In yesterday’s Wide Moat Daily, I highlighted the oversupply of biotech real estate triggered by “the COVID-19 era.”

What started out “like a gold rush” for life-science properties turned into a supply glut.

The sector’s real estate pipeline peaked in the second quarter of 2023, when activity totaled 17% of existing inventory. But that oversupply – now coupled with slower capital flows from venture capital firms and the government shutdown – has resulted in reduced profitability for life-science landlords.

Developer interest has crashed in the meantime, with pipeline activity now sitting at just 3% of existing inventory. And investment interest is even worse.

Shares of real estate investment trust (“REIT”) Alexandria Real Estate (ARE), for instance, have fallen 25% since its earnings report last week. With that fall, the stock is down about 75% from its 2021 peak.

As a developer, I’ve seen this more times than I can count. A property sector gets “hot,” there is massive overbuilding, and the supply glut becomes a drag on companies in that sector. That was the story of life-sciences properties in the first half of the 2020s.

Could something similar happen to data centers in the years ahead?

That’s what we’ll look at today…

Dark Fiber

During the late 1990s and early 2000s, telecom companies spent billions building out fiber networks. The thinking was that data traffic would continue to surge higher and that the fiber infrastructure would become profitable… eventually.

But after the dot-com crash, growth in data traffic actually slowed. And as much as 90% to 95% of that fiber went unused. It was “dark,” in other words.

People are worried that something similar could happen with data centers.

Basically, the fear is that data-center construction will get ahead of itself. Too much supply will meet slowing demand growth… and companies in this sector will suffer.

My take: If that’s going to happen, it won’t be any time soon. Just look at the numbers.

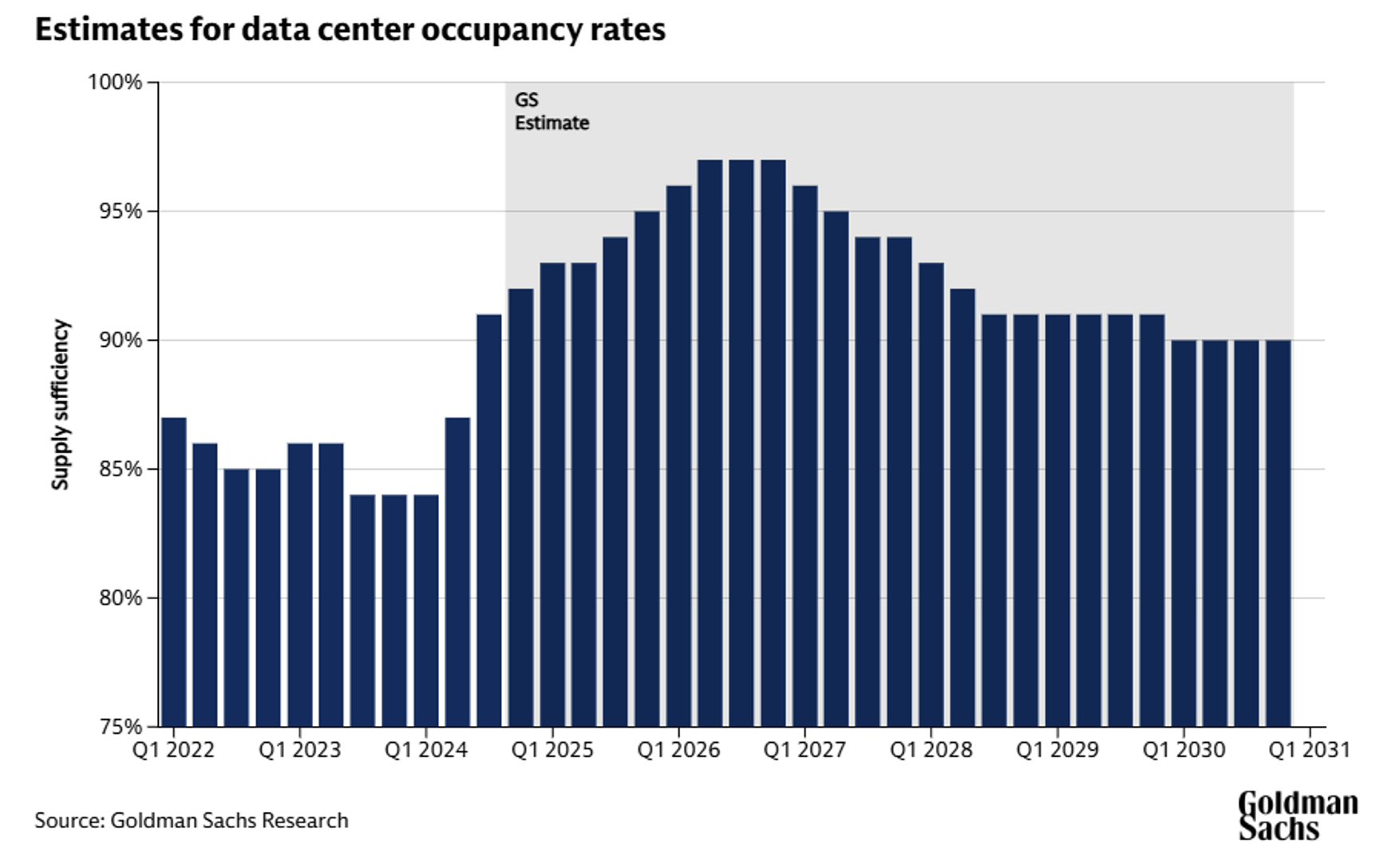

According to Goldman Sachs Research, global power demand from data centers will increase 50% between 2023 and 2027 – and by as much as 165% by the end of the decade.

On the supply side, hyperscale cloud companies like Meta Platforms (META), IBM (IBM), Alphabet (GOOG), and Apple (AAPL), and data-center operators like Digital Realty and Equinix (EQIX), are deploying large amounts of capital to build new high-capacity data centers.

Taken together, Goldman forecasts that the balance of data-center supply and demand will tighten in the coming years. Occupancy is projected to increase from around 85% in 2023 to 95% or more in late 2026.

That will likely start to moderate in 2027 as more data centers come online and AI-driven demand growth starts to slow.

The research estimates current global data-center power usage to be around 55 gigawatts (“GW”), comprised of:

-

Cloud computing workloads (54%)

-

Traditional workloads for typical business functions, such as e-mail or storage (32%)

-

Artificial intelligence (14%)

But by 2027, Goldman forecasts that power demand will reach 84 GW… with AI growing to 27% of the overall market, cloud computing dropping to 50%, and traditional workloads falling to 23%.

This isn’t an isolated opinion either. As commercial real estate and property investment firm JLL recently stated:

Billions of dollars have been invested in AI over the last couple of years, which is driving demand for more powerful and efficient data center infrastructure. As a result, global data center construction currently stands at record levels. All signals suggest that AI demand will continue to build momentum in 2025.

It adds that:

Across the hyperscale and colocation segments, an estimated 10 GW is projected to break ground globally in 2025. Separately, 7 GW will likely reach completion. This equates to roughly $170 billion in asset value that will need to secure either development or permanent financing in 2025.”

Bottom line: It’s entirely possible that data-center supply will get ahead of demand. Like I said at the top, I’ve seen that story play out in various property sectors more times than I can count.

But it won’t happen this year. It won’t happen next year. And I seriously doubt we’ll see it in 2027.

To me, the buildouts we’re seeing in data-center capacity are a response to very real, very strong demand forces.

And that’s why data-center REITs are likely to have several good years ahead of them.

And one of my favorites is…

The Data-Center Dynamo

Based in Texas, Digital Realty (DLR) has an enterprise value of around $80 billion. Its 300-plus data centers across more than 50 leading metros serve over 5,000 customers… so far.

This gives it a distinctive edge over the competition, as do the deep relationships it fosters with both utilities and local governments. And its proven development track record hardly hurts either.

On the company’s latest earnings call, CEO Andy Power explained that, “With each passing week, we continue to see massive investment announcements and partnerships aimed at scaling the infrastructure necessary to support the world’s most powerful AI training models.”

Keep in mind that Digital Realty has a massive $6.4 billion development pipeline (at cost). So, it automatically stands to benefit from AI’s multiyear acceleration, including through stronger renewal spreads, stronger development yields, and continued bookings strength.

Given the unprecedented growth in data-center space, Digital Realty plans to expand outside of its core U.S. markets into areas with remote campuses to support a single-use case or customer.

And all the while, it continues to maintain conservative financing to support its $10 billion total-value land portfolio. The REIT ended its last quarter with 4.9 times net debt to adjusted earnings before interest, taxes, depreciation, and amortization. It also boasted ample liquidity of around $7 billion to invest in new opportunities.

Digital Realty then went a step further still by issuing equity of $500 million and selling off around $120 million in non-core assets. So, in short, it’s well-placed to handle what happens from here.

More Impressive Digital Realty Details

Digital Realty’s scale and balance sheet strength have translated into best-in-class earnings and an increase in full-year guidance.

In the third quarter of 2025, it signed about 50 megawatts worth of new leases – over 50% of which were AI-related. This will generate around $160 million in annualized generally accepted accounting principles rent.

Meanwhile, DLR’s cash re-leasing spreads and same-store cash net operating income growth both improved 50 basis points at the midpoint, which are now 5.75% to 6.25% and 4.25% to 4.75%, respectively.

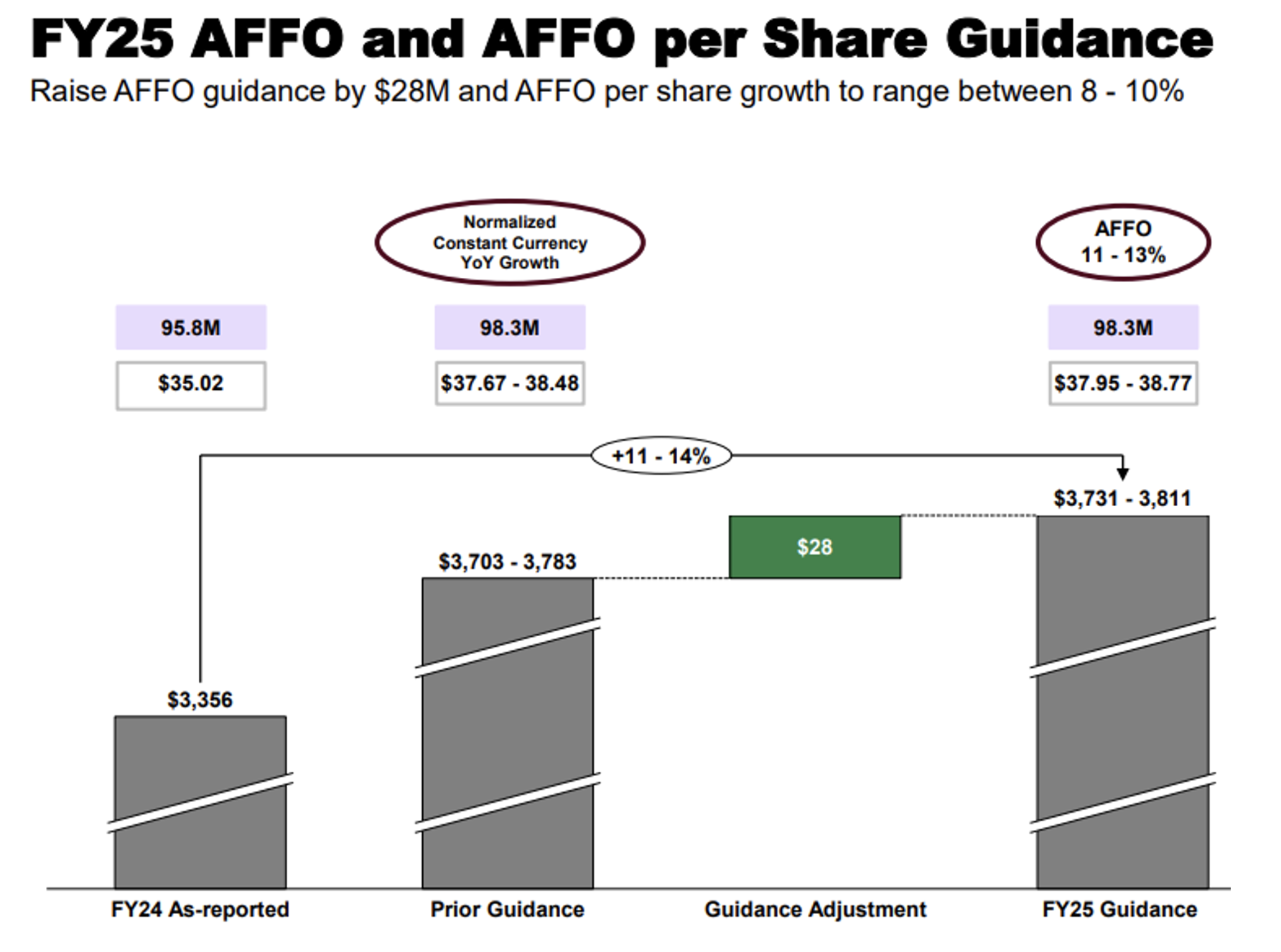

We also need to consider its core funds from operations (“FFO”) per share, which were $1.89 and ahead of consensus. Digital Realty raised its full-year FFO per share by $0.15 at the midpoint to $7.35 per share, which was also better than predicted.

Plus, it raised its adjusted FFO ("AFFO") guidance by $28 million and AFFO per share growth to 8% to 10%.

Source: Digital Realty

Digital Realty is now trading at 26 times price to AFFO, above its normal multiple of 22.3 times. Its dividend yield is 2.8%.

Shares aren’t cheap. But a REIT with fundamentals like these rarely is. And given everything I’ve just shared, I remain bullish on DLR.

Data centers may very well have their “dark fiber” moment… eventually.

But I don’t think it will happen anytime soon. And in the meantime, I don’t think we’ve come close to seeing what quality REITs like DLR can offer.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|