It could have been worse.

The latest inflation numbers came in yesterday, with the Consumer Price Index

(“CPI”) rising 2.7% year over year. That’s a clear uptick from May’s 2.4% and

just a tenth of a point shy from where it was in February, the first full

month President Trump was in office.

Inflation headed in the wrong direction in June. Yet it’s not nearly as bad as

we’ve been told it could be, and it actually fell in line with the estimates

(2.6% to 2.7%).

How many dire predictions have we heard about Trump’s tariffs since he began

implementing them? Many sources expected an abject depression by now, with

average citizens unable to afford even basic necessities.

Instead, Yahoo Finance – hardly a MAGA media outlet – wrote this yesterday:

Economists and consumers alike are on high alert for signs of President

Trump’s sweeping global tariffs showing up at the cash register. While

overall inflation has remained tame through the trade turmoil, price

increases of imported goods suggest “scattered signs” of the impact of

tariffs.

“Scattered signs.” That’s practically praise from a publication that routinely

takes the most critical interpretation possible of Trump’s actions.

All of this matters, of course, because inflation readings will influence the

Federal Reserve’s policy decisions in the month ahead. Lower inflation should

mean rate cutting, all else equal. And that means rate-sensitive assets, like

real estate investment trusts (“REITs”), finally catch a bid.

REITs’ Surprising Strength (Shouldn’t Be So Surprising)

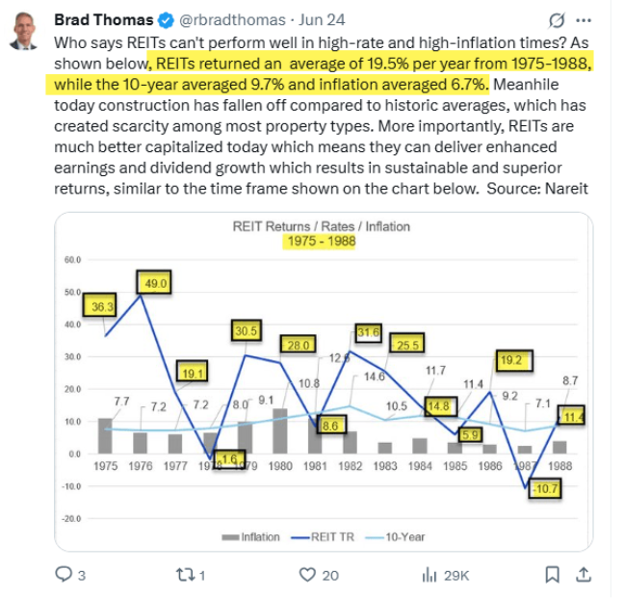

On June 24, I posted this on X:

That’s a lot of information, I know. And it might seem contradictory

considering how we’ve had inflation the last several years… yet REITs have

woefully underperformed.

But it was supposedly Mark Twain who said that “history doesn’t repeat itself;

it rhymes.”

No two timespans are ever identical. However, there are truths that tend to

apply no matter what. One of them is that slow-but-steady REITs usually do

come out ahead in the end.

You might be surprised to know that REITs were actually doing very well

earlier this year. From January to March, they were even outperforming the

larger equity market.

But then Trump unrolled his tariff plan… economists began to predict the end

of the world from inflation… and REITs lost a lot of their momentum.

That is to say their stocks did, as the markets lost confidence in their

ability to borrow at better rates. This does make sense. Somewhat.

Since REITs are mandated by federal law to pay out at least 90% of their

annual taxable income to shareholders, they have limited means to stockpile

cash. With limited means to stockpile cash, they have to do more borrowing.

And borrowing conditions under current interest rates favor lenders, not

“lendees.”

But that doesn’t mean quality REITs aren’t holding their own anyway.

REITs Look Good on Multiple Fronts

When REIT representative group Nareit published its mid-year evaluation last

week, it naturally acknowledged the tariffs situation. But it ultimately

concluded that “despite abundant investor concerns,” REITs are doing much

better than expected.

In fact, “REITs are generally well-positioned to weather any potential

fluctuations due to their solid property operations and strong balance

sheets.” And as for “increasing and/or elevated interest rates,” those don’t

automatically “equate to weak or poor real estate performance.”

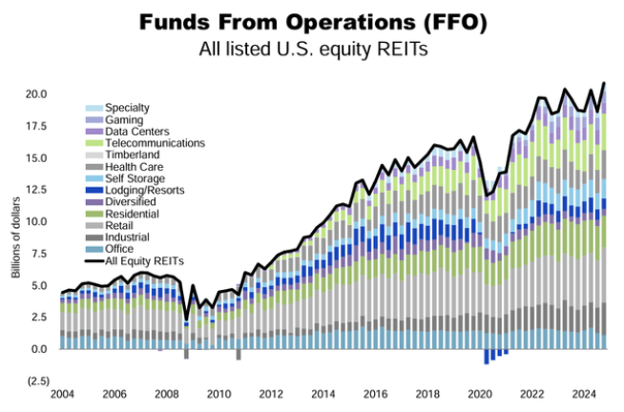

The truth is that REITs have done a great job of growing their funds from

operations (“FFO”) per share – their version of earnings – even in the midst

of elevated interest rates and investor concerns.

Source: Nareit

That’s largely because they learned their lessons after the 2008 housing

market crash. So many of them had been holding unwise amounts of debt, and it

took time and hard work to recover.

Really, it took new corporate mindsets about debt, taking advantage of good

times… and being properly prepared to take advantage of bad times. The

majority of REITs took all that to heart and haven’t forgotten it since.

That’s why so many of them have not only kept their earnings growing, but

their dividends as well.

Take a look at a REIT like Realty Income (O), the gold standard in the

triple-net space.

And yet, despite doing everything it’s supposed to do, the share price is

basically flat over the past five years. That’s disheartening, I know. But it

just goes to show that price performance doesn’t always tell you the true

value of the underlying company.

Given all that – their current health; their growth since 2008; and their

proven capability to thrive, high interest rates or not – REITs look

well-positioned to continue delivering positive results from here… even if

inflation increases.

Admittedly, I’m still rooting for interest-rate cuts. That would almost

certainly drive REIT returns, stock valuations, and investor profits. However,

it’s foolish to stay on the sidelines when there are so many attractive entry

points right now.

Nick Ward put it this way in the most recent update for

The Wide Moat Letter:

[REITs] have been beaten down in recent years because of rising interest

rates. But when that trend changes and the Fed makes a decisive dovish pivot

(which is what Brad expects to see happen over the next 12 to 18 months),

REITs are likely to act like coiled springs.We continue to recommend quality REITs before the rest of the market rushes

back into the sector. And for bargain hunters, there is no shortage of

values in the REIT portfolio right now.

I couldn’t have said it better myself.

Regards,

Brad Thomas

Editor, Wide Moat Daily

P.S. Check out my

YouTube show

this week, where I’ll reveal a handful of attractive REITs trading at a wide

margin of safety.

|