I named my company Wide Moat Research because I’m a big believer in not just growing wealth but protecting it.

Too often, analysts and investors alike are focused on growth alone. They might not even realize it, but that doesn’t mean the damage doesn’t happen.

It certainly happened to me. Twice.

I’ll try to keep this brief for you regular readers who already know my story. But I thought I was knocking it out of the park as a younger man, developing commercial real estate sites.

I carefully researched every property I ever purchased, and my tenants were quality companies I made sure to know well. I thought I was automatically safe that way.

Problem was, I was so focused on growth that I didn’t make my business partner accountable – a mistake that ultimately led to unethical management, which I wrote about recently.

He was rich, and I wanted to get rich. And so, I attached my money to him.

The results were disastrous.

I also didn’t diversify properly. Back before the housing market crash, real estate was the place to make fast money. And so, every bit of money I made went toward either reinvesting in real estate or purchasing high-priced luxuries.

I didn’t have any savings to speak of other than equity in my real estate partnerships… which is why I was devastated once again after 2008.

That all taught me the value of looking for wide-moat investments: companies that know how to diversify against uncertainty. Plus, they save money during good times so they can safely ride out the bad.

Put more simply, a wide-moat investment is the type of asset you can hold for years or decades… and sleep well at night.

Those are the kinds of assets I want in my portfolio. And if you’re a subscriber, I assume you do as well. So, I’m going to make a point to highlight some wide-moat investments from time to time.

Today, we’ll look at Prologis (PLD) – an industrial real estate investment trust (“REIT”).

It Pays to Know About Prologis

Prologis owns warehouses.

Lots of them.

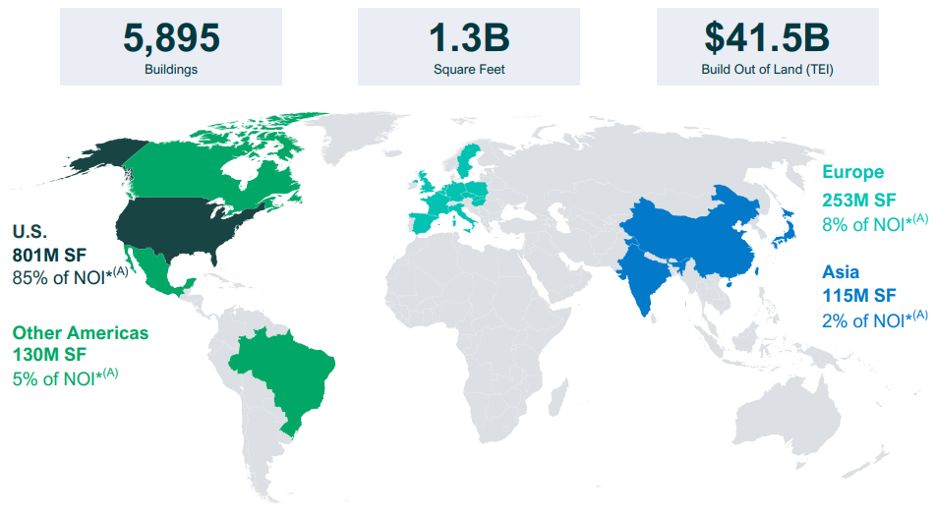

All told, Prologis owns over 6,000 buildings, which take up about 1.2 billion square feet of real estate in 19 countries. It serves more than 6,500 customers. And – as it accurately boasts on its website – approximately “3% of the world’s GDP flows through [its] distribution centers annually.”

When it comes to a “wide moat” real estate portfolio, it doesn’t get much better than that. You can see the company’s reach for yourself below.

Source: Prologis, Q2 2025 Supplemental

Yet Prologis isn’t content to just dominate warehouses. It began investing in data centers back in 1999.

At first, this consisted of converting its own warehouses – small efforts here and there that served it well as e-commerce began to expand. That measured approach also meant it avoided much of the headaches when the dot-com bubble burst in 2000.

But then it began to invest more heavily into data centers once the pandemic hit. In fact, it began building entirely new facilities, oftentimes through partnerships.

As of December of 2024, Chris Curtis, head of data centers for Prologis said the company had “delivered 29 projects dating back to 1999.”

That makes it still a relatively small part of the business, but it will grow. Last year, Prologis’ CEO said:

[Data centers] are a very small portion of the business today. It’s less than one percent. But it’s likely to be ten to fifteen percent of the business going forward, in terms of impact.

Moreover, Prologis boasts 15,000 acres of “development-ready land,” according to its website. Add that to its $207 billion in assets under management, and it’s clear Prologis has a place in the data center race.

Now, I do need to state that I’m not always thrilled with REITs that diversify outside their main property bases. Oftentimes, this is a recipe for underperformance, as they stop operating within their circles of competence.

But Prologis’ has taken a slow and steady approach to its data center buildup. The company also tends to monetize (sell) these assets and recycle the proceeds back into its core business. All this has allowed it to master the sector without undue risk – an impressive feat.

Where Prologis Is Today

Prologis has experienced its fair share of market dips and economic downturns. This includes the housing market crash 17 years ago.

2020, too, of course. Though Prologis ended up benefitting from the ensuing e-commerce wave.

Then interest rates began to rise, and REITs in general fell out of favor. And fears over Trump’s tariffs have more recently weighed on industrial landlords especially.

Yet Prologis just keeps proving its resiliency, even in this past hectic quarter.

Despite extremely pessimistic predictions, core funds from operations – the REIT equivalent of earnings – came in at $1.46 per share. Occupancy stood at a solid 95.1%. And same-store growth was 4.8%.

Now, fundamentals did moderate. For instance, cash same-store net operating income growth decelerated 130 basis points quarter over quarter to 4.9%. And since Prologis’ full-year forecast currently stands at 4.25% to 4.75%… the next two quarters will likely feature more slides still.

Management also reduced its net absorption forecast for the year by about 50%… implying that demand will be flat or even lower these past six months. Similarly, I suspect market rent growth won’t move much either.

However, a stagnant quarter or two isn’t the end of the world for a REIT like Prologis.

Keep in mind that Prologis began over $900 million in new development starts over the last quarter. Nearly 65% of that was build-to-suit deals across seven projects in both the U.S. and Europe.

Moreover, these starts totaled $1.1 billion in the first half of 2025, the REIT’s largest amount ever.

As Christopher N. Caton, senior vice president and global head of research explained, “These are Fortune 500 customers that can see through the short-term noise. And they’re making long-term decisions.”

Significant Possibilities for Prologis

In a recent interview with Fox Business’ Mornings With Maria, Treasury Department Secretary Scott Bessent gave four reasons he’s optimistic about the economy:

-

Trump’s tariffs are bringing manufacturing back to the U.S.

-

The full expensing clause in the One Big Beautiful Bill makes it easier to do so.

-

The same goes for deregulation.

-

“We’re in the middle of this incredible AI boom” that’s spurring growth left and right.

“America is building things again,” Bessent concluded. “This is how a country gets rich and stays rich.”

It’s also how warehouse and data-center landlords like Prologis continue to thrive.

The REIT is sitting on an absolute war chest of land, with over 14,000 acres across its portfolio. That’s enormously important in the rising build-to-suit economy I mentioned up above.

As Senior Vice President Caton pointed out, “We’re finding our land that we control is a differentiator for us.”

Prologis is perfectly positioned to become a long-term benefactor of the American building boom. Yet you wouldn’t know that looking at its share price.

As shown below, shares are trading at a 24.9 times price to adjusted funds from operations ratio. That’s below its normal multiple of 27.3 times.

Source: FAST Graphs

The REIT offers a 3.7% dividend yield, and analysts expect Prologis itself to grow 8% in 2026 and 10% in 2027. Even with no multiple expansion at all, shares could still return more than 10% annually.

With the kinds of catalysts we’re seeing, our forecast is much more aggressive. Wide Moat Research expects 15% to 20% annualized total returns on Prologis.

Source: FAST Graphs

That’s why I see Prologis’ depleted share price today as a wide-open opportunity. I just don’t see how this wide-moat logistics landlord is going to stay down for long.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. For more wide-moat picks, tune into our weekly YouTube evaluation, The Wide Moat Show.

|