Tomorrow, we’ll learn the Federal Reserve’s decision – one way or the other.

Then again, there’s not much suspense this time. The Fed is all but certain to cut its key rate.

That’s because, as I’ve been sharing, the situation in the jobs market is getting dire. Almost one million jobs for most of last year and the first part of this one were, apparently, a mirage. The Bureau of Labor Statistics revised total job growth down by 911,000.

One of the Fed’s mandates is “maximum employment.” And even though inflation is still on the warmer side, the central bank basically has not choice – it must cut. The futures market agrees. As of this writing, traders are assigning a 100% probability to a rate cut tomorrow.

And as the Fed goes lower, rates across the entire economy should fall, all else equal. That’s good news for rate-sensitive assets like real estate investment trusts (“REITs”). That’s why I’ve covered several real estate sectors in recent issues.

We’ve already covered health care, triple net, and even ground leases. Today, let’s look at one more.

And I’ll start by asking you a question…

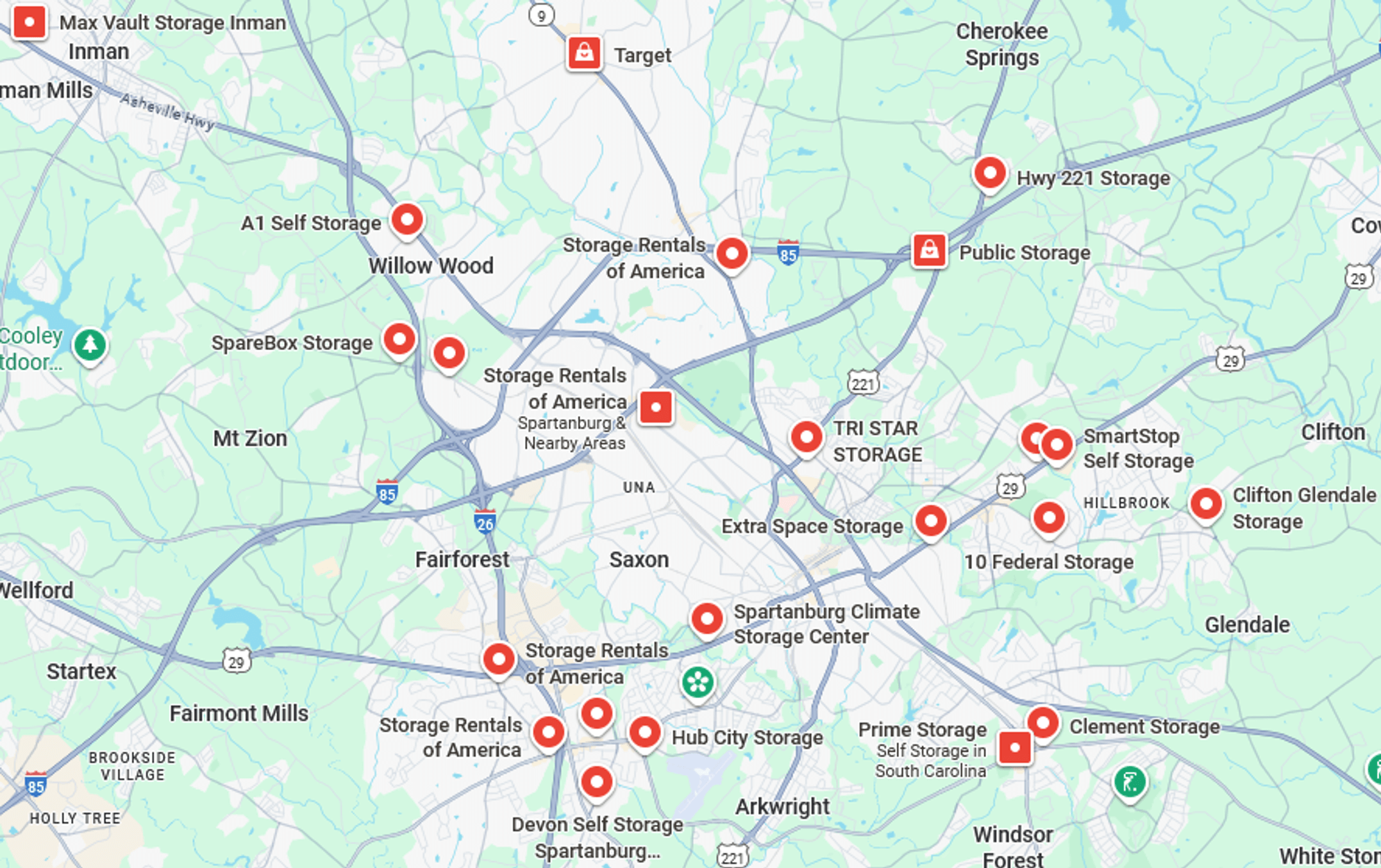

How many self-storage facilities do you have in your area?

No, really. Do a quick search. I did, and here’s what I found in the Spartanburg, South Carolina area.

Source: Google Maps

That’s 21 locations in about a 14-square-mile radius. There are so many of them, in fact, that it’s easy to take them for granted.

But that doesn’t mean you should.

Even with how oversaturated the market seems to be, self-storage facilities can actually be great investments. As I write in REITs for Dummies:

These buildings are cheap to build, cheap to maintain, and cheap to operate. Plumbing isn’t an issue, after all. Temperature controls are, but to a lesser degree (pun intended). Employee counts are minimum. And owners don’t have to worry about changing the carpet whenever there’s tenant turnaround. All they have to do is sweep the floor to prepare for the next lessees to arrive.

That makes them ideal for mom-and-pop owners. So, it makes sense that the vast majority of the 50,000 self-storage facilities throughout the United States are owned by individuals instead of corporations. Which means you can’t really invest in them.

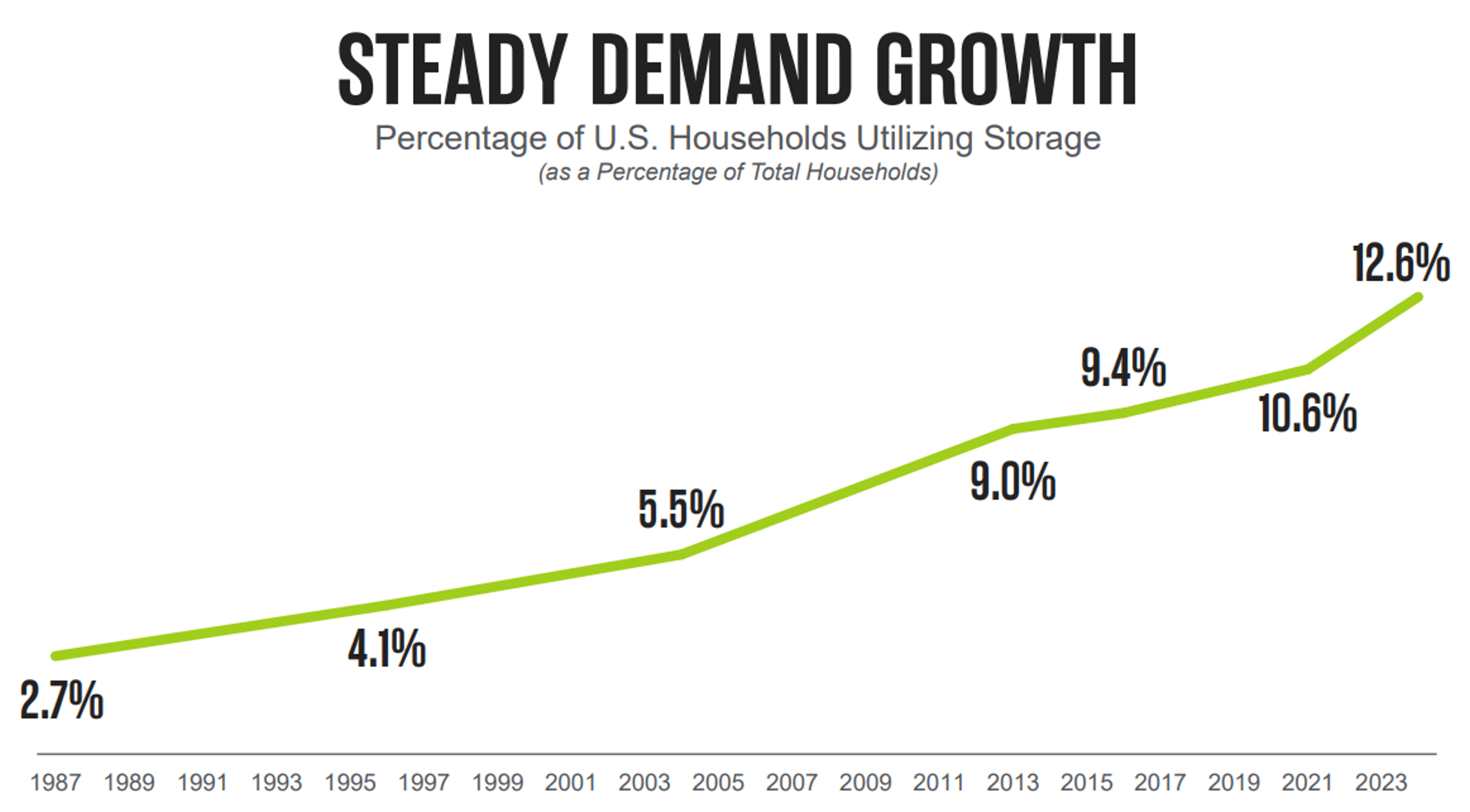

However, there is a type of REIT that does operate exclusively in this space. And they can make excellent portfolio additions. As shown below, the self-storage REIT sector has seen steady demand over the past three decades:

Source: Extra Space

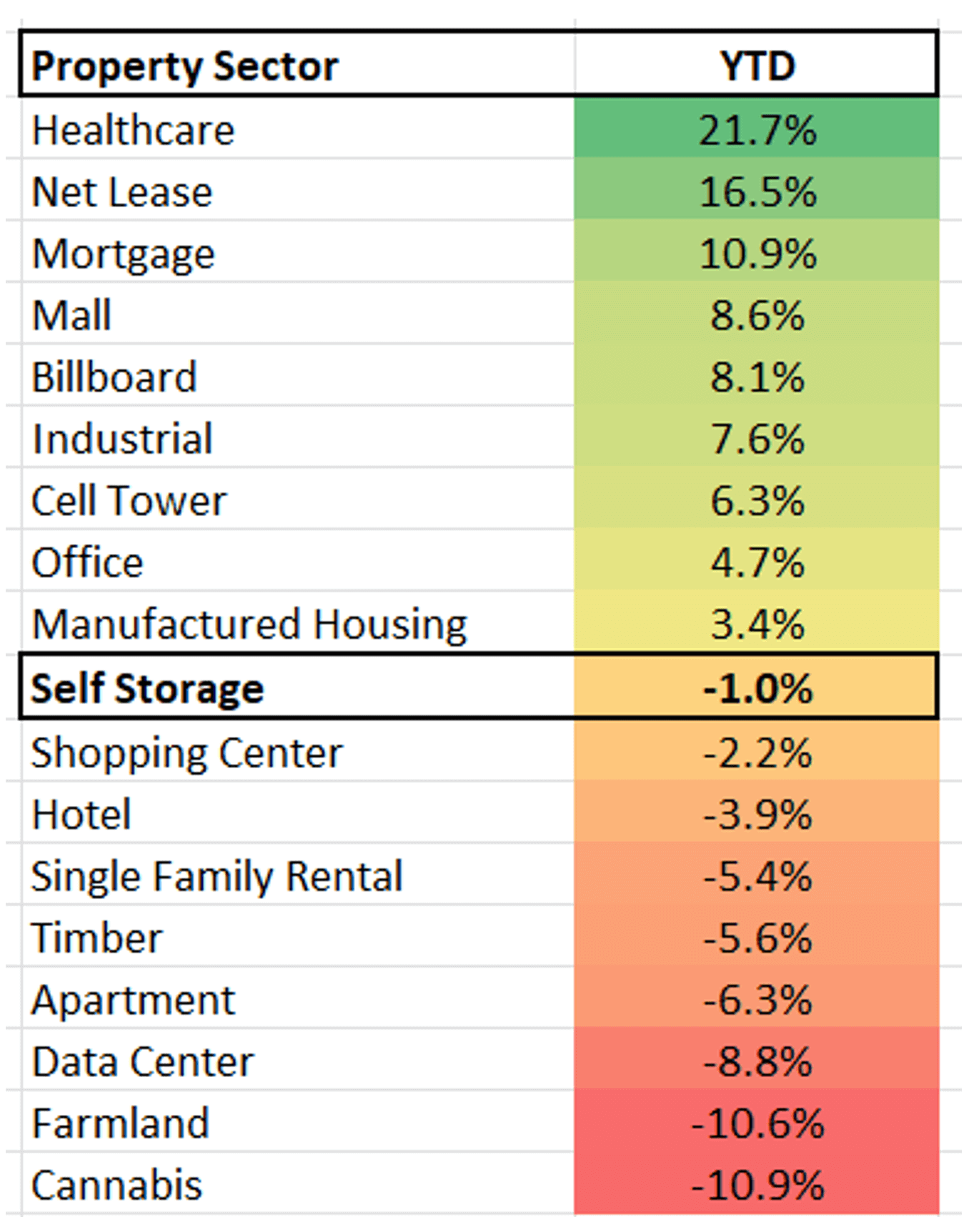

They’re obviously booming businesses. Yet you wouldn’t know that by how their stocks are trading, down 1% year to date (“YTD”) on average.

Source: Wide Moat Research

That’s in large part due to higher interest rates, which tend to affect REITs badly across sectors. Investors automatically (and incorrectly) assume their business models, which do rely heavily on loans, can’t function well when borrowing costs more.

But, as mentioned above, rates are set to fall. In which case, now might very well be the time to act on the three self-storage REITs below.

Self-Storage REIT No. 1: Public Storage

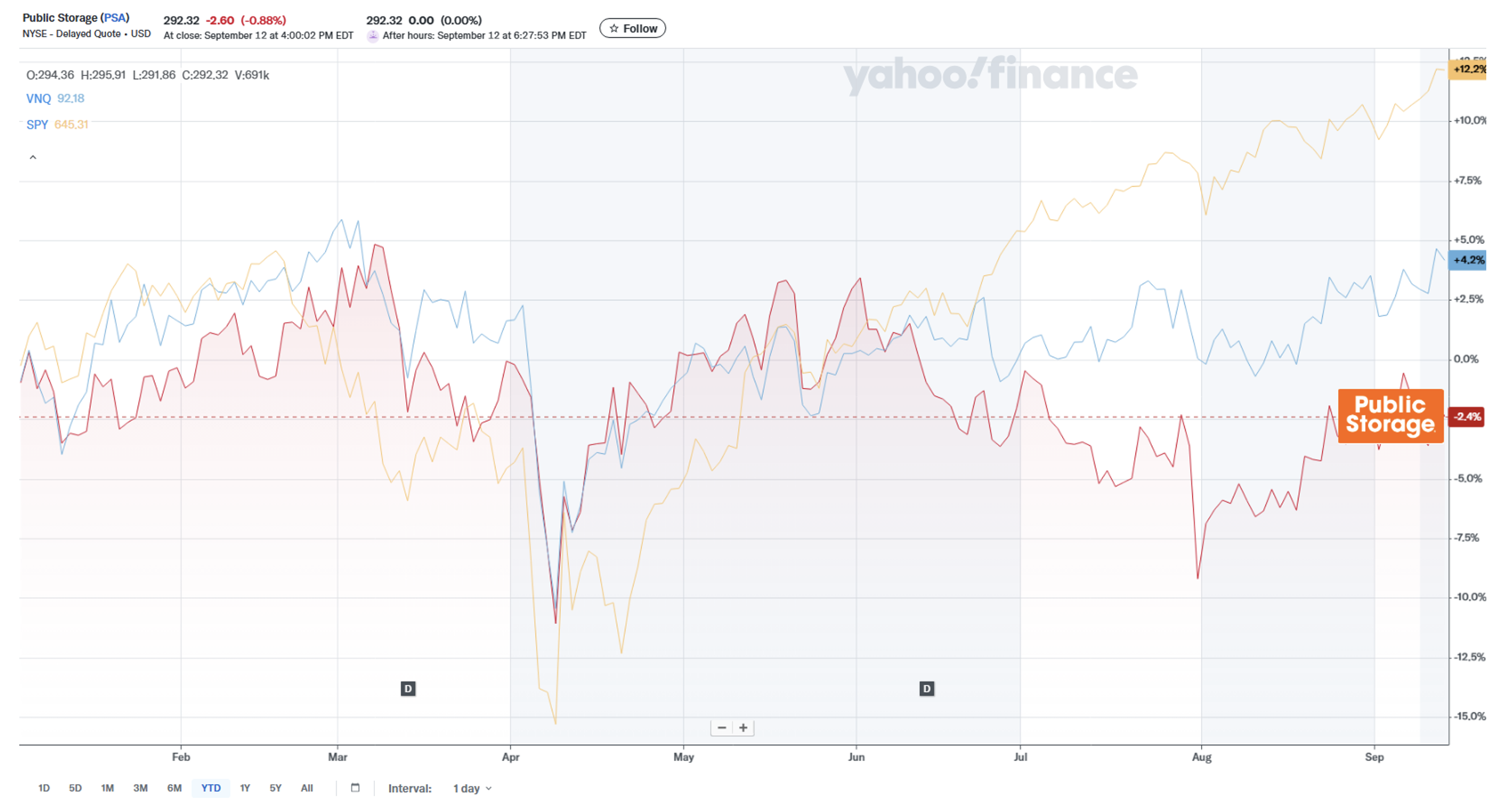

Public Storage (PSA) has more than 3,300 facilities across the U.S. and around 2 million customers. With a market cap of over $51 billion, it’s an S&P 500 constituent and a top 10 holding in the Vanguard Real Estate Index Fund (VNQ).

Yet, as you can see below, Public Storage has underperformed both so far this year.

Source: Yahoo Finance

All the same, I admire it for its moat advantages of scale and cost of capital. It’s effective at delivering strong operational upside by using its sophisticated omnichannel platform that maximizes revenue and increases customer conversion.

The result: It has the most profitable net operating income margins in the sector at 79%.

Public Storage also boasts a fortress investment-grade (A2/A) balance sheet and strong credit metrics. Its net debt and preferred equity to earnings before interest, taxes, depreciation, and amortization (EBITDA) ratio is a solid 4.1 times. And its cost of in-place debt and preferred equity sits at 3.5%.

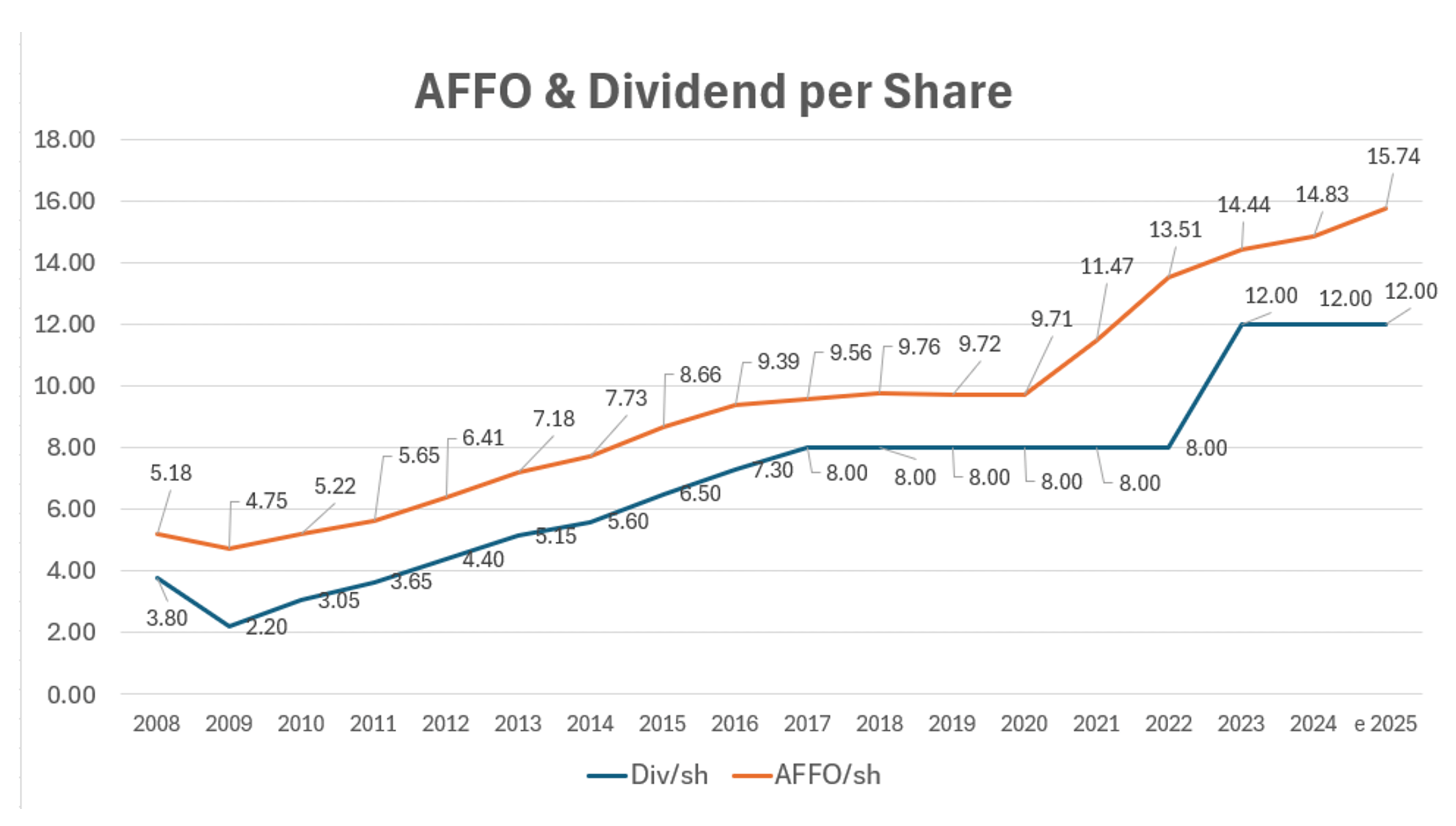

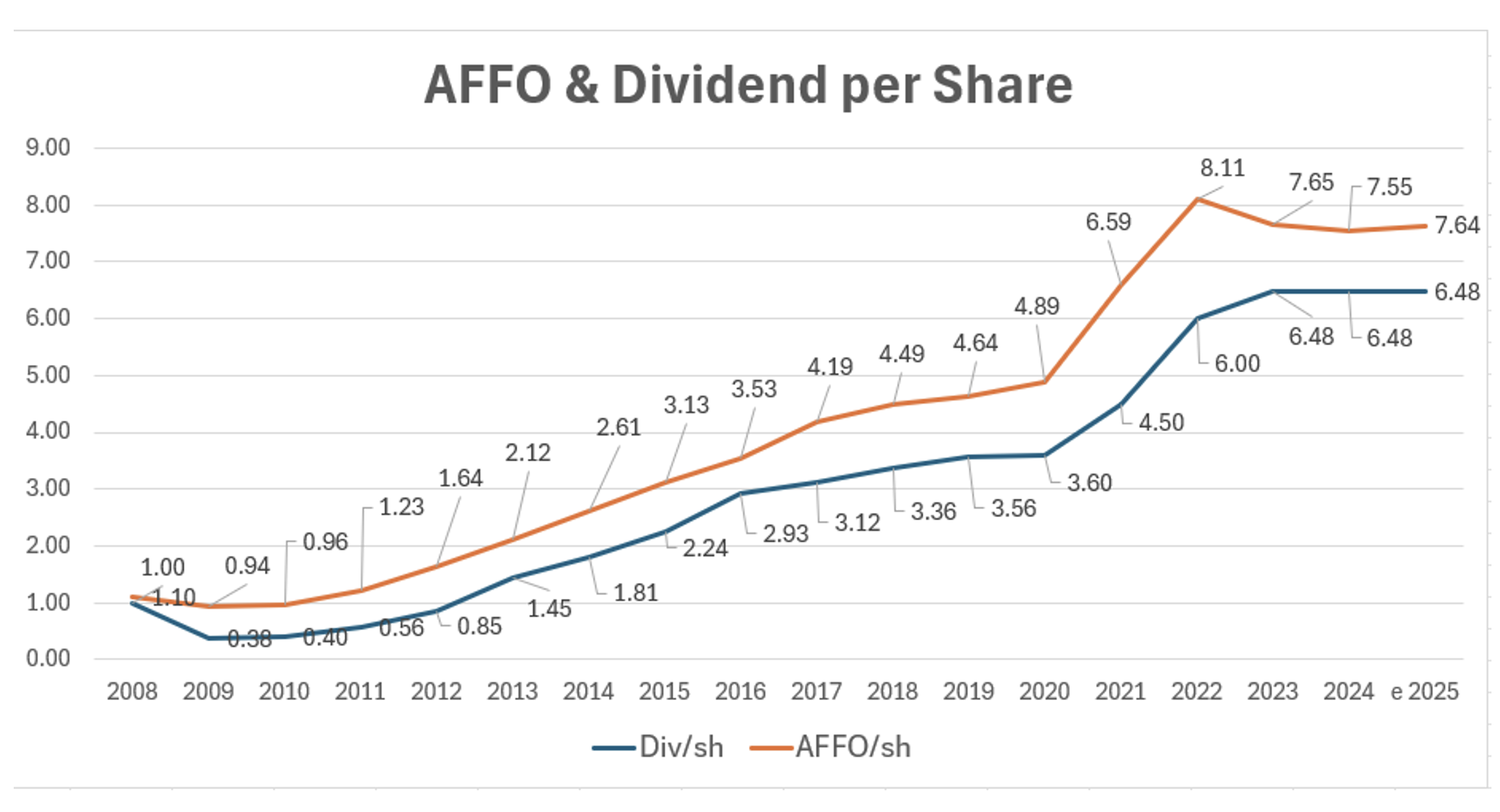

These quality fundamentals have allowed Public Storage to generate impressive dividend growth and earnings per share, as measured by adjusted funds from operations, or AFFO.

Source: Wide Moat Research

Although Public Storage cut its dividend during the Great Recession, it has since delivered solid earnings growth. A 7.8% compound annual growth rate (“CAGR”) over the past 15 years is nothing to sneer at. Nor is a 10% dividend CAGR.

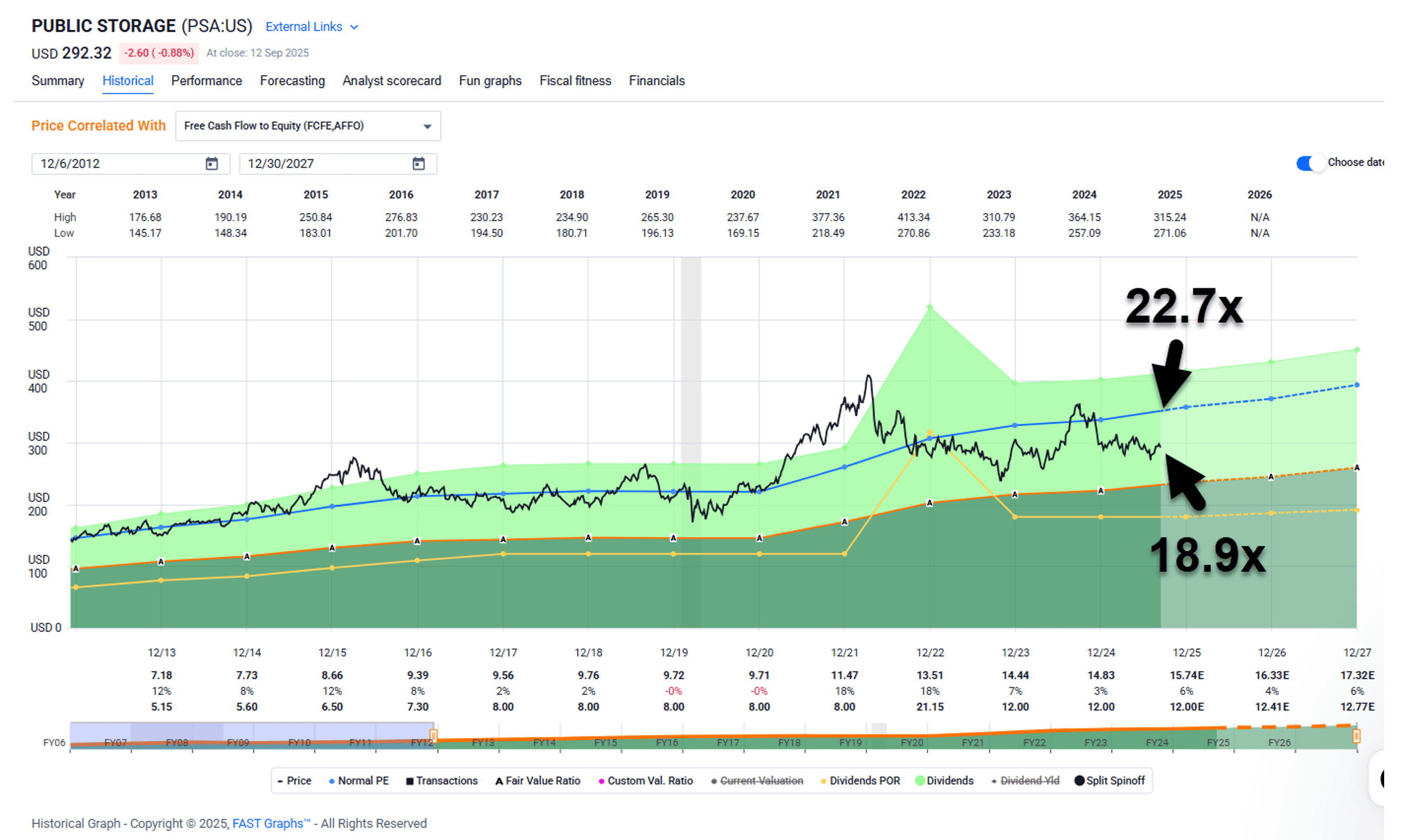

With growth intact and a consensus of 6% for 2025, 4% next year, and 6% in 2027, I find Public Storage an attractive bet. Shares are trading at 18.9 times versus its normal price-to-AFFO valuation multiple of 22.7 times.

Its dividend yield is 4.1%, and I’m forecasting Public Storage to return 20% over the next 12 months.

Source: FAST Graphs

Self-Storage REIT No. 2: Extra Space Storage

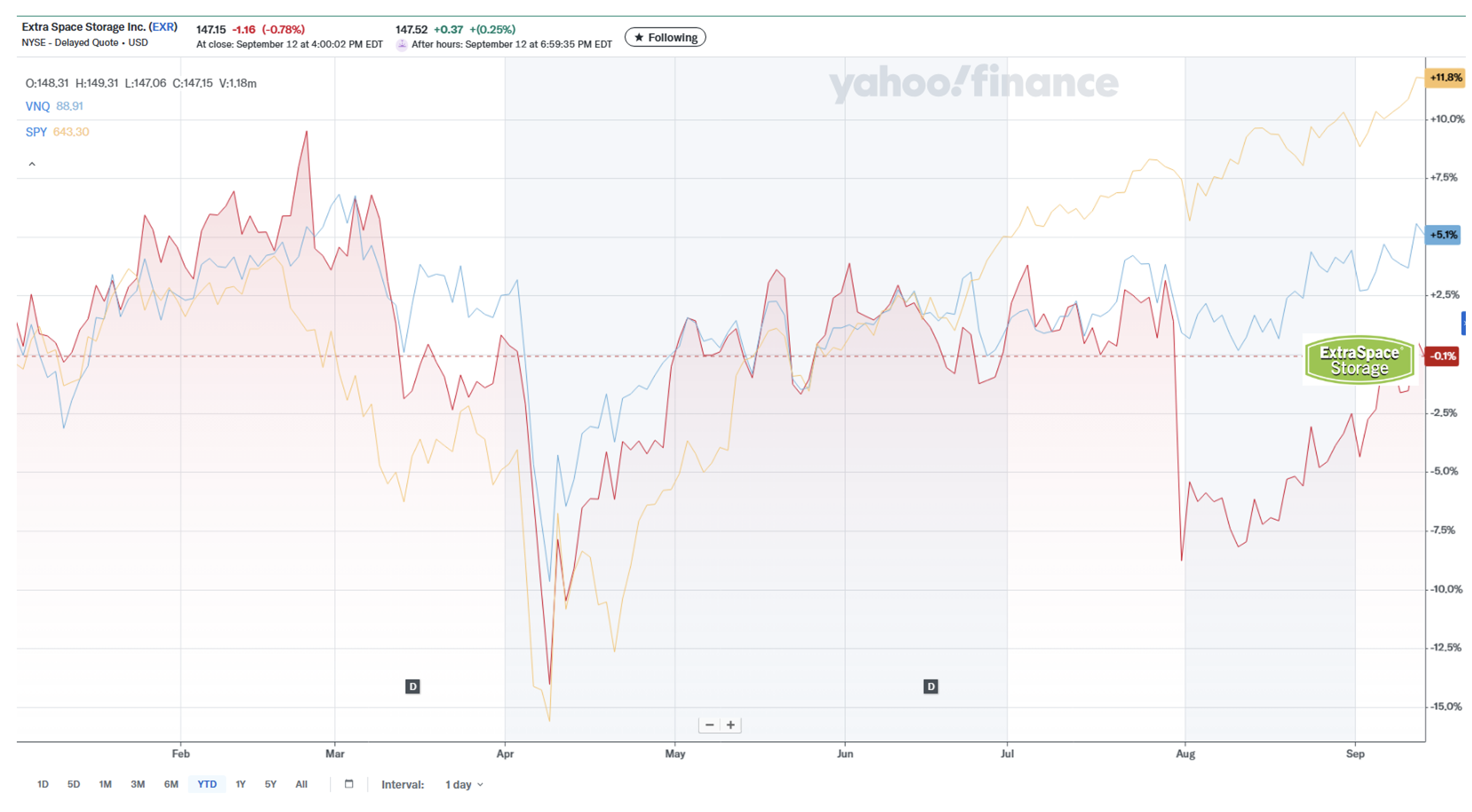

Extra Space Storage (EXR) owns or manages 4,179 properties serving 2.8 million customers. With a $31 billion market cap, it’s another member of the S&P 500 and a top 15 VNQ constituent… that has also seen its shares underperform for the year.

Source: Yahoo Finance

But Extra Space shares a fourth detail in common with Public Storage: It has built a wide moat by achieving scale while simultaneously maintaining a solid balance sheet.

Extra Space has generated high operating margins by increasing rents and lowering capital expenditure costs. And that has resulted in high funds available for distribution along with consistent and predictable dividend growth.

To grow its footprint, this REIT has also maintained a disciplined, rock-solid balance sheet (Baa2/BBB+) with strong credit metrics. It features a 5.2 times net debt-to-EBITDA ratio and a 4.3 times interest-rate coverage.

Like Public Storage, Extra Space did cut its dividend in 2009. However, just look at what it has done since…

Source: Wide Moat Research

Over the past 15 years, Extra Space has grown AFFO per share by 15.5% CAGR. And its dividend has grown by a whopping 22% CAGR.

That growth has certainly cooled down, mind you. Analysts estimate a mere 1% bump in 2025 and 4% in 2026. Even so, shares are too cheap to ignore, trading at 19.3 times versus their normal 22 times, with a 4.4% dividend yield.

Given the potential for multiple expansion, I’m forecasting shares to return 15% to 20% over the next 12 months.

Source: FAST Graphs

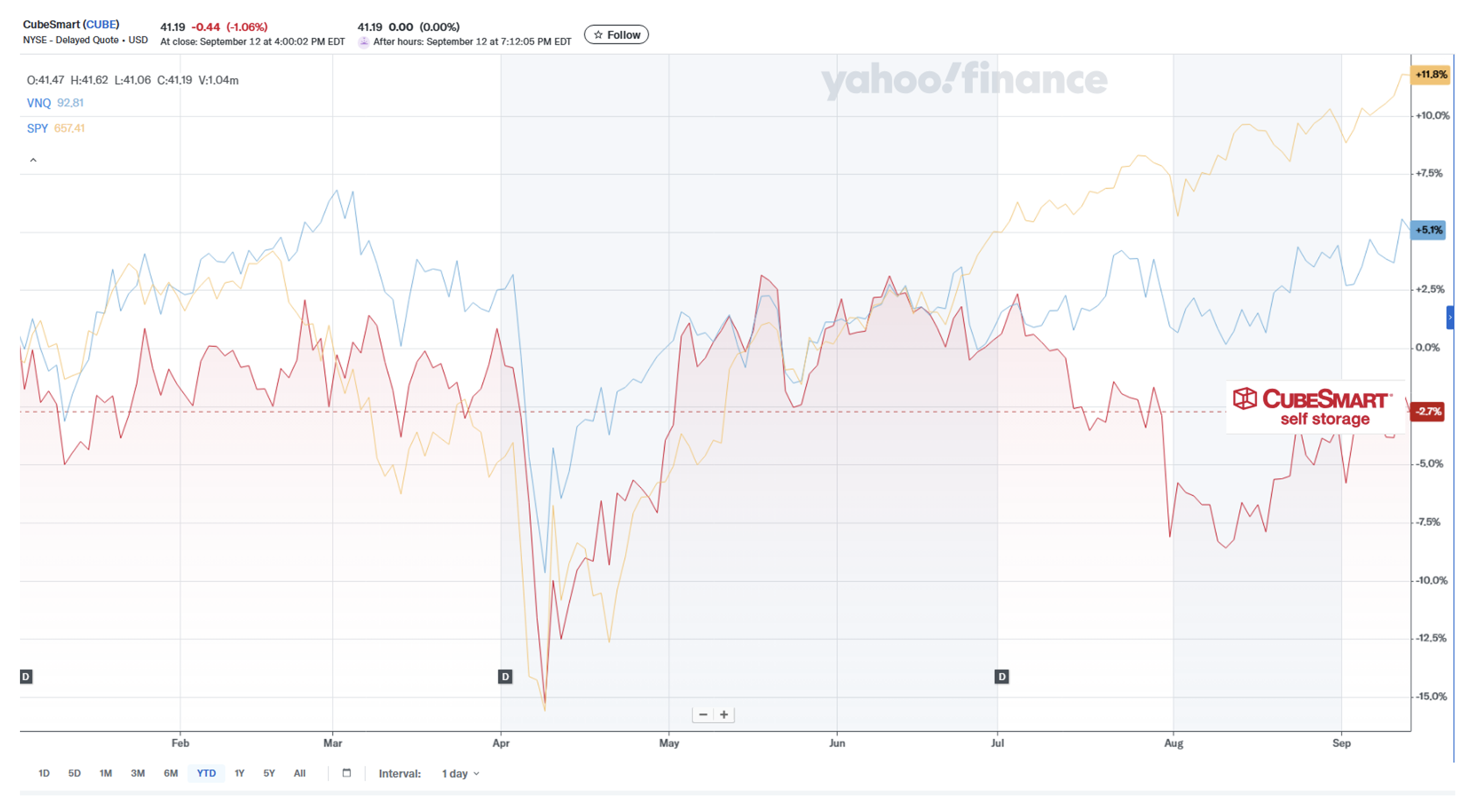

Self-Storage REIT No. 3: CubeSmart

With a $9.39 billion market cap, CubeSmart (CUBE) owns over 1,500 self-storage properties across the U.S. That makes it the third-largest owner and operator of such facilities.

The REIT is differentiated by its strategic focus on submarkets that have the most attractive demographics for stable, long-term demand trends. Yet, once again, it’s underperforming year to date.

Source: Yahoo Finance

Like its larger peers, Cube Smart enjoys a sophisticated technology-enhanced platform that drives efficiency. This allows it to employ cutting-edge strategies that maximize revenue via real-time pricing decisions.

And that attracts significant demand across channels.

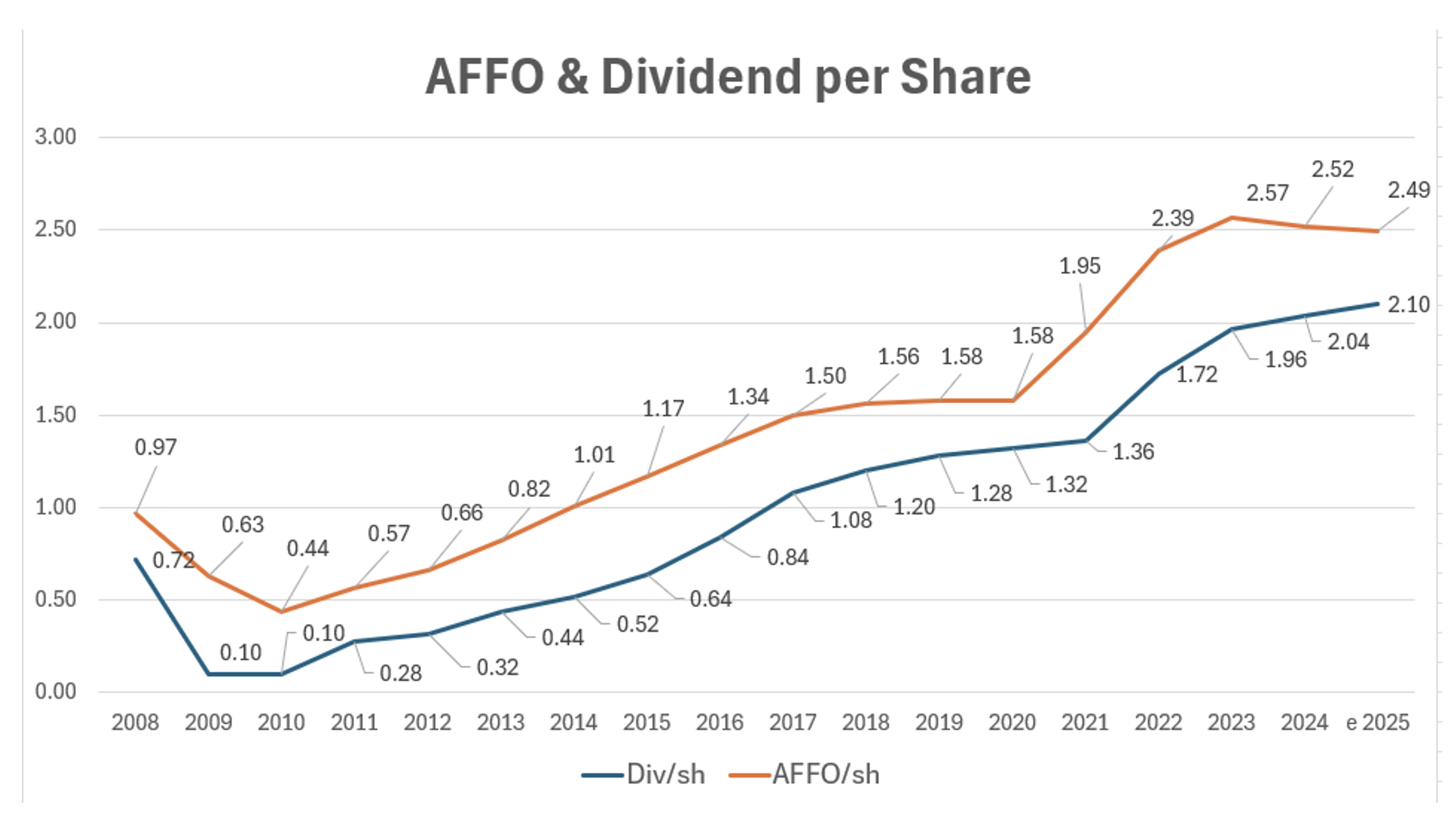

Since the Great Recession, when CubeSmart slashed its dividend by a whopping 86%, it has done a great job of scaling its business model. Over the past 15 years, it has seen best-in-class dividend growth – in excess of 26% CAGR!

Source: Wide Moat Research

In terms of value, CubeSmart is a solid sector pick, with shares trading at 16.5 times compared with its normal 20.2 times. Its dividend yield is 5.1%, and I’m modeling shares to return 15% to 20%.

Source: FAST Graphs

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Tune into this week’s episode of The Wide Moat Show on YouTube for a bonus self-storage pick you might want to know about… and one you probably should avoid.

|