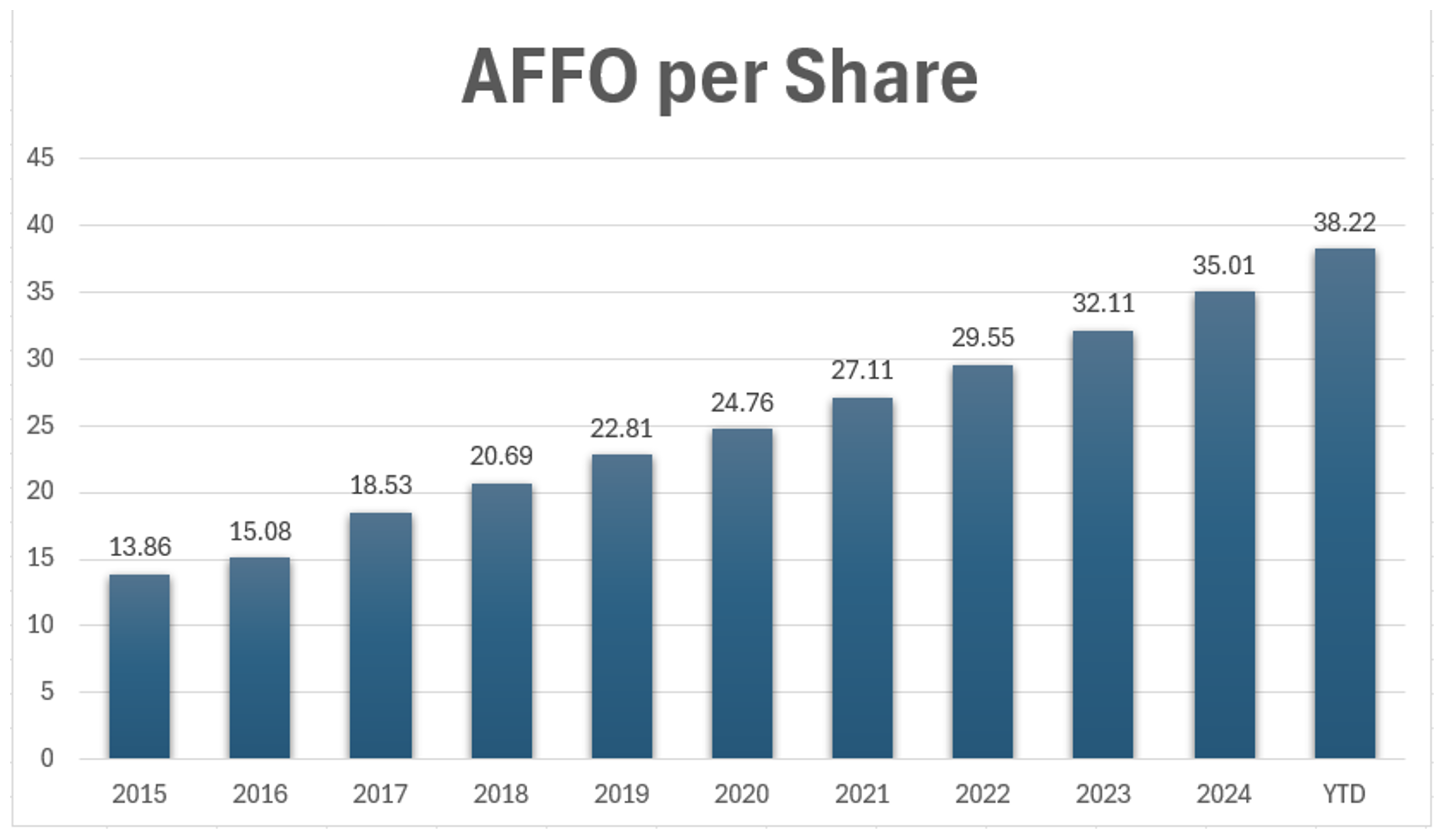

Equinix has generated steady growth in earnings (AFFO per share) of 10.7% CAGR as a REIT. Analysts are forecasting growth of 5% in 2026 and 7% in 2027.

Source: Wide Moat Research

Other Data-Center Players to Know About

There were more data-center names at the turn of the decade, such as QTS Realty and CyrusOne. But Blackstone (BX) purchased the former in August 2021 for $10 billion. And KKR (KKR) and Global Infrastructure Partners bought out CyrusOne in March 2022 for $15 billion.

That same year, cell-tower REIT American Tower (AMT) purchased the data-center portfolio of another significant player, CoreSite. That consisted of 25 data centers, 21 cloud on-ramps, and over 32,000 interconnections for $10.1 billion. As of today, it has 30 data centers in all.

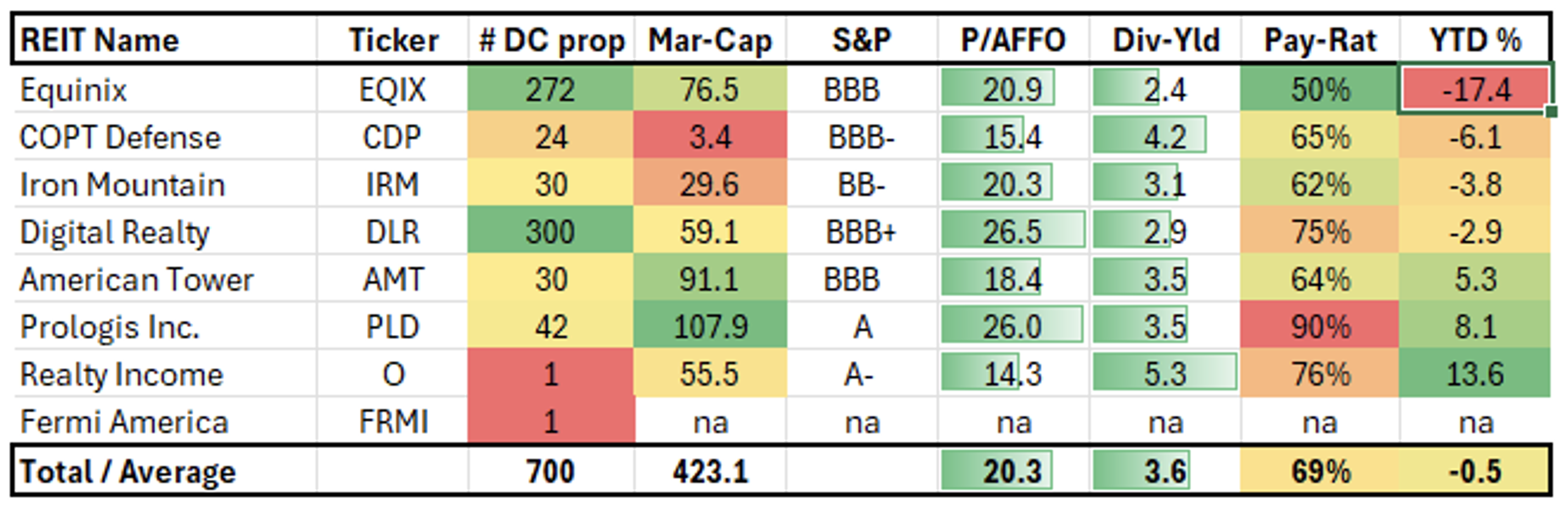

Other REITs that have entered the data-center sector include:

- Iron Mountain (IRM) with 30 data centers

- Realty Income (O), a net-lease REIT, with one after a joint venture deal with Digital Realty

- COPT Defense Properties (CDP) with 24 data centers

- Prologis (PLD), an industrial REIT, with 42 data centers

Source: Wide Moat Research

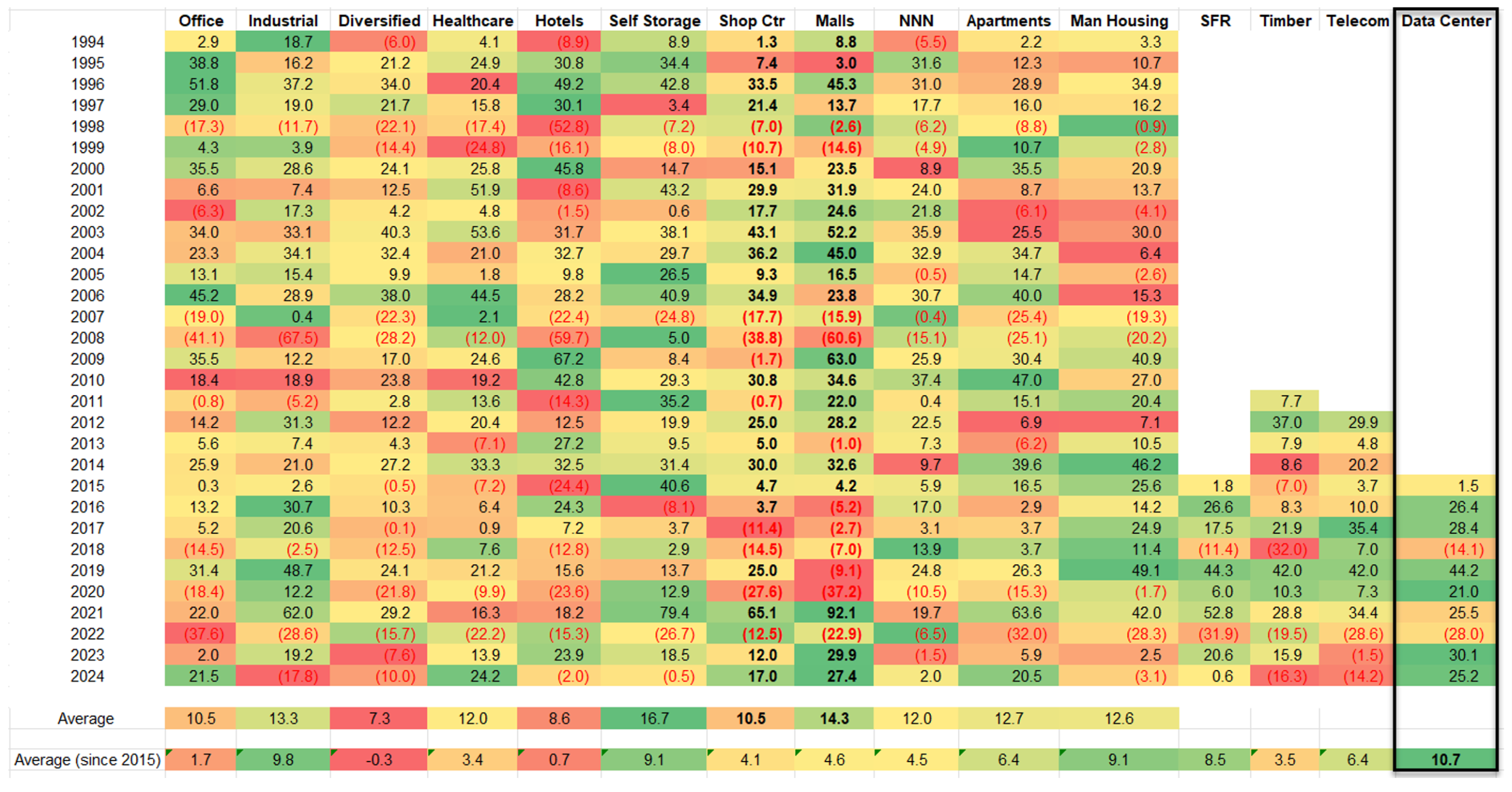

Altogether, data-center REITs have generated an average annual return of 10.7% from 2015 to 2024. That makes them the top-performing REIT sector during this period.

Source: Wide Moat Research

The New Data Center on the Block

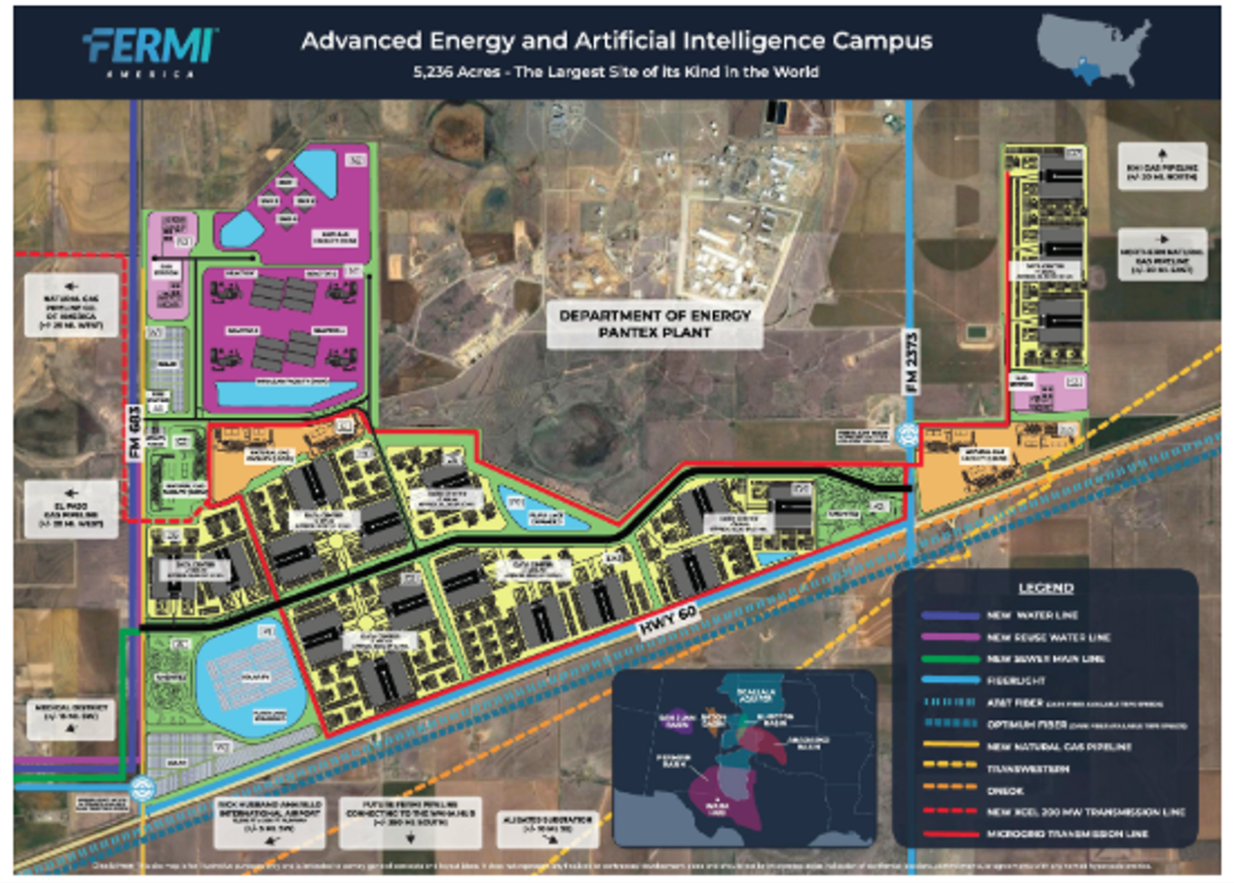

There is one more data-center REIT I need to mention: Fermi (FRMI).

Founded on January 10, 2025, Fermi is co-founded by former Texas Governor and Energy Secretary Rick Perry. The company held its IPO yesterday and is now valued in the neighborhood of $13 billion.

Fermi’s portfolio will consist of a single, massive 6,000-acre energy and data-center campus within 12 years. It’s currently being built within the Texas Tech University system outside Amarillo, Texas, on a ground lease.

When completely finished, the facility should be able to house 18 million square feet of AI-specific data centers, powered by nuclear energy, natural gas, wind, and solar power. In the shorter term, Fermi is aiming to have 1.1 gigawatts of power online by the end of next year.

The site is located near major natural gas pipelines and fiber data lines. It’s also next to the U.S. Department of Energy Pantex plant, described as “the nation’s primary nuclear weapons center.”

Source: Fermi S-11

I’m intrigued by Fermi; I’m not going to lie. But it’s clearly in the very early stages of its existence, so I can’t recommend it today.

(The company offered 32.5 million shares priced at $21 toward the upper end of its expected range of $18 to $22 late Tuesday, resulting in gross proceeds of $83 million. UBS, Evercore ISI, Cantor, and Mizuho are acting as book-running managers on the offering.)

For the time being, we’ll just add it to our Wide Moat coverage spectrum. I always want to have at least several years’ worth of operational data to analyze, so let’s consider this the starting point of that initial investigation.

It should be interesting to see what happens from here!

Regards,

Brad Thomas

Editor, Wide Moat Daily

PS: Tune in to The Wide Moat Show next week (and every week), where we’ll expand on the technology sector outside of data-center REITs. While you’re at it, be sure to subscribe so you never miss an issue. We’ll be celebrating 10,000 followers very soon, and I’d love for readers to join us over on YouTube.