Movie watchers want what they want.

And woe to the Hollywood execs who don’t produce it.

That seems to be the story right now as the U.S. box office suffers yet another miserable year. To quote the Los Angeles Times:

The total theatrical haul for the summer – which, for industry watchers, stretches from the first weekend of May through Labor Day – grossed $3.67 billion in the U.S. and Canada, down slightly from $3.68 billion in 2024, according to Comscore. The numbers are even more sobering compared with 2023’s Barbenheimer-fueled summer sum of $4 billion, a target the industry used to hit routinely.

Following summer box office figures might seem like a strange topic to cover, but it’s for a good reason. I make it my business to track just about every category of commercial real estate (“CRE”). That includes movie theaters. And outside of offices, you might be hard-pressed to find a more troubled area of CRE since the COVID-19 era.

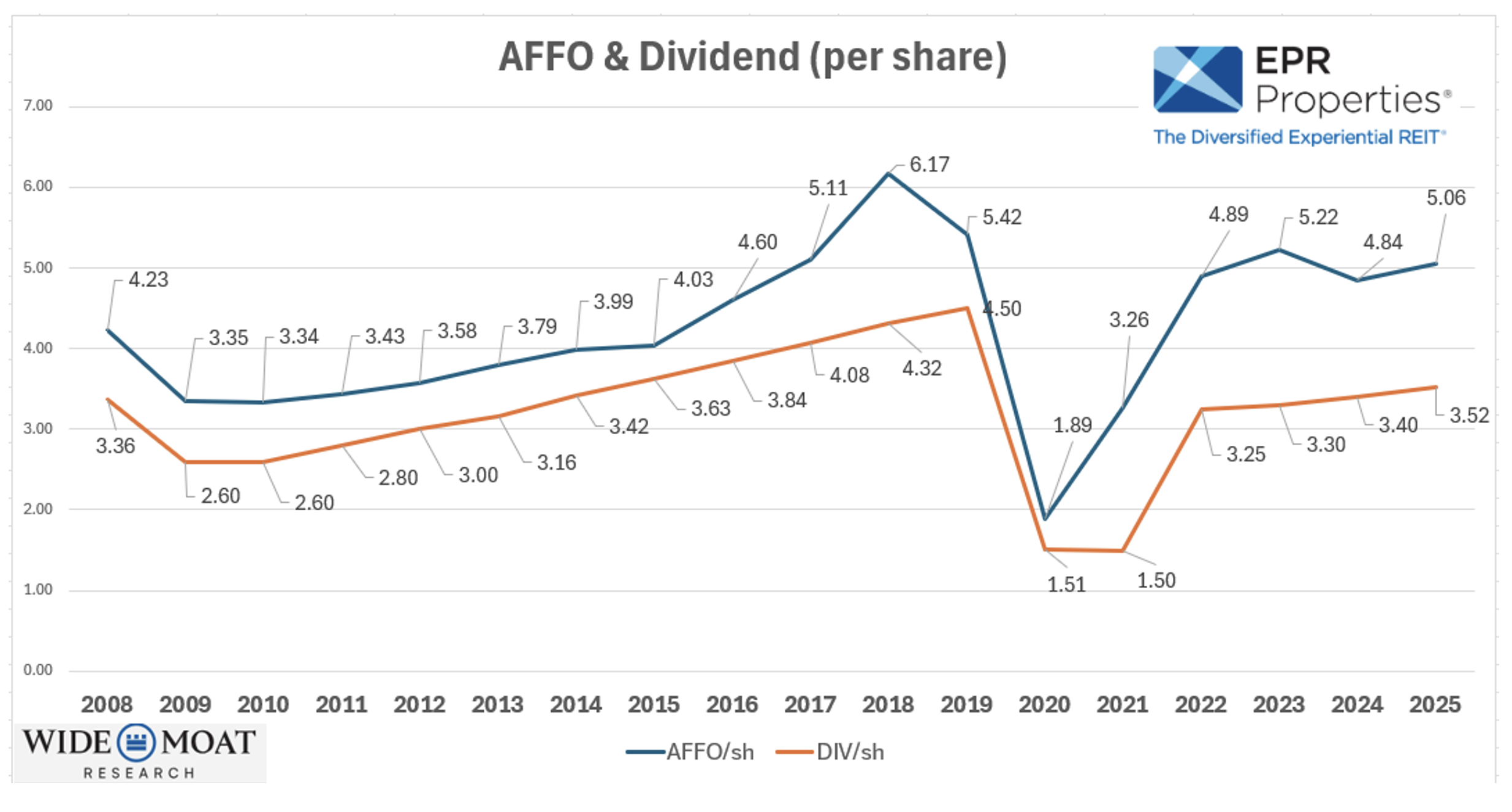

On my last episode of The Wide Moat Show, I profiled EPR Properties (EPR), a real estate investment trust (“REIT”) historically known as a movie theater landlord. I shared this chart:

The company’s adjusted funds from operations (“AFFO”) understandably took a hit during COVID-19. And the company – again, understandably – cut its dividend. But even though we’re five years on from that era, EPR has yet to recover its previous AFFO levels. Its dividend also is below pre-COVID levels. That’s why I listed EPR as a REIT to avoid.

In the CRE-watching world, people have been wondering if movie theaters could ever reclaim their former glory. The answer, so far at least, is no.

In addition to the numbers mentioned above, we’re now getting reports that the Stephen King adaption, The Long Walk, performed badly as well. Starring Mark Hamill, it only earned $11 million over the weekend.

For comparison, King’s It made $123 million when first released in 2017.

Some might be quick to point out how the world-famous author angered conservatives right before The Long Walk debuted by maligning Turning Point USA founder, Charlie Kirk, a mere day after he was assassinated. And while King ended up deleting the post and even apologizing for it, feelings remain understandably raw.

So, yes, that misstep might very well have factored into the movie’s poor performance so far. However, King had two other adaptions earlier this year that also underwhelmed.

In February, The Monkey made just $14 million when it opened. And The Life of Chuck was even worse, with a weekend debut of $224,000.

So with all very much deserved respect to Charlie, I’d say something else is going on at the box office. Something I don’t think big-name production companies like Paramount Skydance (PSKY) quite know how to fix.

So, they’re angling to do what businesses always do when an industry faces trouble – join forces.

The Hollywood Dilemma

You probably saw by now that Paramount wants to buy up rival Hollywood studio Warner Bros Discovery (WBD). While no formal announcement has been made – and we’re now hearing that it might take a little longer to happen – we do know a bid is being prepared.

Both stocks shot upward on the news last week. And they’ve largely retained those gains, leaving many to speculate how much further they can go once an official offer does appear.

It’s a tempting thought to some, but I’m not buying. I don’t see how any price pop is sustainable right now. Not when movie ticket sales are what they are.

There’s a range of arguments for why they’re so abysmal, many of which make sense. These include how:

-

Hollywood actors and writers have felt the need to wade into political and social issues, angering some would-be customers. King might be one example. Rachel Zegler, star of Disney’s live-action Snow White, might be another. As a general rule, angering potential customers is bad for business.

-

The shutdowns themselves left people nervous about congregating in crowded spaces.

-

The push to stream movies more quickly – and more cheaply – has dulled moviegoers’ appetite to actually go to theaters. Streaming is arguably a better experience as well (you can pause, rewind, or even watch a movie over several days)

-

Inflation has made life far too expensive to justify an $11.50 ticket (plus another $5 for a medium soda and $8 for a medium popcorn). At high-end theaters, it’s even more expensive – in the range of $22 to $25 for just a single ticket.

Those are all valid points, but I don’t think they’re the biggest cause. After all, as the LA Times mentioned, 2023 saw massive crowds come out to see big-name stars in movies like Barbie and Oppenheimer.

Even this terrible, horrible, no good, very bad year, the much-maligned Disney (DIS) proved it can still produce global blockbusters with its $1 billion live-action Lilo & Stitch. And A Minecraft Movie made $957 million.

Despite everything, including ever-climbing inflation, people still plunked their money down for a night out at the movies. It’s just that they did so with purpose, only buying when they really thought it was worth it.

Give the Investors What They Want

By my analysis, Hollywood’s biggest problem is simply that it isn’t giving the people what they want anymore.

It got lazy on the success of franchises like Star Wars (Disney) and Marvel (Disney) and D.C. (Warner Bros.) superheroes. Popular book adaptations, too. Those movies had made money – and lots of it – in the past.

So why not keep a good thing going until it’s no longer a good thing?

Well, we have the answer now… especially since Hollywood began twisting those beloved storylines completely out of shape. The unsurprising end result was that audiences left feeling dissatisfied and less likely to engage in the future.

Judging by the last few years, producers haven’t learned their lesson yet. Not really. And I’m not willing to recommend them until they’re more in tune with the customers who fund their salaries.

Now, I do understand the investment argument when it comes to investing in Paramount specifically. Its second-quarter earnings per share was $0.46, beating expectations by 31.43%. And while revenue of $6.85 billion didn’t match anticipations, it was only off by $0.02 billion.

It should also be noted that Paramount+ gained 9.3 million subscribers over the same quarter of 2024. The company says the service is “on track” to even turn a full-year profit in 2025 for the first time since launching.

Overall, consumer-generated revenue of $2.2 billion was up 15% year over year. And acquiring Warner Bros could very well strengthen Paramount from here, giving it greater scope, scale, not to mention access to some beloved franchises – Harry Potter, Game of Thrones, the D.C. comic book universe, etc.

Even so, I remain concerned about how many watchable movies and shows it will actually produce in the foreseeable future.

I’m not saying the company – or Hollywood in general – is dead in the water or has no hope of investable growth from here. I only mean that I don’t see any reason to nominate it for your portfolio right now.

Not until I see consistently better box office results and streaming profits.

The same goes for REITs like EPR Properties, mentioned above. I stand by that analysis today.

Personally, I prefer recommending businesses with durable competitive advantages: ones that are capable of generating reliable and predictable income. That’s why, next week, I plan to reveal my highest-conviction sleep-well-at-night (“SWAN”) picks on my Wide Moat Show on YouTube.

This will be a show worth watching, and I hope to see you there.

Happy SWAN Investing!

Brad Thomas

Editor, Wide Moat Daily

|