While my passion for a certain niche of the market was on full display in yesterday’s article… I’m the first person to admit that there’s more to investing in life than real estate investment trusts (“REITs”).

There’s also their “cousins” known as business development companies, or BDCs.

These two asset classes share some obvious and important similarities. Perhaps most importantly is how they’re legally required to distribute at least 90% of their taxable income.

REITs, created in 1960, were the first business class to operate under this “pass through” structure. They pay no taxes on their annual income, passing those savings onto their holders.

BDCs then followed that same blueprint in 1980, only as closed-end venture capital funders. They help finance businesses that would otherwise struggle to get loans, usually through secured, high-rate offerings. Their typical clients are smaller companies valued at less than $5 billion – often those that have been taken private in leveraged buyouts.

If that sounds a bit risky, it can be. That’s why BDCs tend to come with double-digit yields that could tempt even an investment saint. These days, most yield 11% or higher. So it makes sense that some income investors are obsessed with them.

As for me, I’m still a REIT man at heart. I appreciate the greater safety that comes with quality real estate. And I like how much they tend to grow their dividends, with the average yield being 4.1%.

When I purchase a REIT, I know I’m investing in a portfolio of brick-and-mortar assets. That means, more often than not, I can visit any of its properties to determine whether that source of income is viable.

I actually conduct that kind of “boots on the ground” research often… visiting my local mall owned by Simon Property (SPG)… a nearby shopping center owned by Kimco Realty (KIM)… or my local theater owned by Realty Income (O).

BDCs, however, are essentially a second tranche of private equity. And you have to approach them differently.

Here’s what you should know before diving into these assets…

BDCs versus REITs

Since they’ve been around for two decades longer, it makes sense that the REIT universe is bigger than the BDC’s.

According to industry expert Nareit, REITs own over $4.5 trillion of commercial real estate assets, including listed and non-listed public and private equity and mortgage REITs. BDCs, meanwhile, have around $451 billion of assets under management.

That in and of itself isn’t a problem, of course. And it does make sifting through the possibilities less complicated.

What is more problematic is how BDCs come with increased volatility relative to junk bonds and leveraged loan funds that use little to no actual leverage. The very nature of their business is riskier. But the reward, of course, is often double-digit yields.

Many REITs, however, have investment-grade rated balance sheets that allow them to obtain lower costs of capital… which in turn helps them generate wider investment spreads.

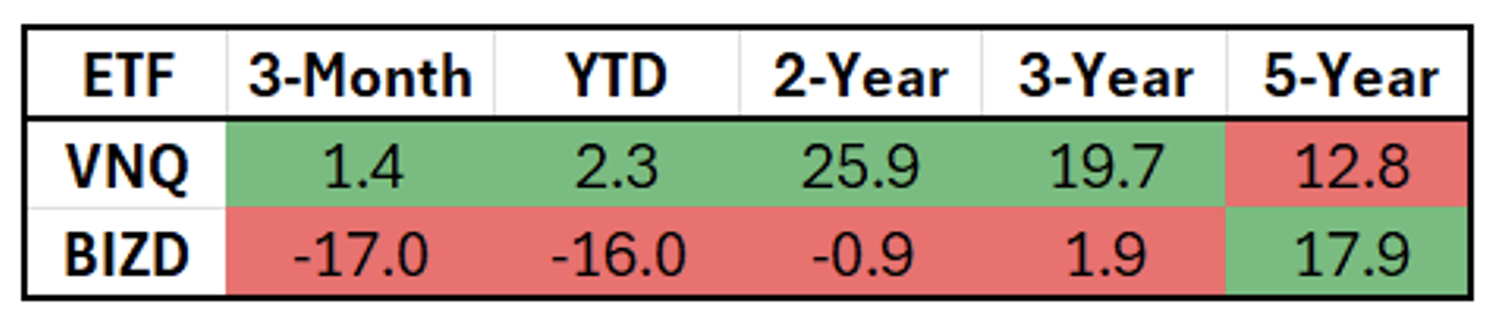

In terms of overall performance, consider Vanguard Real Estate Index Fund ETF (VNQ) and VanEck BDC Income ETF (BIZD).

Source: Wide Moat Research

Don’t get me wrong, REITs returning 2.3% year to date is hardly something to celebrate. Not when the S&P 500 (SPY) has grown by 13.4% and Invesco QQQ ETF (QQQ), which tracks the Nasdaq 100, is up 18%.

But it’s still a whole lot better than BDC performance. Since mid-September, especially, BIZD has fallen to a new 52-week low under $14.

Source: Yahoo Finance

That’s partially because rate cuts serve as a positive catalyst for REITs… but a negative one for BDCs since most of their loans float at a yield premium above short rates.

Plus, the private-credit industry is spooked by the recent bankruptcy of auto-parts distributor, First Brands… which recently acknowledged that it has $2 billion unaccounted for.

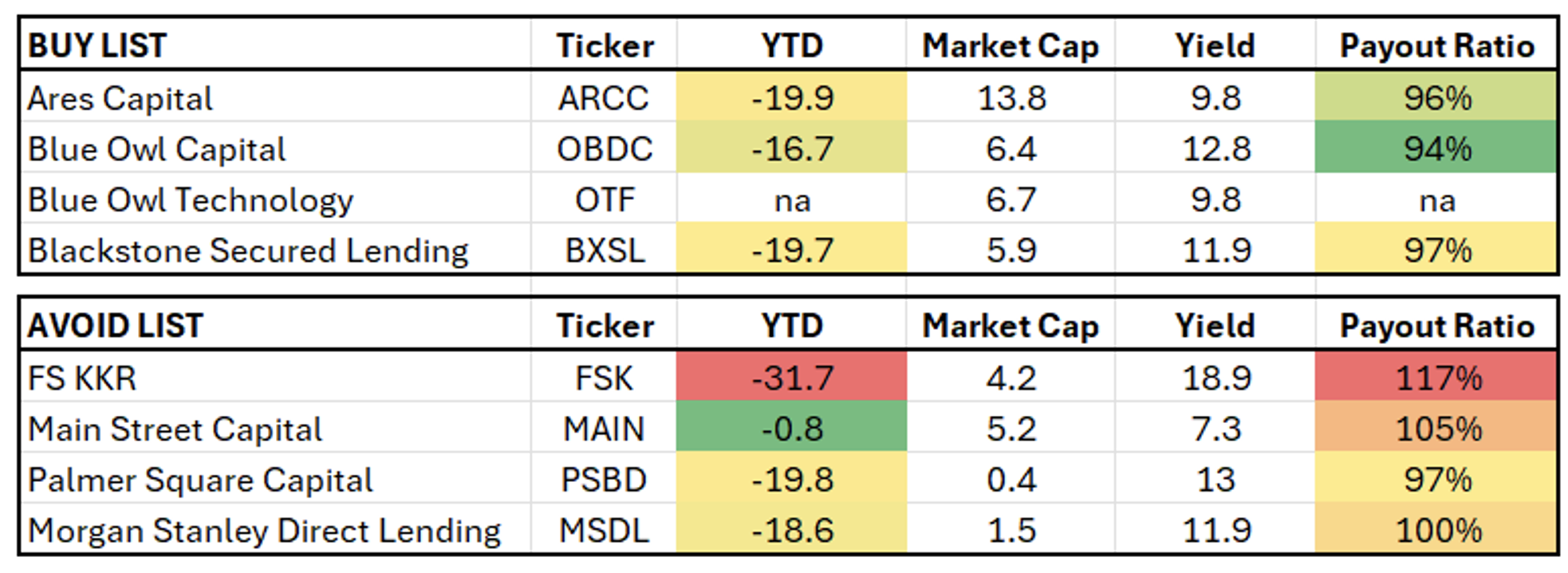

Palmer Square Capital (PSBD), a BDC, has modest exposure to First Brands. It was enough, however, to send shares crashing to a 20% discount.

The company sports a current 97% payout ratio. So, based on analyst consensus estimates for 2016 of -6% growth, it’s probably going to have to cut its dividend before long.

In fact, many BDCs face that same risk, including FS KKR Capital (FSK). It now yields 19% since its shares are so cheap – and understandably so.

Accruals, (which are loan payments not made for at least 90 days, have approached 5%. And its payout ratio is 117% based on 2025 earnings per share.

That’s unsustainable.

Another one to watch out for is Main Street Capital (MAIN), which is, unfortunately, a retiree favorite. It pays its dividends monthly and has grown that payout by 132% since its October 2007 IPO.

Even so, its payout ratio is 105%. And lower interest rates could spark dividend cuts from here.

Two Better BDCs (and a Final Word of Caution)

With all that said, I do understand the quest for yield. And BDCs can do very well under the right circumstances.

Ares Capital (ARCC), for one, is the largest BDC with a market value of just under $14 billion. Better yet, it has a solid investment-grade balance sheet, rated BBB, making its 96% payout ratio reasonable.

Shares are down around 17% over the past 90 days, offering a 10% dividend yield.

Two other BDCs on my buy list are Blue Owl Capital (OBDC) and Blue Owl Technology Finance (OTF).

Blue Owl Capital boasts a well-covered payout ratio of 94%, a BBB- rated balance sheet, and an 11.8% dividend yield. And shares are trading at an 18% discount.

As for Blue Owl Technology Finance, it pursues sponsor-backed upper-middle-market companies in non-cyclical sectors, particularly software. Its dividend yield is 9.7%, and shares are trading at a rich 20% discount.

Even so, keep in mind that BDCs generate lumpier earnings. Analysts actually expect their collective earnings per share to decline this year, next year, and again in 2027.

My bottom-line conclusion is that REITs are safer investments than BDCs, especially now. But I completely understand if you’ve got the will and the means to try the latter and chase yield.

Stephen Hester runs our High-Yield Advisor service where he tracks and recommends high-yielding assets like BDCs. Here’s how he spelled out the recent status of that market in the latest issue:

I strongly believe that [our current BDC holdings] currently trade at near-distressed levels. Yes, it’s true that non-accruals have been rising. Yes, there has been some net asset value degradation with a few BDCs. But that is part of the economic cycle.

And many of these non-accruals will eventually be written up, and the losses are likely to be less than anticipated.

As always, maintain responsible diversification within the sector to limit catastrophic meltdowns. And never forget to avoid becoming the next “sucker” of a high-yielding “sucker yield” stock.

If it looks too good to be true, it probably is.

Source: Wide Moat Research

Happy SWAN (sleep well at night) investing!

Regards,

Brad Thomas

Editor, Wide Moat Daily

|