Enjoy the relative calm right now.

Because, in a few quarters, we’ll be dealing with crashing markets, mass unemployment, and perhaps even a mortgage/credit crisis to boot.

Or, at least, that’s what the market seemed to be thinking yesterday…

On Monday, the major indexes fell in apparent response to (of all things) a post on Substack. The now-viral report from Citrini Research presents a scenario from the perspective of a market observer two years in the future. And it wasn’t pretty.

From the post:

The unemployment rate printed 10.2% this morning, a 0.3% upside surprise. The market sold off 2% on the number, bringing the cumulative drawdown in the S&P to 38% from its October 2026 highs.

[…]

AI capabilities improved, companies needed fewer workers, white collar layoffs increased, displaced workers spent less, margin pressure pushed firms to invest more in AI, AI capabilities improved…

It was a negative feedback loop with no natural brake. The human intelligence displacement spiral. White-collar workers saw their earnings power (and, rationally, their spending) structurally impaired. Their incomes were the bedrock of the $13 trillion mortgage market – forcing underwriters to reassess whether prime mortgages are still money good.

It goes on like that…

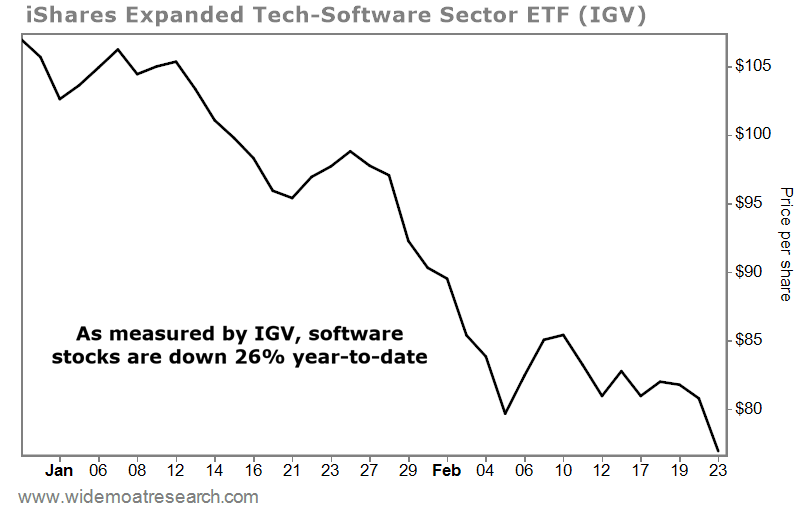

In that worst-case scenario, software names were the first casualties. Perhaps that’s why the iShares Expanded Tech-Software Fund (IGV) fell as much as 5% yesterday. Individual names like Datadog (DDOG) and Zscaler (ZS) each fell about 10%.

As readers know, this “SaaS-pocolypse” has been going on for some time. In fact, the software sector has undergone the largest non-recessionary 12-month drawdown in over 30 years, losing around $1.3 trillion in market value. Since just January, the IGV is down about 26%.

As I explained in a recent Wide Moat Daily article:

… the reason behind [Tuesday’s] collapse was [AI] – specifically, Anthropic’s newest round of AI tools from its Claude Cowork, a desktop app that can read, create, and edit computer files. It’s apparently now branching out into sales, finance, legal tasks, and customer support.

Put another way, the AI seems capable of handling tasks typically accomplished by enterprise software.

As a result, once-vaunted software stocks are dirt-cheap relative to their historic multiples.

But should they be?

Mr. Market seems to be in a mood for considering hypotheticals.

So, here’s a hypothetical: What if the world does not end?

Being the value investor that I am, I couldn’t help digging through the muck to evaluate these fallen angels.

The stocks are under pressure. But Software as a Service (“SaaS”) revenue is sticky… many of these companies have 95% retention rates with multiyear contracts… and they often provide mission-critical software.

And if you’re looking for gems among the rubble, here are two names I’m keeping an eye on.

Salesforce and AI Go Hand in Hand

Salesforce (CRM), one of the original SaaS giants, helps businesses manage customers, sales, marketing, customer service, and data. Founded in 1999, it’s best known for pioneering customer relationship management (“CRM”) software delivered over the Internet.

This creation helps companies track leads, customers, sales, e-mails, phone calls, support tickets, and contracts. Instead of having to deal with messy, time-consuming spreadsheets, Salesforce’s software maintains all that information in one centralized system.

It essentially becomes the “system of record” for customer data. So, once a company switches over to it, it’s very unlikely to try out something else – even AI – when doing so could complicate or even ruin its accounts.

Critics will argue that we’re still in the beginning phases of AI breakthroughs. And they’re right. I just think they’re wrong in believing that automatically means this SaaS powerhouse is kaput.

You see, Salesforce is already layering AI on top of its massive customer dataset of over 150,000 customers with millions of users. This allows it to generate better sales forecasts, automate lead scoring, predict churn models, automate follow-ups, and handle support agents.

In which case, it’s becoming even more critical to keep, not less so.

Salesforce has begun breaking down its annualized revenue run rate that it generates from new AI products. We learned in December, for instance, that its Agentforce platform passed half a billion dollars in the third quarter of 2025.

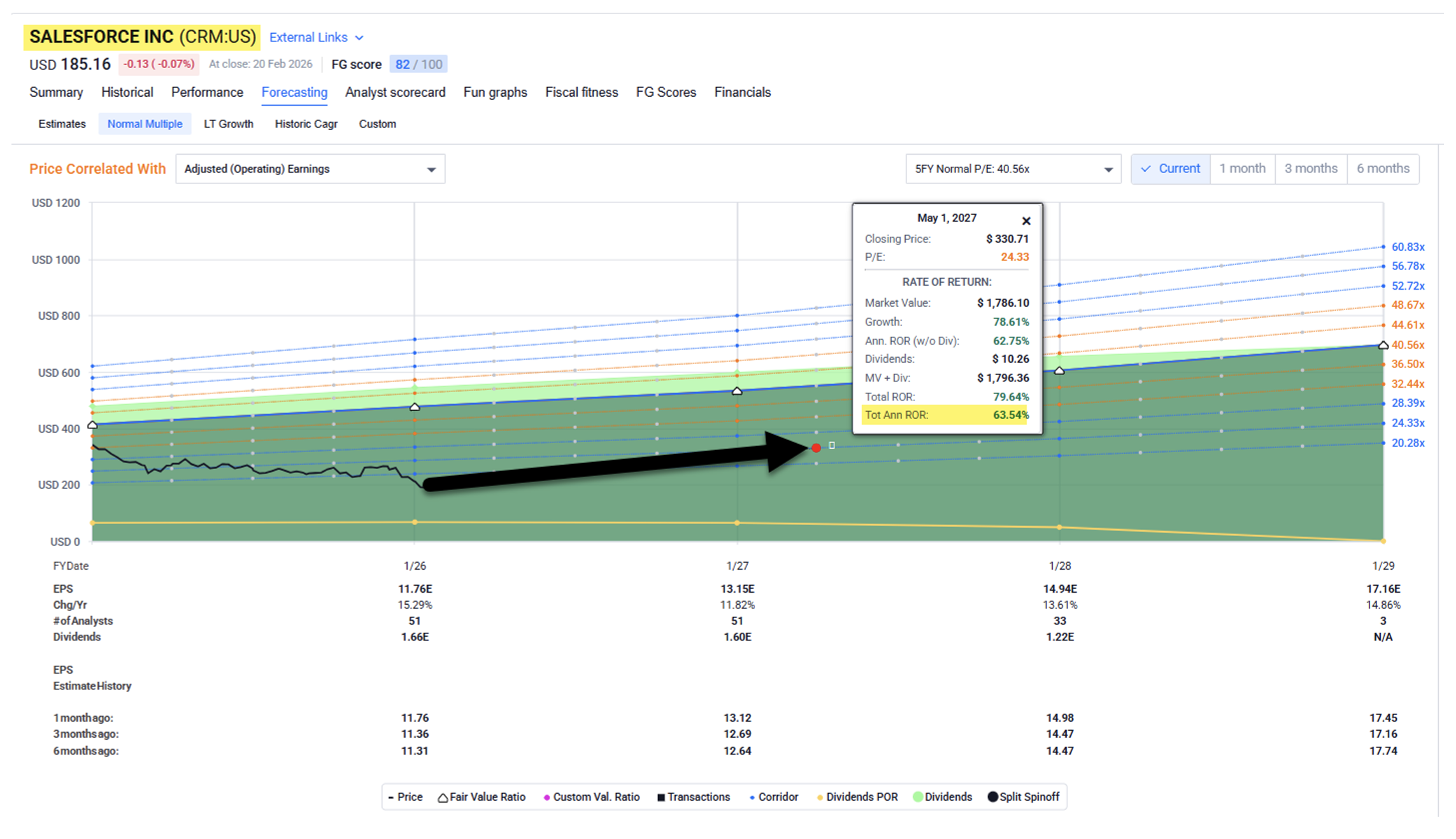

The company will announce earnings tomorrow, so we’ll be looking for updated numbers there. But for now, shares are trading at $185.16 with 15.6 times forward earnings per share (“EPS”).

Over the past five years, they’ve traded at an average of 40 times. So if Salesforce can begin to show increased AI adoption, I could see it returning 50% or more over the next 12 months.

Again, we’ll get to see the updated numbers very soon – and how investors receive them. But I expect they’ll show promise that I wouldn’t mind a piece of.

Source: FAST Graphs

HubSpot

HubSpot (HUBS) is a cloud-based CRM and marketing software company. Unlike Salesforce, it focuses primarily on small- and mid-sized businesses, growing companies, and startups.

HubSpot began in 2006 with a focus on inbound marketing, helping clients attract customers through content, search engine optimization (“SEO”), and e-mail rather than cold sales. Over time, it evolved into a full CRM platform and now offers an integrated suite of tools called “Hubs”:

- Marketing Hub – e-mail marketing, automation, SEO, ads

- Sales Hub – CRM, deal tracking, outreach tools

- Service Hub – customer support

- CMS Hub – website building

- Operations Hub – data sync and automation

At its core, HubSpot is a CRM platform — but with strong marketing DNA.

The company built its product to be easy to use and fast to deploy. So, you can sign up and get started quickly without hiring an army of integrators. That’s one of the big reasons why it has done so well even with Salesforce in the game.

Source: HubSpot

HubSpot already reported fourth-quarter 2025 results earlier this month. Revenue grew 18.2% year over year, and full-year 2025 revenue grew 18.2% to $3.1 billion. Plus, it delivered another quarter of standout operating profit growth with an operating margin of 22.6% and 18.6% for the full year.

The company also added more than 40,000 new customers in 2025 so that it now has more than 288,000 globally. As CEO Yamini Rangan explained on the earnings call:

… we are focused on making AI work for growth companies. While there is no shortage of AI solutions in the market, there is a real gap between generating AI output and driving growth outcomes. Closing that gap is what will unlock broad AI adoption, and that requires content [and] having the right information at the right time with the judgment to know what to do with it. And that’s where HubSpot has a clear advantage.

HubSpot has guided $3.69 billion to $3.70 billion in revenue, or 18% year-over-year growth, for 2026. Pro forma operating margins are expected to increase one point to 20%, and it predicts $740 million in free cash flow.

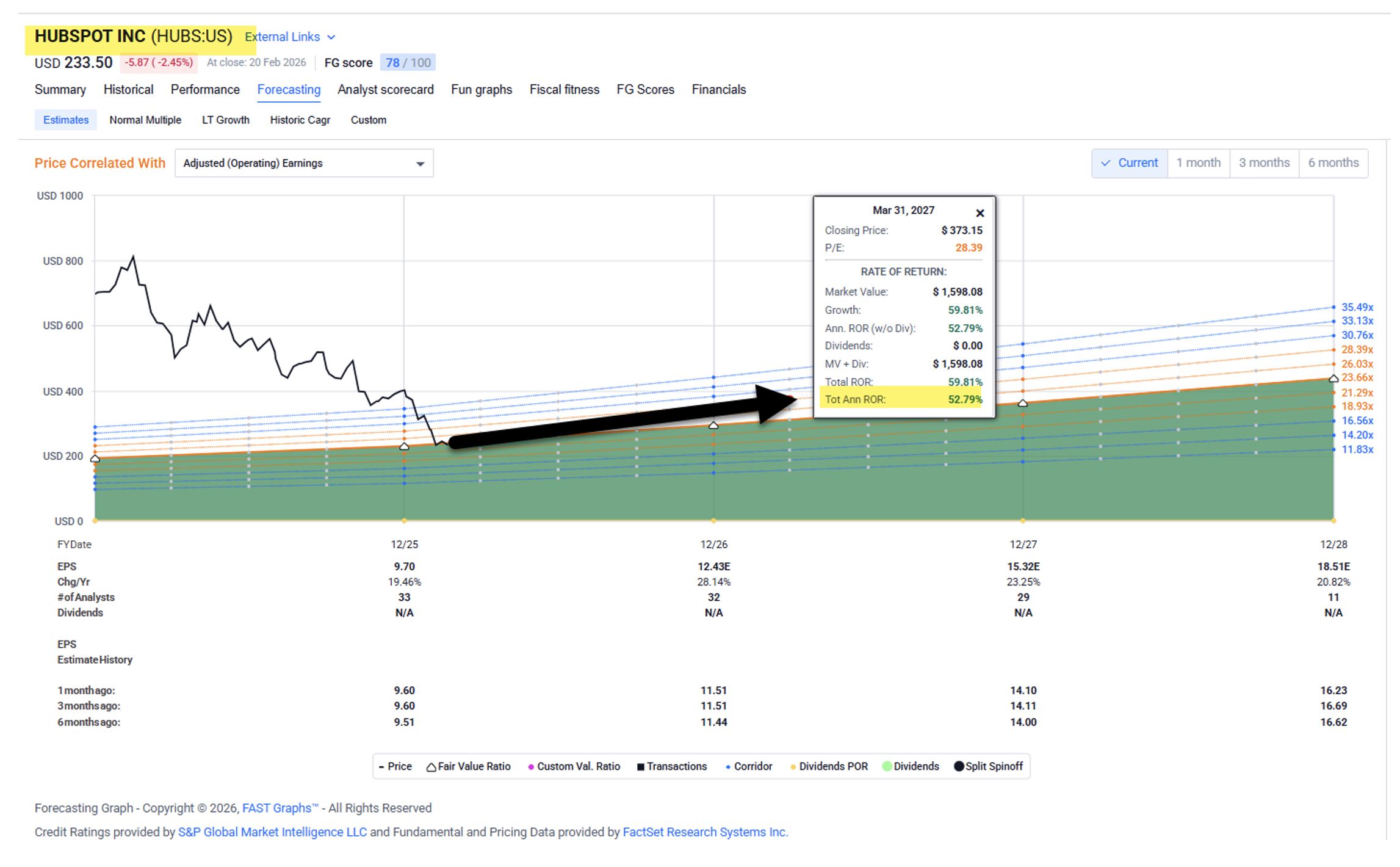

Shares are now trading at $233.50, with a price-to-earnings (P/E) of 23.2 times – significantly below their average EPS multiple of 82 times. Analysts expect growth of 28% this year, 23% in 2027, and 21% in 2028.

Yet thanks to AI-inspired panic, HubSpot offers value investors a significant opportunity… with shares potentially returning at least 50% over the next 12 months.

Source: FAST Graphs

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Tune into the Wide Moat Show on Thursday, where Nick Ward and I discuss the “Fallen-Angel Software Sell-off” further.