There are market moments when specific share prices make no sense. And we’re looking at one of those moments now.

Imagine playing Monopoly, only to find that Boardwalk is marked down by 30% as you near Go. But it’s not because there is something wrong with the property itself… It’s because the rules have changed.

That’s essentially what is happening today in a corner of the real estate market.

Specifically in single-family rental (“SFR”) real estate investment trusts (“REITs”).

I’m looking at Invitation Homes (INVH) and American Homes 4 Rent (AMH). As two of the largest institutional landlords in the U.S., they own about 140,000 SFR homes combined across high-growth Sun Belt markets.

That’s made them a tidy sum of money in past years, allowing them to reward their investors in return. In 2026, however, their stocks have fallen so far that the market is effectively valuing their $400,000 homes at closer to $280,000.

The last time the median U.S. home sold for that price was in 2014.

We can thank Washington, D.C. for this shift.

In January, President Donald Trump took to Truth Social to denounce corporate SFR landlords, calling them out for making the American housing dream untenable.

As I detailed shortly after, that’s his opinion, not mine. But it looks like Congress is siding with him as it debates the 21st Century Renewing Opportunity in the American Dream (“ROAD”) to Housing Act.

That piece of legislation, which could pass in the next month or two, will almost certainly complicate SFR REIT operations.

So yes, some of the decline makes sense.

But the magnitude of the sell-off doesn’t.

What we’re seeing now, I believe, is an intense overreaction – one that opens up a buying opportunity I can’t ignore.

The Case Against SFR REITs Is Clear

In my last article on the subject on March 10, I quoted BMO Capital Markets as saying that:

The latest draft [of the ROAD legislation] would prohibit additional home purchases by investors above the threshold, while grandfathering existing portfolios. However, the revised bill calls for a 7-year disposition requirement on future homes acquired, including built-to-rent [“BTR”], which has a negative surprise.

Forced resales would likely inhibit capital to develop homes given greater uncertainty on exit economics. Homebuilders wouldn’t have the ability to de-risk with BTR to third-party investors/REITs. Also, if REITs aren’t able to grow, it may hinder reinvestment.

Basically, the proposed legislation could limit how these companies grow and force them to sell homes over time.

Duly noted.

I’ll also fully acknowledge how Senator Elizabeth Warren (D-MA) has demanded disclosures from companies like Invitation Homes and American Homes 4 Rent concerning how they make their money.

If she and Donald Trump can agree on something like this, you know it’s bipartisan enough to probably pass.

It’s also popular enough with the American people to pass. After all, they’ve been sidelined from homeownership for years now. And SFR investors with their enormous amounts of money are an easy scapegoat.

Those institutional buyers often make all-cash offers for the homes they want. So their bids are much more likely to succeed against everyday buyers – only for them to turn the properties into long-term rentals that completely remove houses from the residential real estate market.

That opens up a lot of room for public distrust and dislike on the surface. (For a deeper evaluation, read my March 10 article.) And now that Washington has decided this setup must be curbed, it’s reasonable for investors to expect these businesses to suffer.

What’s not reasonable is to declare them all but dead despite how SFR REITs and other institutional investors still feature:

-

Hard assets that include inflation protections

-

Durable demand from a market with limited supply

-

Scaled operations that offer automatic cost advantages

Those basics haven’t changed, and they won’t change even if the ROAD legislation does pass.

Don’t get me wrong: There will almost undoubtedly be changes that SFR REITs will have to adjust to. So I’m not saying their stock prices will bounce right back to their former glory.

What I am saying is that they will very likely recover a nice chunk of that change. And I, for one, want to get in on that profit opportunity.

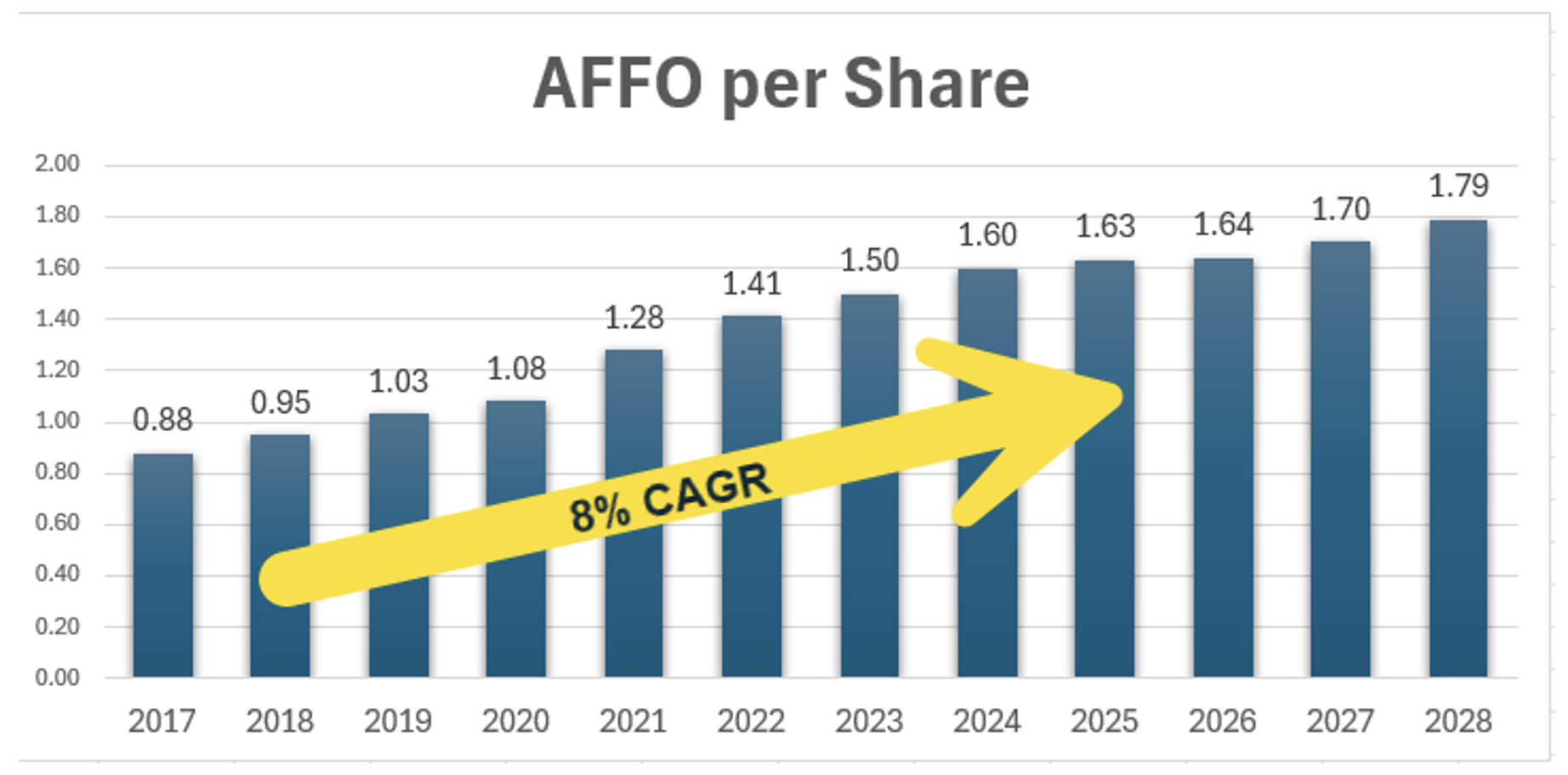

A Closer Look at Invitation Homes

Invitation Homes, the largest U.S. single-family rental REIT, owns 85,000 homes primarily situated across major Sun Belt and Western markets. The company was founded by Blackstone (BX) in 2012 following the Great Financial Crisis and subsequent housing downturn.

In 2017, Blackstone took INVH public. And in 2018, the REIT merged with Starwood Waypoint Homes to further consolidate the institutional housing sector.

As political headwinds developed, INVH began to reposition its capital toward BTR communities in 2023. This move helped it to continue generating notable adjusted funds from operations (“AFFO”).

In fact, earnings grew 8% from 2018 to 2025, while dividend growth has averaged around 15% per year.

Source: Wide Moat Research

That record is obviously in jeopardy now.

INVH benefits from strong occupancy of about 96%. But it must meaningfully accelerate new lease rates to maintain those high renewals.

As seen above, analysts expect modest growth of 1% in 2026. Though that should return to 4% in 2027 and 5% in 2028.

INVH now trades at 15 times compared with its normal multiple of 24 times, and its dividend yield is 4.9% with a 73% payout ratio that reflects policy concerns. I like it today, recognizing that the long‑term fundamentals of single‑family rental housing outweigh short‑term political and rate noise.

If the current scrutiny stabilizes and housing supply remains constrained, it should move back toward fair value.

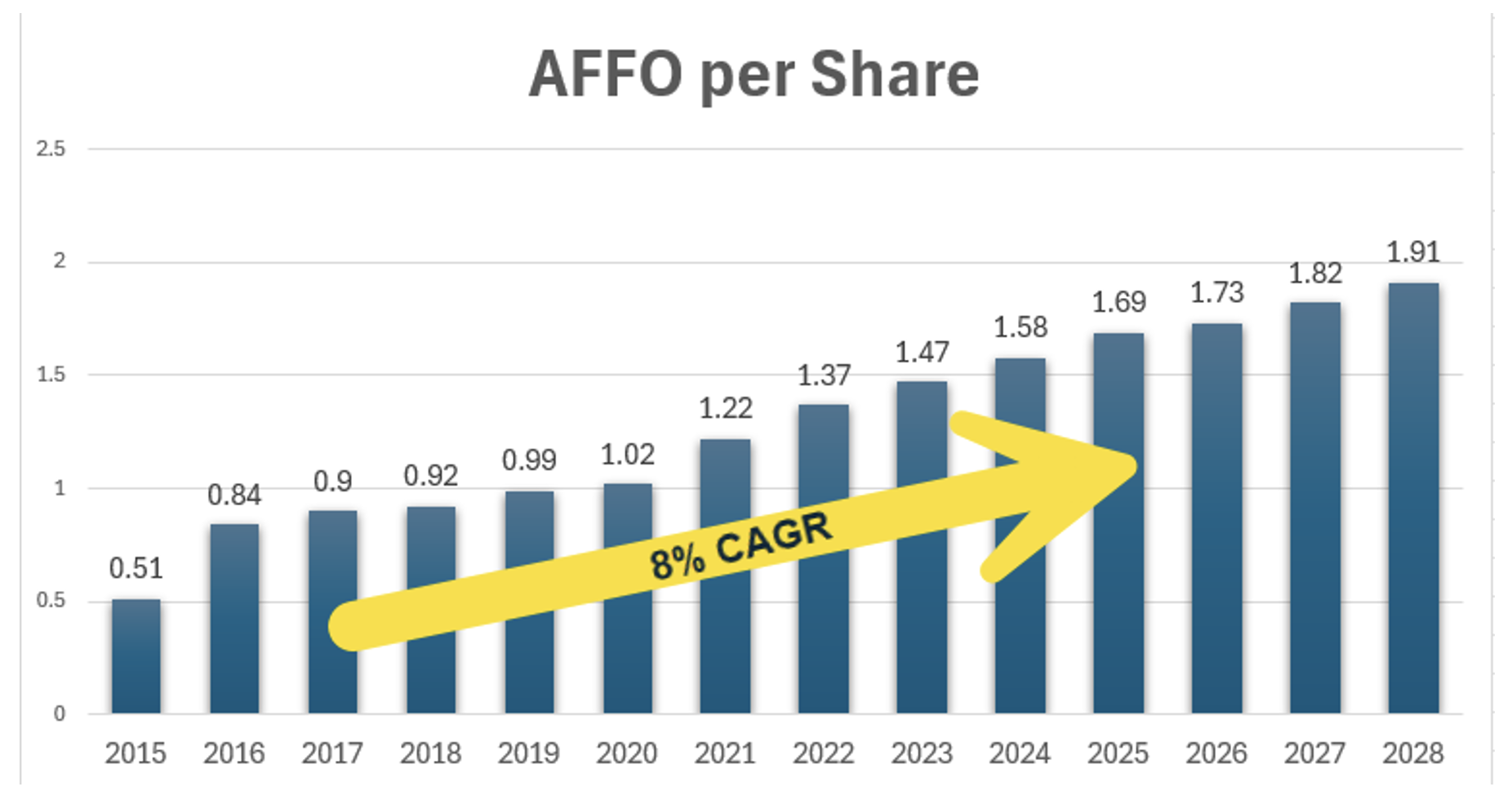

A Closer Look at American Homes 4 Rent

American Homes 4 Rent is an SFR REIT sector pioneer, founded in 2012. Today, the company owns 60,500 homes and holds the second-largest public SFR platform.

Founded by W. Waynes Hughes (founder of Public Storage) and his son Wayne Hughes Jr., AMH went public on August 1, 2013. The company expanded into development in 2014 (forming AMH Development) and effectively created the BTR model.

The REIT generated 8% earnings (AFFO per share) growth from 2017 to 2025, while its dividend averaged around a 25% compound annual growth rate (“CAGR”).

Source: Wide Moat Research

Similar to INVH, AMH will have to grow occupancy to meet its high 95% fiscal-year 2026 guidance. As seen above, analysts are forecasting modest growth of 2% in 2026, returning to 5% in 2027 and 5% in 2028.

AMH now trades at 16.2 times compared with its norm of 25 times. Its dividend yield is 4.8% with a payout ratio of 76%.

This puts it in obvious value territory – especially considering how it posted 7.5% revenue growth in 2025 and offers a mix of income, inflation protection, and long-term demographic demand.

All things considered, though, I still believe in both SFR REITs’ ability to navigate the housing market. As supply remains constrained and interest rates ease, their shared business model should compound cash flows and dividends just fine.

In which case, their share prices will only stay this low for so long.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Tune into The Wide Moat Show on YouTube this week, where my cohost Nick Ward and I will discuss both the single-family rental and cold storage REIT sectors in greater depth.

|