Last week, Lauren Thomas (yes, that’s my daughter) broke a big story for The Wall Street Journal.

Activist investor Land & Buildings Investment Management, led by founder and CEO Jonathan Litt, is pressuring Six Flags Entertainment (FUN) to make some big changes. Utterly unimpressed with the theme-park operator’s stock – of which it holds around 2% – Land & Buildings believes there are readily available avenues to boost its worth.

As proud as I am of my daughter, this isn’t just for parental bragging rights. This is a story I’ve been following for years. And it’s a good example of how leveraging real estate assets can potentially provide a catalyst for an otherwise lagging business. That’s a setup we look for from time to time in our paid services.

Here’s the details…

Spin-Out or Sell

I’ve been following FUN for years. Which means I know this isn’t the first time Land & Buildings has proposed drastic shifts to its status quo.

Back in December 2022, for instance, Litt pushed similar demands: Six Flags should either sell its properties for a fast infusion of cash… then rent the land from the new owners. Or it should spin them off into a real estate investment trust (“REIT”).

Perhaps Litt read my Seeking Alpha article from July 2019. A sale-leaseback arrangement, I argued, made “perfect sense” considering FUN’s “sub-investment-grade” status. Plus, its “overall cost of capital” was “higher than” the yield on cost it “would get in the debt and equity marketplace.”

These alterations clearly haven’t happened, hence Land & Buildings’ first and second interventions. But it was successful in prompting Six Flags to merge operations with Cedar Fair in July 2024. Litt also got FUN’s board to begin an official search to find a new CEO back in March.

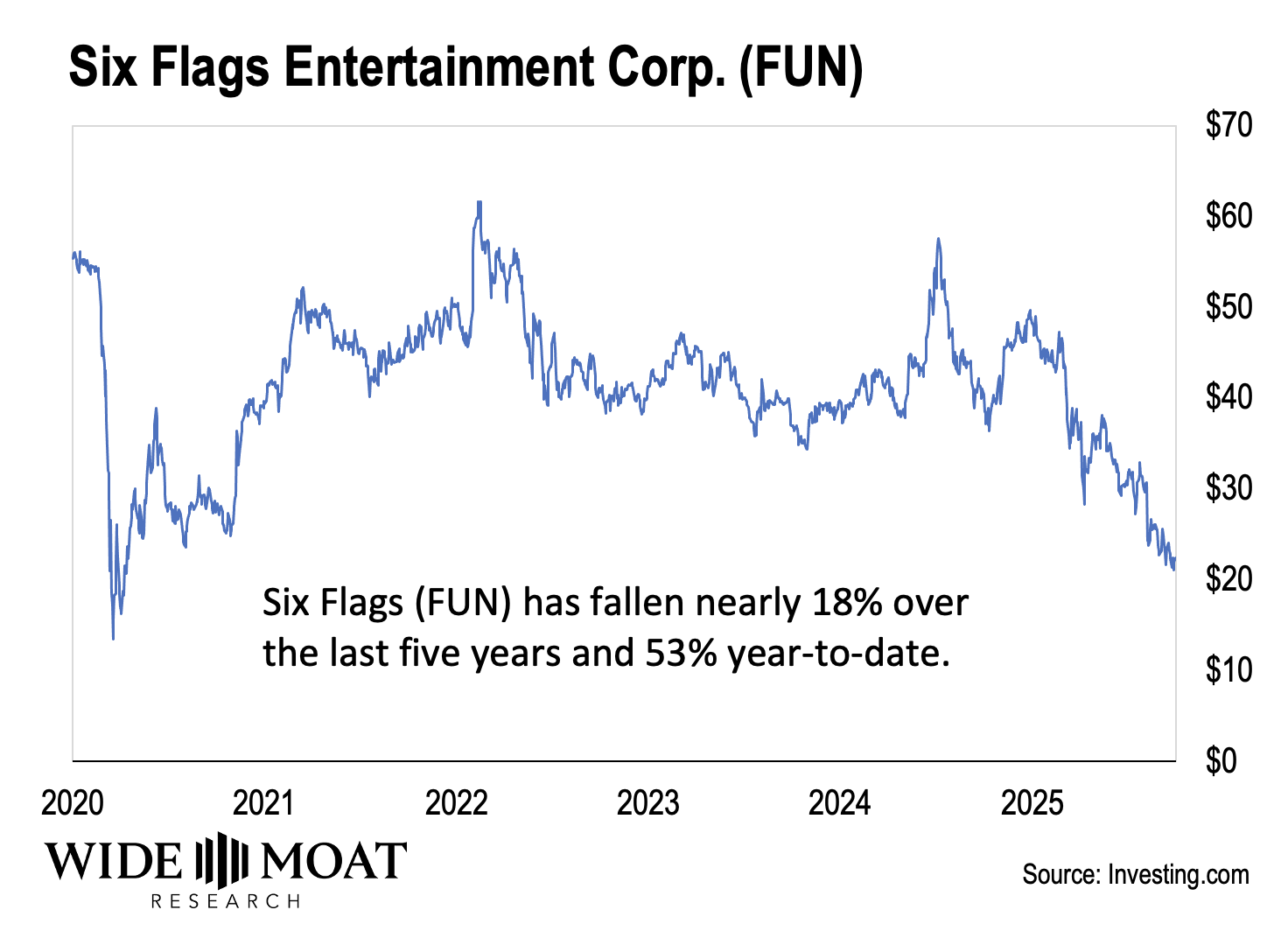

Even so, shares are down 18% over the past five years and about 53% year to date.

There’s more work to be done to turn this company around. And Litt and I agree that real estate is the key to unlocking value.

However – and this may surprise readers – I don’t think a REIT is the way to go.

A FUN REIT Just Doesn’t Seem Smart

Six Flags owns plenty of real estate, with 27 amusement parks and 15 gated water parks.

Two of these properties are in Mexico and two in Canada. The other 38 are located in some of the U.S.’s biggest metro areas, including:

-

New York City

-

Los Angeles

-

Chicago

-

Washington, D.C.

-

San Francisco

-

Boston

-

Dallas

FUN also owns nine resorts, all of which are worth a pretty penny on their own. Yet, believe it or not, I don’t believe spinning them all off into a REIT is the answer.

Yes, this is the expert on real estate investment trusts speaking. And no, I haven’t changed my stance on how worthwhile REITs can be.

But as “the expert,” I know this business model’s pros and cons very well. That includes the legislation surrounding it.

As I explained in REITs for Dummies, a decade ago, ordinary C corporations could spin off their real estate – tax free – into REITs. And so a whole range of companies did exactly that, shifting their financial responsibilities without costly financial ramification.

It was such a popular tax “loophole” that it caught Uncle Sam’s attention… including how it was becoming more and more likely that businesses as big as McDonald’s (MCD) could go this route.

And that would mean a noticeable dip in IRS revenue.

That’s why, “In late 2015, President Barack Obama signed a law” revoking that right. Now, companies have to pay their “fair share” if they want to pursue such an option.

Not surprisingly, no C corp has spun off its land into a REIT since.

Nonetheless, as Lauren explains, Land & Buildings:

… is calling again for Six Flags to spin out its parks’ real estate into a new real-estate investment trust entity that it thinks would trade at a higher multiple. The idea of separating operations from real estate is sometimes referred to in the investing world as an “opco-propco” split.

Apparently, Litt really, really thinks FUN has devalued itself. And I’m sure he has research to back that evaluation and subsequent solution up.

At the same time, remember what happened to Sears when it spun off its real estate into a REIT – Seritage Growth Properties (SRG) – before Obama’s law went into effect. I wrote last week how:

Sears strikes me as the type of business that “cut its flowers to water its weeds,” to borrow a phrase from Peter Lynch.

It could have tried to reinvent itself. It wouldn’t have been easy, but it also wouldn’t have been the first company to do so. Even Berkshire Hathaway once existed as a New England textile business.

Instead, Sears quit all the wrong things and doubled down on a business model that was in obvious decline.

And while REIT spin-offs have been wildly profitable – shares in Darden Restaurants (DRI) have increased 315% since it spun off its real estate into Four Corners Property Trust (FCPT) – Sears’ attempt didn’t ultimately save it from irrelevancy and eventual insolvency.

It still had to generate consistent profits for its remaining business afterward… which it failed to do.

On a more positive note, to quote Lauren again:

Land & Buildings also believes Six Flags should evaluate an outright sale of its real estate, which it thinks could be worth as much as $6 billion. It sees private-equity firms and other real-estate companies as interested buyers.

And that, I think, is a much better option.

A Sale-Leaseback Is the Catalyst FUN Needs

Since the “real-estate companies” category obviously includes REITs, two particular suitors come to mind right away.

First, there’s S&P 500 constituent VICI Properties (VICI), a net-lease REIT that owns 93 large, experiential properties. Most of these are casinos leased to Caesars Entertainment (CZR), MGM Resorts International (MGM), The Venetian, Penn Entertainment (PENN), and other big-name institutions.

So VICI’s business model is already structured around experiential assets, making it a logical suitor for Six Flags’ assets – especially when you consider how it has a loan portfolio with Great Wolf Lodge worth around $724 million. VICI is also an expert in sale-leaseback deals, making it an even better fit.

Another logical option is Realty Income (O), another member of the S&P 500. This larger net-lease REIT owns over 15,500 properties in all 50 states and within Europe, which it’s busy expanding into.

Realty Income has also begun growing its experiential holdings, such as gaming and data centers. And it’s well-positioned to tackle a monster sale-leaseback deal like Six Flags.

Regardless of who steps up, Six Flags owns some desirable real estate that can be sold and leased back at attractive pricing levels. Based on the latest activist news, I suspect Six Flags is more motivated than ever.

But no matter what happens, I think we’re in the early innings for a new wave of sale-leasebacks to unlock shareholder value on both sides of the deal.

As I shared in an interview in December last year:

[W]hen I look at the net lease sector, more and more I’m comparing it to the banks. That’s because a lot of these businesses are really more like banks disguised as REITs. That’s because they finance just about everything.

So, Realty Income could buy a theme park and lease it back. It could buy an NFL football stadium and lease it back. It’s just a form of financing. And it’s something a lot of people don’t understand.

As I said, VICI and Realty Income are the two most obvious suitors. And since we hold both in our Wide Moat Letter portfolio, I’ll be following this story going forward.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|