The August jobs report was released on Friday. The numbers… weren’t great.

According to the Bureau of Labor Statistics, the U.S. only added 22,000 jobs in August. Economists had expected 75,000 jobs added.

Also, 7.384 million people are now unemployed in the United States. June’s figures were revised down to negative 13,000.

That’s right. Hiring actually contracted three months ago, all things considered. The last time that happened in America was December 2020.

So, who is to “blame”?

All this happened on Trump’s watch with his extremely unorthodox handling of global trade.

Then again, it has also all been on Powell’s watch with his abject refusal to lower rates after Trump took office.

Then again, it also all happened as business leaders brag about their AI-fueled cost-cutting (i.e., job-cutting) measures. Like Microsoft (MSFT), which said it’s saving hundreds of millions of dollars by using AI instead of humans for support functions. Or PayPay’s (PYPL) implementation of its customer service bot, PayPal Assistant.

Then again (again), most of the jobs gains the U.S. saw last year actually went to foreign-born workers. So, perhaps the downbeat jobs numbers are the result of new immigration policies?

“Everyone” can debate the information until they’re blue in the face. But one thing is crystal clear: Interest rates have to come down.

‘Shifting Balance of Risk’

When Powell spoke after the Fed’s Jackson Hole meeting last month, he spoke about a “shifting balance of risk.” He was referring to the labor market. And judging by the numbers on Friday, yes, the balance of risk is certainly shifting.

Powell opened the door for a September rate cut. But he also made sure to stress that it wasn’t a certainty. After Friday’s news though, there’s no gray left to the question. It’s obvious what needs to happen.

Fed fund futures now show unanimous expectations for a rate cut this month. Twelve percent of traders even think we’ll see a 50 basis-point drop instead of 25.

However, even if that minority is wrong, I imagine we’ll see more cuts in the final quarter of the year – all of which will benefit businesses. Especially real estate investment trusts, or REITs.

I know I argued this just a month ago after the initial July jobs report came out. I don’t mean to sound like a broken record. But it’s worth repeating. Here’s what I wrote on August 5:

I’ve personally seen how the right REITs can transform a portfolio over time. These mandatory dividend payers are governed by strict rules that tend to keep them more conservatively managed.

In exchange for an income tax exemption, REITs pay out at least 90% of their otherwise taxable income annually to shareholders. This setup tends to mean that they pay higher dividends than other companies, not to mention more stable ones, too.

Dividends are well and good. But when it comes to share price appreciation, REITs haven’t done much lately. In fact, they haven’t done that well since the Fed began raising rates in early 2022. And while REIT enthusiasts like me certainly hoped this year would mark their big share price return…

That just hasn’t happened yet.

That’s because most investors believe REITs can’t perform well in a high-interest-rate environment. These corporate landlords borrow significantly whenever they want to make an acquisition, so people automatically assume they struggle whenever the cost of that borrowing rises.

Also, REITs tend to be treated as bond adjacent. So, rates go up, share prices for REITs go down – that’s the market’s conventional wisdom.

No amount of contrary data – such as the strong balance sheets, increasing dividends, and growing property counts REITs have boasted for years – can make them think otherwise.

Fortunately for us, we can use that misconception in our favor today, by buying up quality REIT shares at low, low prices – right ahead of the next rate cutting cycle.

Even Stagflation Shouldn’t Hamper REITs’ Resiliency

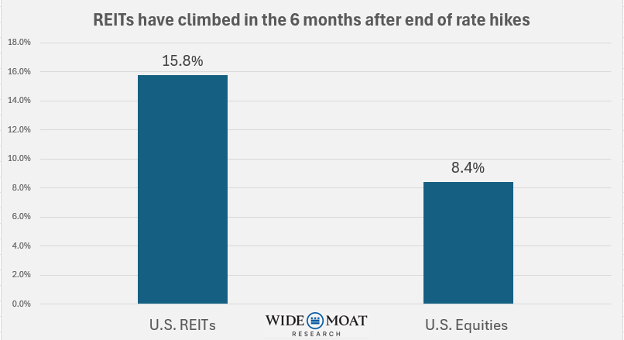

REITs have performed remarkably well after most rate-hiking cycles end. Between 1994 and 2019, they’ve returned 15.8% in the first six months after the Fed stops raising rates.

The larger equities category, meanwhile, has only risen 8.4%.

Source: Cohen & Steers

I know the last 26-month period hasn’t followed suit. But we’ve also been dealing with a slew of exceptional factors:

-

The unprecedented government spending of the COVID-19 era

-

A Federal Reserve chair desperate not to repeat his embarrassing mistakes (“transitory inflation,” anyone?)

-

Trump’s game-changing tariffs

However, I think those factors will lose their potency once interest rates really begin to fall. REITs will find it easier to finance their debt, both old and new, allowing them to grow faster and smarter – even more so than they have been for the past three and a half years.

The stigma they’ve been living under should decline as well.

I even expect this to be true if we find out this week that we’ve officially entered into a period of stagflation. We’ll have a better idea of this on Thursday, after the Consumer Price Index (“CPI”) results are published.

After hitting four-year lows in April, economists expect headline CPI to have increased four months in a row – this time from 2.7% in July to 2.9% in August. Core CPI, meanwhile, will probably remain at 3.1%.

But even if that is true, the pressure will be on Powell and his governors to test out lower rates. They’ve already allowed too much damage to be done by waiting this long.

Besides, REITs can actually do quite well under stagflation since they offer protection against both sides of the problem. Their contractual rent increases tend to take inflationary factors into consideration. And those contracts are often for years or even decades on end, meaning they still get paid unless their tenants go bankrupt.

One REIT Sector I Have a Close Eye On

Essentially, REITs look good regardless of how the economic cards fall. They’re already doing just fine under current interest rate conditions…

They’ll almost certainly do even better once the Fed starts cutting. And they’re set to hold their own even if inflation continues to spike.

And of all the sectors and subsectors we cover here at Wide Moat Research, there’s one in particular I have my eye on – health care. The reason why was found in the same jobs report on Friday.

Here’s how The Wall Street Journal covered it this morning:

So far in 2025, the economy has added an average of about 74,000 private-sector jobs a month, according to the Labor Department, a step down from last year’s average gain of about 130,000 jobs. Take away the roughly 64,000 jobs that health services have been adding each month, though, and the remainder of the private sector has been contributing only about 9,400 jobs a month.

Health care has been adding the lion’s share of new jobs this year. And that’s why I’ll be covering health care REITs in the next few days. And Nick Ward and I are set to talk about net-lease REITs on Thursday for our next YouTube episode (called “Nothing But Net”).

There’s a whole world of high-quality, low-cost corporate landlords to consider as September plays out. And I, for one, want to consider as many as I possibly can.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|