A Note from Brad: Before we get to today’s issue, I have a quick favor to ask. It’ll only take two minutes.

Over the past several years, the team at Wide Moat Research has worked hard to show you how to capture big wins and use income strategies to outperform the market.

But we can always do things better, right?

Today, I’m hoping to hear from you about what that might look like…

So, can you please take just a few minutes to answer some quick questions about your experience, and share what we can do better?

Our team will read each and every response and work through your feedback as a group.

Click here to share your opinion.

Again, we want to hear it all…

What stocks did you buy? Have you had any success? How could we do better?

We know how busy everyone is, so we designed the survey to only take a minute or two.

Thank you again for being such a valued member of our community. I can’t wait to hear your thoughts.

When I first started out in commercial real estate development, I only dealt with free-standing properties across the Southeast.

It was less hassle finding good sites for businesses like dollars stores, drugstores, and auto-parts shops. So that’s who I signed my contracts with.

I was pretty good at finding tracts of land for these properties throughout the Carolinas, Georgia, and Virginia. But when Advance Auto asked me to scout out Alabama, it got a bit more complicated.

Venturing into the town of Cullman, I first headed to the local Walmart, as I always did. Those well-trafficked stores made great businesses to piggyback off of. All I needed was a nearby plot of land to build on.

In this case, several similarly minded businesses had already gotten there. So, there was no place to build…

Except for a two-acre space, which was too large and quite clearly didn’t feature a “for sale” sign.

Undaunted, I tracked the owner down to offer him $250,000 for a portion of his site. Equally unphased, he gave me a definitive response: He would sell the whole thing or nothing at all.

I thanked him for his time but declined the opportunity, hopping into my car for the long trip home.

It seemed like such a shame though, and I kept pondering the site as I drove.

I wanted it. There was no two ways about it. But I’d have to find another tenant if I was going to buy the whole two acres.

Back in my office, I sketched out a plan that included a free-standing Advance Auto and a small, 10,000-square-foot shopping center. Then I called the guy back, made an official offer of $575,000 (which he accepted).

And I got to work finding tenants for my very first shopping center.

That was how I learned first-hand how profitable this commercial real estate (“CRE”) category can be. And in case you were wondering, yes, those building were constructed and stand to this day.

Cullman, Alabama

Don’t Underestimate the Humble Shopping Center

I know shopping centers might not seem the most exciting investments. I’d venture to guess that you drive by properties like the one pictured above about a dozen times a day. But that’s exactly what can make them sturdy profit-generators.

Here’s an interesting finding: For all the talk of e-commerce, online sales only account for about 16% of total retail purchases according to the U.S. Census Bureau. And while that figure has grown significantly in recent years (it was about 7% in 2015) it means that the lion’s share of consumer purchases are still done the old-fashioned way – going to a store and buying the thing yourself.

Despite this, the sector has been mostly unloved by Mr. Market in recent years. The FTSE Nareit Shopping Center Index – which broadly tracks the performance of public real estate investment trusts (“REITs”) in this space – is down about 5% over the past year.

But that negative sentiment can also mean attractive valuations for high-quality REITs in this space before sentiment turns again (it always does eventually). That’s why retail CRE still deserves your attention and (possibly) your investment.

There are 14 REITs in the Wide Moat Research shopping center coverage list. And while that opens a wide window of investment opportunity, there are clear standouts to hone in on.

One of the top players in this sphere, without a shadow of a doubt, is Federal Realty Investment Trust (FRT).

A Closer Look at FRT

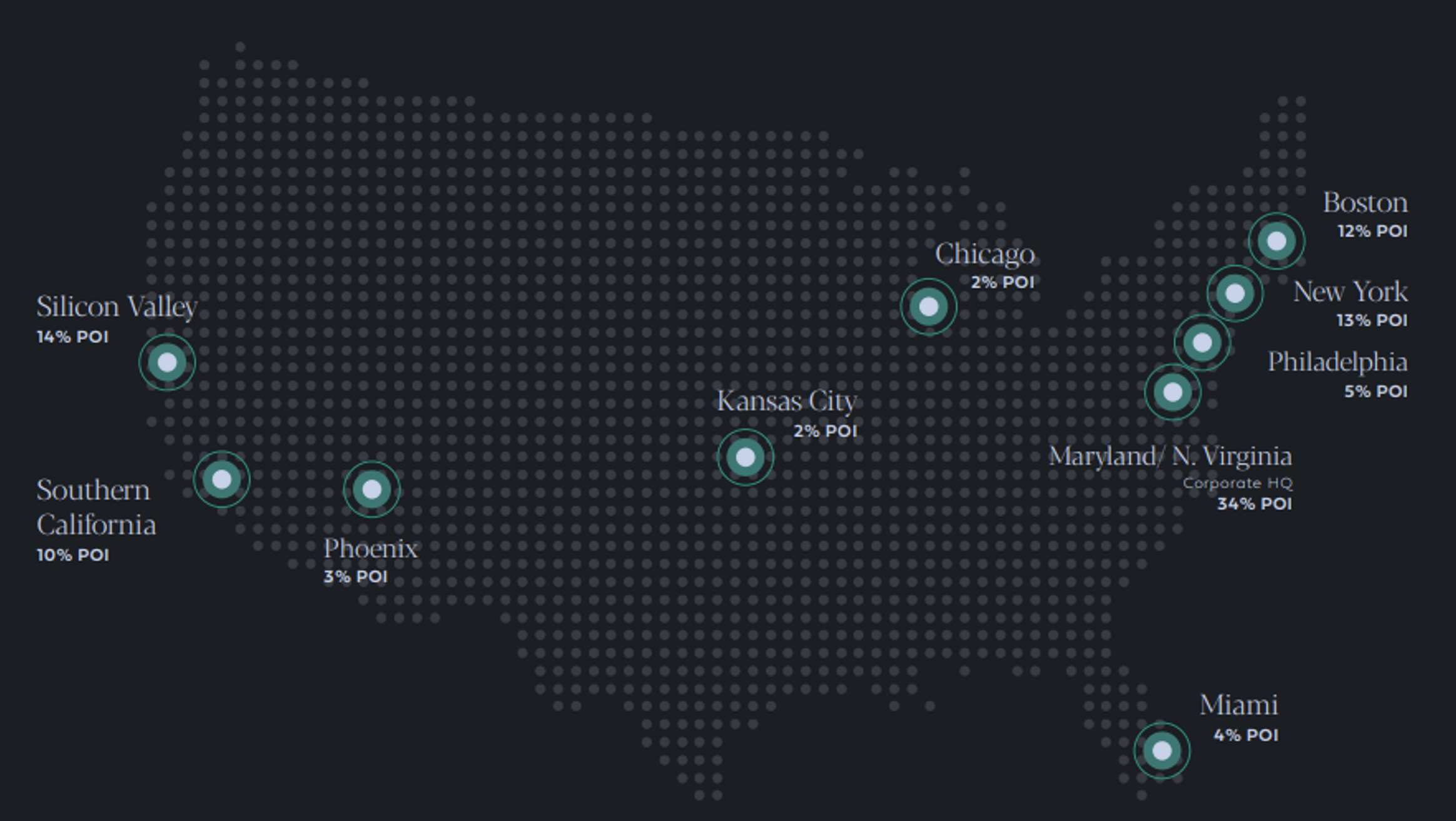

It owns a total of 102 open-air properties, 27 million square feet of commercial space, and 3,000 residential units. This portfolio generates 79% of rental income from retail customers, 10% from office clients, and 11% from residential tenants.

These are concentrated in well-populated and affluent areas such as Silicon Valley, Boston, and the greater D.C. commuting line:

Source: Federal Realty

Federal Realty was founded in 1962, so it has obviously survived – and thrived – through so much change already: economic recessions… market volatility… periods of REIT investment favor and fear…

That’s in large part because it always insists on quality management, no matter the times. These leaders make sure to balance savings and growth that keep the REIT in a constant state of readiness for whatever comes its way.

For instance, Federal Realty’s current C-suite team has secured over $1.5 billion of liquidity. That gives it ample capital to develop new projects, such as the 3,200-plus residential units in its pipeline and the near 7 million square feet of major active rezonings in process.

The REIT has a BBB+ credit rating from S&P and a Baa1 from Moody’s. And no wonder. Its solid credit metrics include a 5.4 times annualized net debt to earnings before interest, taxes, depreciation, and amortization (EBITDA) multiple and a 4 times fixed-charge coverage.

Perhaps the most convincing differentiator for Federal Realty, however, is its dividend history, which is unmatched in REIT-dom. With 58 consecutive years of dividend increases, it easily qualifies as a dividend king – a title reached when a company has achieved a half-century of such ever-rising payments.

Federal Realty is trading at 18.9 times price to adjusted funds from operations (“AFFO”) compared with its normal multiple of 25.3 times. Its dividend yield is 4.5%, and analyst growth estimates are for 7% in 2025, 6% in 2026, and 7% in 2027.

Source: FAST Graphs

With these figures in mind, I suspect Federal could return around 20% annually over the next 12 months. This forecast is based on a combination of yield, growth, and modest price appreciation of 10%.

Shopping Center REIT No. 2: Regency Centers

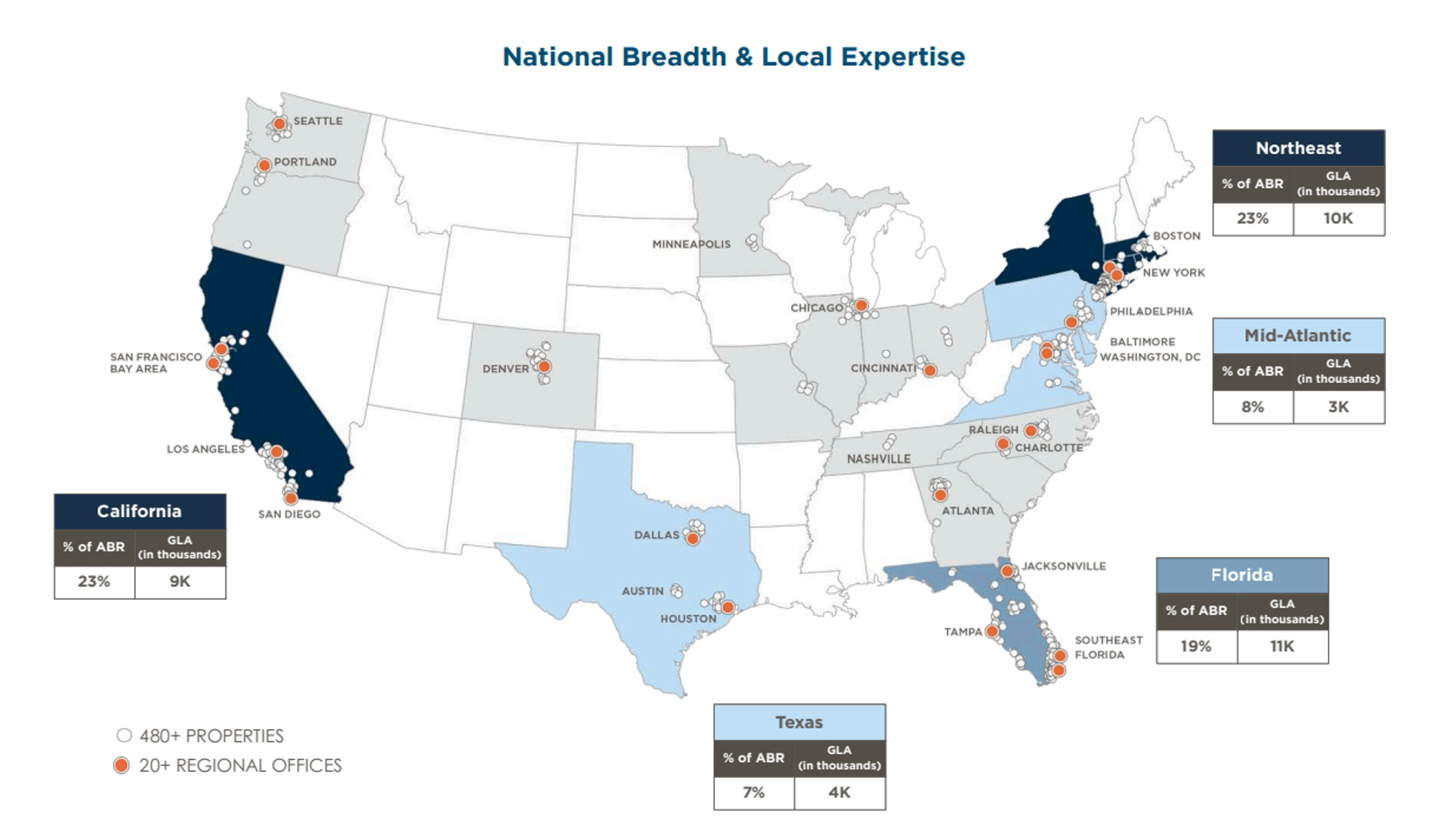

Regency Centers is a Jacksonville-based shopping center REIT that focuses on suburban trade areas with compelling demographic trends. It operates in 20 markets with 480 properties, around 85% of which are grocery anchored.

Grocery-anchored neighborhood and community centers, you see, have lower capital expenditure requirements. They also boast high customer visits, since people go to pick up groceries every week.

In addition, these properties have below-average exposure to at-risk tenant categories such as Burlington and Kohl’s. And they offer greater landlord control and flexibility.

Another positive is Regency’s tenant roster, which includes names like Publix, TJ Maxx, Albertsons, Whole Foods, Kroger, Ahold, and CVS. In fact, this REIT is the top landlord by store count for many leading, best-in-class U.S. grocers.

Source: Regency Investor Presentation

As with Federal Realty, Regency has an impressive balance sheet, rated A- by S&P and A3 by Moody’s. The company intentionally prioritizes conservative leverage levels and a laddered debt maturity schedule, with no more than 15% of total debt maturing annually.

Its credit metrics are solid, too. Leverage remains in the 5 times to 5.5 times range in terms of net debt and preferred stock to operating EBITDA for real estate. And Regency has ample capacity and flexibility for opportunistic investments.

Also keep in mind that while this REIT did cut its dividend in 2008 and 2009, it held firm in 2020.

As you can see below, shares are trading at 19.5 times price to AFFO compared with its normal 22 times multiple. Its dividend yield is 3.9%, and analysts expect growth of 9% in 2025, and 5% in 2026 and 2027.

Source: FAST Graphs

Although Regency Centers is not as cheap as its peers, I must stress the quality of its business model and the stress-free nature of its rental stream. Given its current valuation, I believe it could return around 15% over the next 12 months.

And make sure to tune into our YouTube show this week, where we’ll discuss a larger retail shopping list of three retailers and three retail REITs. It’s going to be a good one!

You can subscribe to the show (and catch up on past episodes) right here.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|