All may not be well in Las Vegas.

From Fox News:

Meanwhile, the Las Vegas Convention and Visitors Authority (LCVA) released its year-end summary for 2025 as well – and those numbers are worrisome to many.

There were 38,545,700 people who visited Sin City – down 7.5% from 2024, the report said.

[…]

Total occupancy in 2025 was 80.3%, with average room rates at $196.54 and a convention attendance of 5,988,200.

In comparison to 2024, convention attendance, visitors, occupancy and the daily roommate were all down.

Readers know we cover a variety of commercial real estate sectors. One of those sectors is gaming, which is why I keep such a close eye on the Las Vegas market. And, at first glance, things to seem worrisome.

But I also urged investors to stay calm two weeks ago in my article about VICI Properties (VICI). The gaming and experiential real estate investment trust (“REIT”) fell out of favor late last year due to tenant issues. And as I wrote on February 11:

Caesars Entertainment [CZR] remains its largest tenant with 18 properties, generating over $1.2 million in revenue and accounting for 39% of VICI’s annualized cash rent…

VICI has pulled back recently due to a softening in the Las Vegas market. Specifically, its Caesars Regional Lease saw a 28% decline in earnings before interest, taxes, depreciation, amortization, and rent/restructuring (“EBITDAR”) since 2021 – with a 13% increase in rent.

Given that Caesars is VICI’s largest customer, the market is understandably concerned about the low rent coverage (roughly 1 times), which could result in a lease reset.

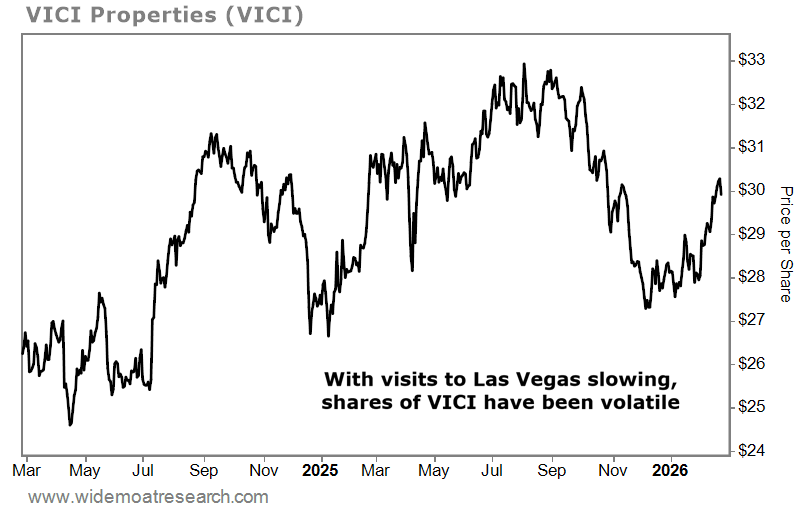

The result is that VICI has gone nowhere for the past 24 months. With visits of Las Vegas slowing, VICI share have been volatile.

But as I argued in that February 11 issue:

VICI now trades at 12.2 times price to [adjusted funds from operations, or AFFO]… below its normal multiple of 15.7 times. That makes its dividends yield a juicy 6.2%.

Analysts forecast growth of 3% in both 2026 and 2027. Given the “sum of the parts,” we believe VICI could return over 20% during the next 12 months.

Las Vegas is in a bit of a gully right now –no doubt. But VICI and Caesars are still quality companies with a tantalizingly cheap price tag. And I still believe that today, even after the latter’s Thursday report.

Betting on Caesars

Caesars Entertainment reported fourth-quarter and full-year 2025 earnings last week, where it did confirm continued pressure on the lower-end Las Vegas consumer. Even so, the casino operator’s digital outperformance brought about a much-needed perspective.

In the latest quarter, Caesar’s same-store consolidated net revenue and adjusted EBITDAR were up 4% and 2% year over year to $901 million and $2.9 billion, respectively – as expected.

Excluding the Caesars Digital segment, same-store brick-and-mortar adjusted EBITDAR fell about 5% year over year. Reported Las Vegas Strip adjusted EBITDAR came in at $447 million, in line with consensus. And regional adjusted EBITDAR was $404 million, below expectations of $408 million.

Digital, however, generated $85 million of adjusted EBITDA, above the consensus of $78 million. The iGaming business delivered 39% year-over-year non-gaming revenue growth, driven by the iGaming handle’s 25% year-over-year quarterly gain.

Management noted that cash on hand was $887 million (excluding $97 million of restricted cash). And traditional outstanding debt was $11.9 billion, resulting in financial net debt of $11 billion.

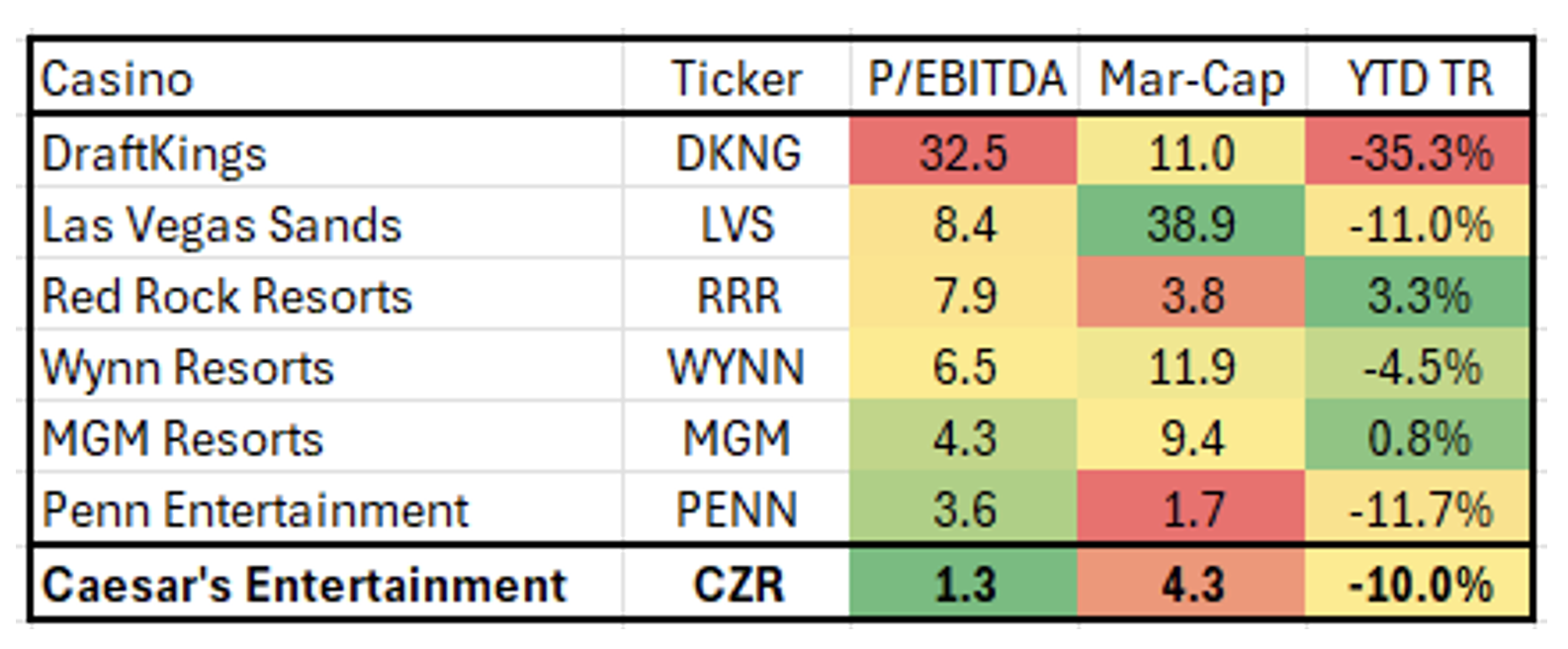

Shares are still trading at an incredibly cheap 1.3 times price to EBITDA compared with their normal 3.7 times. But whether that’s warranted or not revolves around the very big question of whether the Las Vegas Strip can grow again.

Caesars itself seems to think so considering how it repurchased 2.2 million shares last quarter. Perhaps it’s banking on a bump in leisure travelers after April. After all, as potential tax refunds begin to come in, consumers could very well begin to flow back into “Sin City” again.

The perception that operators have changed their pricing models in consumers’ favor could provide another boost still.

Then there’s the fact that Vegas has a strong events calendar this year, with more group/convention business picking up in the first half of 2026. And that’s to say nothing about the city’s evolution into a professional sports destination, hosting:

- The NFL’s Raiders

- The NHL’s Golden Knights

- The WNBA’s Aces

- The MLB’s Athletics as of 2028.

- The Formula 1 Las Vegas Grand Prix

All things considered, I like the entry point here for Caesars. Its diversified footprint and improving free cash flow profile boosted by underappreciated digital assets should help to deleverage its balance sheet.

And that, in turn, should accrue value for shareholders.

Wide Moat Research’s 12-month price target for Caesar’s is $36 per share, which translates into a total return of around 60%.

Source: Wide Moat Research

Betting on VICI

As for Caesar’s landlord, I maintain my confidence in VICI.

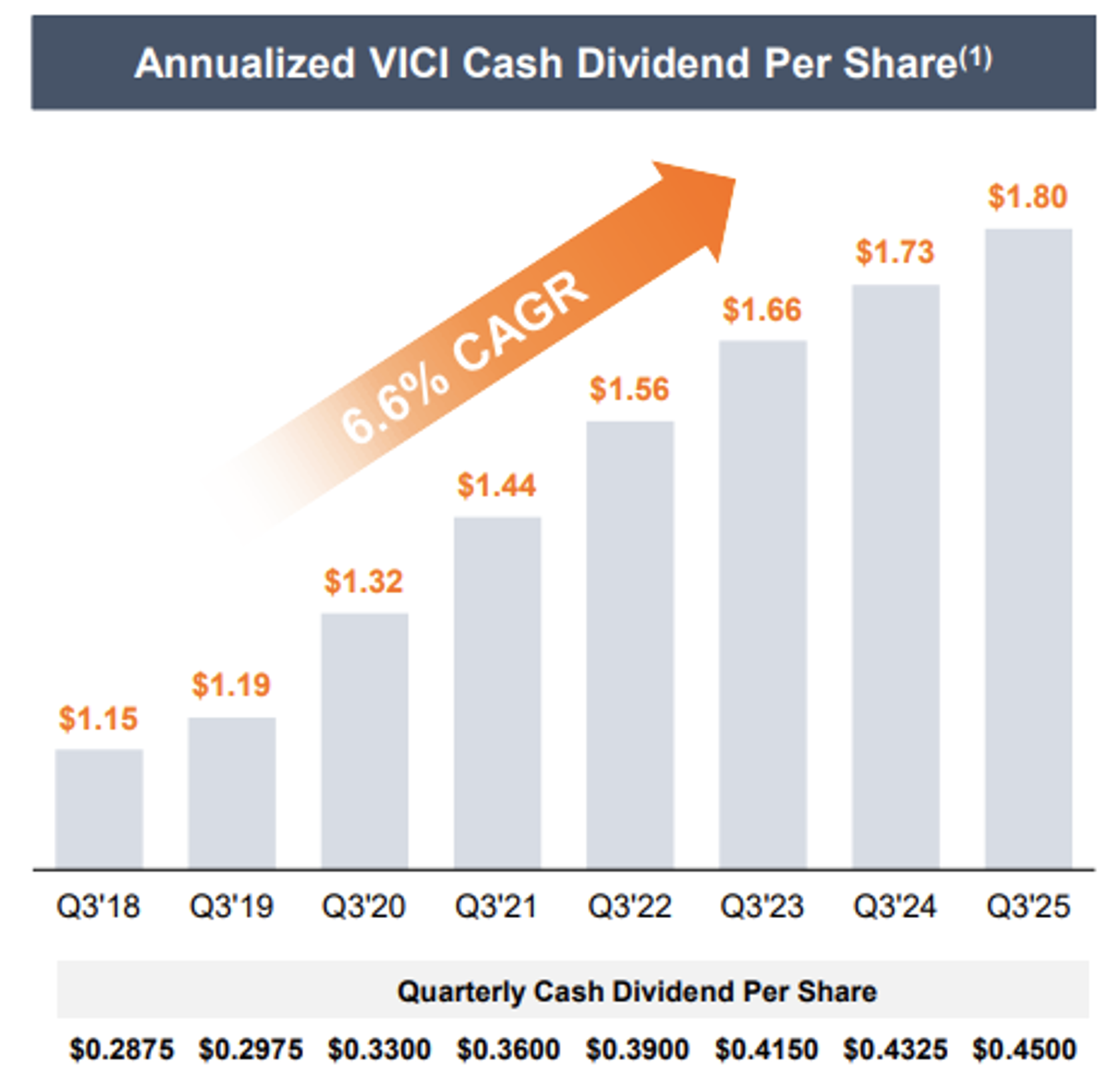

Its balance sheet, for one thing, is in great shape. At the end of the third quarter of 2025, VICI had total debt of $17.1 billion and 5 times net debt to annualized adjusted EBITDA. The capital markets discipline it maintains has allowed it to generate steady and reliable dividends for its investors.

Source: VICI Investor Presentation

Casinos do remain VICI’s largest tenant category by far. However, it has continued to expand its footprint into other property sectors such as wellness, theme parks, and family entertainment.

Management also mentioned last October that “university sports is definitely a big opportunity.” So, it’s probably just a matter of time before this net-lease REIT starts investing in athletic facilities as well.

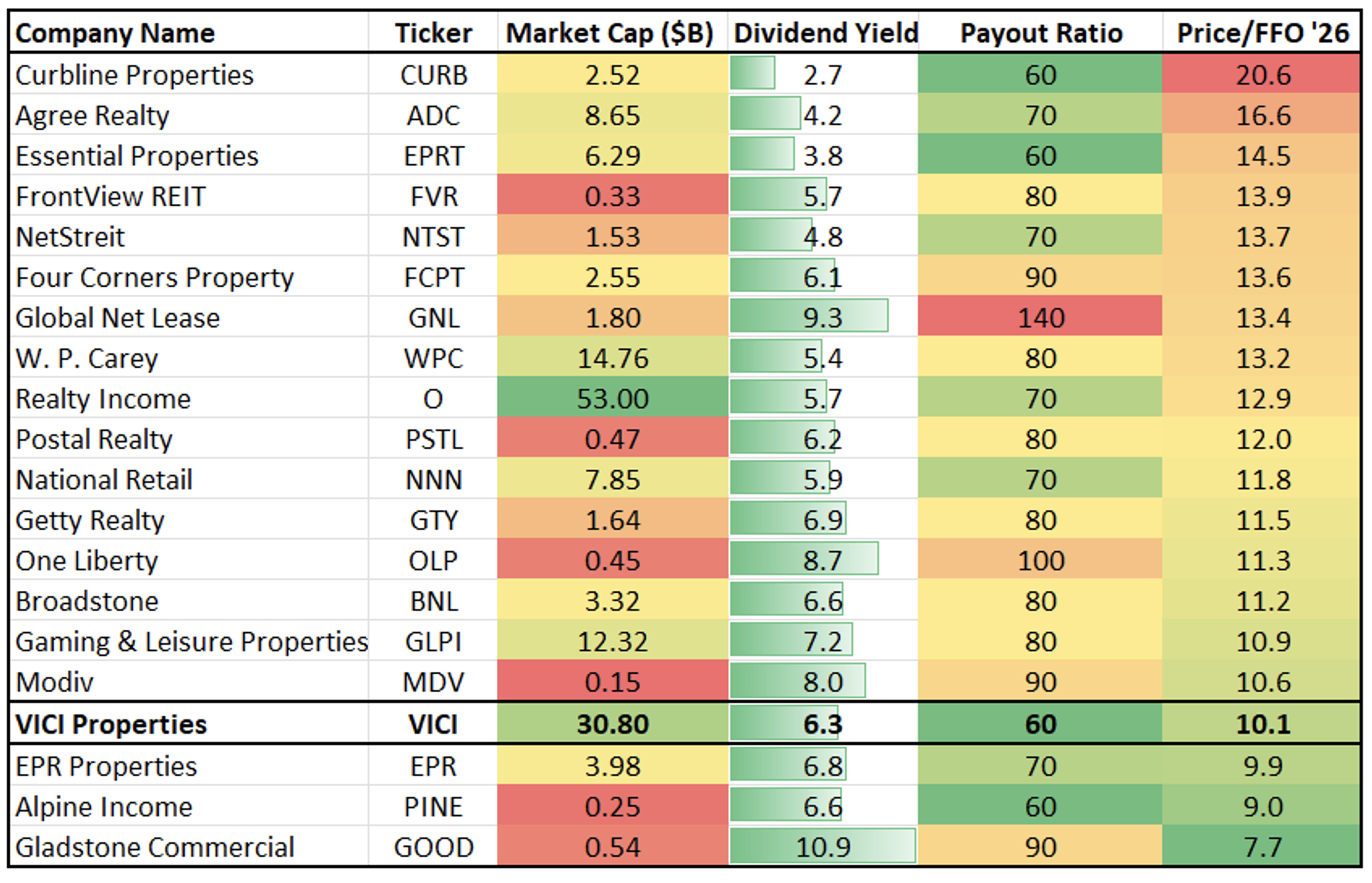

As seen below, VICI is trading at an attractive valuation of 10.1 times with a 6.3% dividend yield. Shares have returned around 7% year to date, 60% less than its largest peer, Realty Income (O) – which I wrote about on Monday.

Source: Wide Moat Research

As such, we see VICI outperforming in 2026. Don’t be surprised at all when this S&P 500 constituent continues to flex its muscle, generating sustainable profit margins that support future dividend increases.

As for its relationship with Caesars? Well, VICI has more than one way of keeping that substantial customer happy, including with a potential rent reduction if necessary.

That wouldn’t be ideal, of course. But it wouldn’t justify VICI’s current devaluation either. Again, the stock is trading well below what I’d consider fair value… and we want to be part of its rise back to where it should be.

By the time you read this, the REIT should have already released its fourth-quarter 2025 and full-year 2025 earnings. Take a look at them and see if you agree.

Regards,

Brad Thomas

Editor, Wide Moat Daily