There’s a lot going on in the world – the Federal Reserve, trade, and the ever-present artificial-intelligence narrative.

But, today, something completely different.

We’ll look at the pizza industry. Yes, really.

It might not seem exciting, but there might be more to like than you’d assume at first glance.

As my regular readers know, I was a real estate developer for over two decades. Those were busy years for me. I traveled up and down the southeastern U.S. to build retail properties of varying sizes.

I worked with nearly 100 companies, from smaller customers like Maurice’s BBQ to large tenants like Walmart (WMT) and Sherwin-Williams (SHW). All added up, I was responsible for over $1 billion in transactions.

I definitely had my favorites among that list – companies I really admired for one reason or another. Like Papa John’s (PZZA), one of my very first clients.

Back in the ’90s, I helped a friend grow his particular franchise from a handful of locations to over a dozen. Having previously run operations for KFC in Japan, he knew how to run a tight and successful ship. And I’ll admit I was envious.

It made me want to try it out myself.

But There Was a Problem…

The problem was, I had no experience outside of building brick and mortar. So as much as I wanted to branch out, I held off for years.

Then, one day, I called my friend up to ask him if he wanted to lease the last remaining space in a brand-new shopping center I’d developed in Chester, South Carolina. It was 1,500 square feet – perfectly suited for a Papa John’s.

His answer was that he was too busy to open another store. But he suggested I lease the space myself… by becoming a franchisee.

I don’t know why that made me set aside my concerns and go for it, but it did regardless. I set up a call with Papa John’s and, within a few weeks, I got green lit for three South Carolina stores.

As it turned out, that was a huge mistake… but I wouldn’t learn that until later.

One Store… Then Several

I opened my first Papa John’s store in Chester, the next in Newberry, and the third in Union. Within months, I was approached by a fellow franchisee who wanted to sell his store in Laurens.

And so I bought that one up, too.

Then, as fate would have it, another franchisee in North Carolina approached me about buying his four locations. That’s how I became the owner of eight stores far too quickly.

Source: Wide Moat Research

The cost for each store was something like $250,000, which means I had around $2 million invested in the business. $2 million with no experience in food operations whatsoever.

As it turned out, building retail locations was one thing. Operating them was quite another.

I was overwhelmed by the challenges of hiring – and training – managers. Dealing with ingredient logistics while controlling costs was another headache. And dealing with the (mostly teenage) employees was a nightmare. At one point, a disgruntled employee hauled a deer carcass into the store freezer. True story.

That’s part of why I ended up having to liquidate all of them.

It didn’t help that most of my net worth was tied up in a real estate partnership… in which my business partner was using our assets like an ATM machine. But I don’t know if I would have been able to keep my pizza business running anyway.

As I tell my friends, if you want to become a millionaire in the pizza business, just start with $2 million.

I Should Have Just Bought the Stock

With all that being said, pizza can be a wonderful business. The inputs (dough, cheese, sauce, etc.) are relatively cheap. The process of making them is mostly automated. And the markups on the finished product are sizeable. When done at scale, it can make for a nice business.

Which is why I would have been much better off investing in Papa John’s stock than its franchise business. And that might still be the case today…

As the world’s third-largest pizza delivery company, it has over 6,000 restaurants in approximately 50 countries and territories.

Papa John’s reported better-than-expected second-quarter 2025 results earlier this month. System-wide restaurant sales came in at $1.26 billion, up 4% year over year. And total revenue also rose 4% to $529 million.

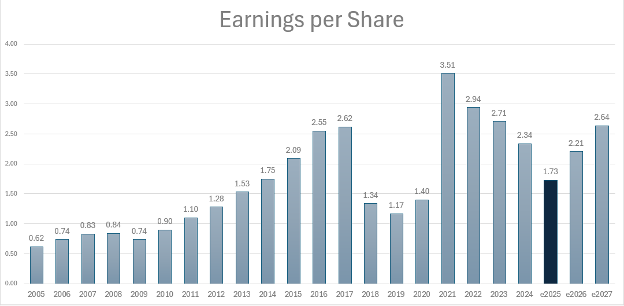

Turning to earnings per share, the company does admittedly have a lumpy earnings history. You can see in the chart below that it’s not expected to be so hot this year.

Source: Wide Moat Research

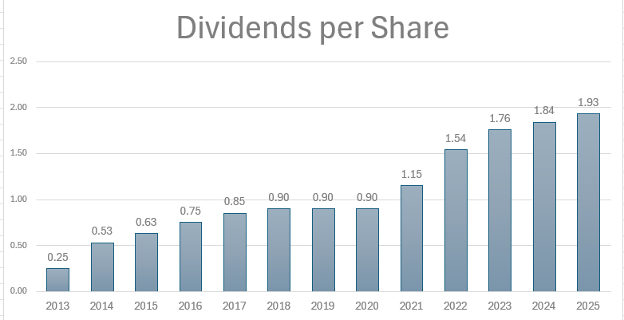

Even so, Papa John’s dividend history has been solid – growing by 21% compound annual growth rate (“CAGR”) since 2013.

Source: Wide Moat Research

So, is now a good time to buy? Before we answer that, let’s look at one of its top competitors…

Domino’s on Display

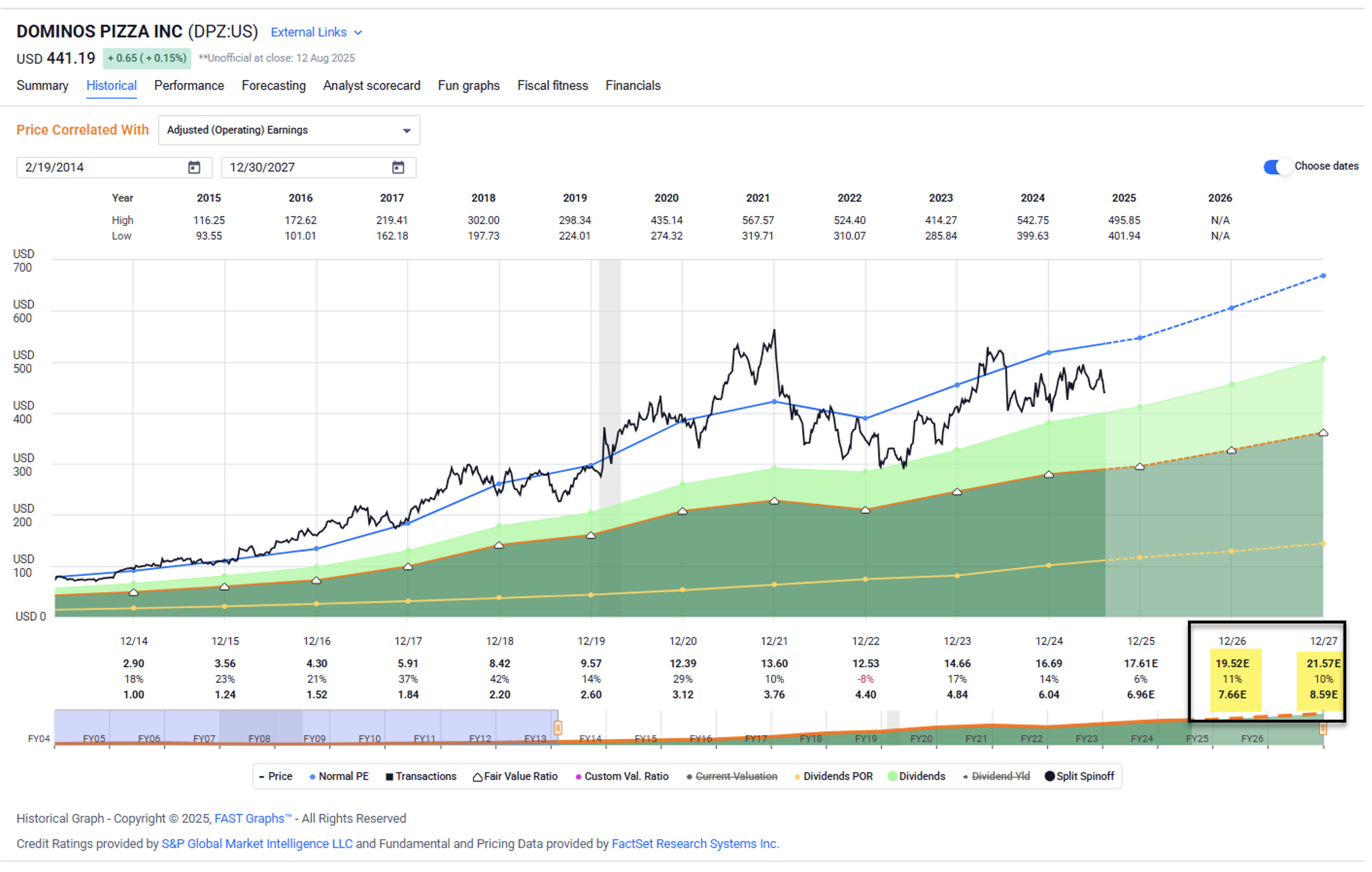

Domino’s Pizza (DPZ), which was founded in 1960, now operates more than 21,300 stores in 90 international markets around the globe.

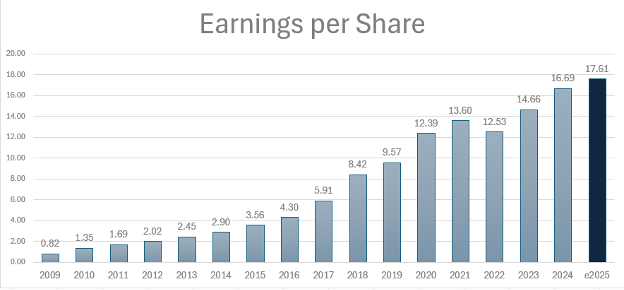

One particularly interesting tidbit about Domino’s is that around 95% of its franchisees start out as pizza makers or delivery experts. That might just explain its earnings history, which is much more stable than Papa John’s.

It boasts a 22% CAGR since 2009.

Source: Wide Moat Research

In the second quarter of 2025, Domino’s revenue grew slightly ahead of expectations, coming in at $1.15 billion against a $1.14 billion estimate. And income from operations increased 14.9%.

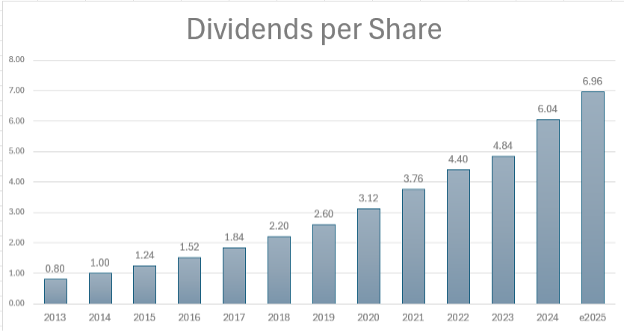

It also features a solid dividend history, with 20% CAGR since 2013, when it began that program.

Source: Wide Moat Research

Based on fundamentals, I give Papa John’s a C+ and Domino’s an A-. But as I always stress, it’s not just quality we need to consider as investors.

Valuation is equally important. In which case, Papa John’s is trading at 23.5 times earnings – below its normal 32.8 times.

Its dividend yield is 4%, which is tempting at first glance. However, we have to remember its unimpressive full-year earnings forecast. Combine that with its dividend-to-free-cash-flow payout ratio of 107%…

And Papa John’s dividend has to be called into question.

Then again, analysts are forecasting solid growth in 2026 and 2027 of 28% and 19%, respectively.

Source: FAST Graphs

Domino’s, meanwhile, is trading at 25.6 times compared with its normal 31.1 times. So again, it looks like a bargain at first glance.

At 1.6%, its dividend yield is much lower than Papa John’s. But it’s also much safer based on its free cash flow payout ratio of just 38%.

Analysts expect it to grow 11% in 2026 and 10% in 2027.

Source: FAST Graphs

In short, both pizza chains are undervalued. And when it comes to taste, well, I know I have my favorite. But I’m sure you do, too, so order as you so choose.

When it comes to fundamentals, Domino’s is the definite winner. However, I’m hardly bearish on Papa John’s long term.

I recently added another former customer of mine, Advance Auto Parts (AAP), to Wide Moat Confidential, my small-cap service. And shares have mushroomed since by around 95% in just over 90 days.

Similar to AAP, Papa John’s is also in turnaround mode. Its new CEO has been there for about a year now, and he’s successfully returning the company to positive comparable sales and transaction growth in North America.

The Louisville-based chain is laser-focused on continuing to execute its strategy to grow restaurant sales, generate sustainable profits, and build long-term value for shareholders.

So ultimately, while I wouldn’t bet $2 million on pizza like I did two decades ago – and while I’d caution you before doing the same – I do think Papa John’s and Domino’s are both ideas worth looking into.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|