The cold-storage story might not look so hot these days. But that wasn’t the case a few years ago.

Cold storage – the industry that specializes in storing temperature-controlled perishables such as frozen produce, dairy, and juices – was rolling in profits back in 2020.

That’s when people stopped going out to restaurants, cooking at home instead to avoid catching COVID-19. Grocery stores needed to be stocked and restocked more quickly as a result. And that meant more food was flowing through cold-storage facilities on the mass-distributed food “assembly line.”

Recognizing this, investors made cold storage giant Lineage (LINE) – a real estate investment trust (“REIT”) – the largest IPO of 2024. Many assumed that cold storage’s run was never going to stop.

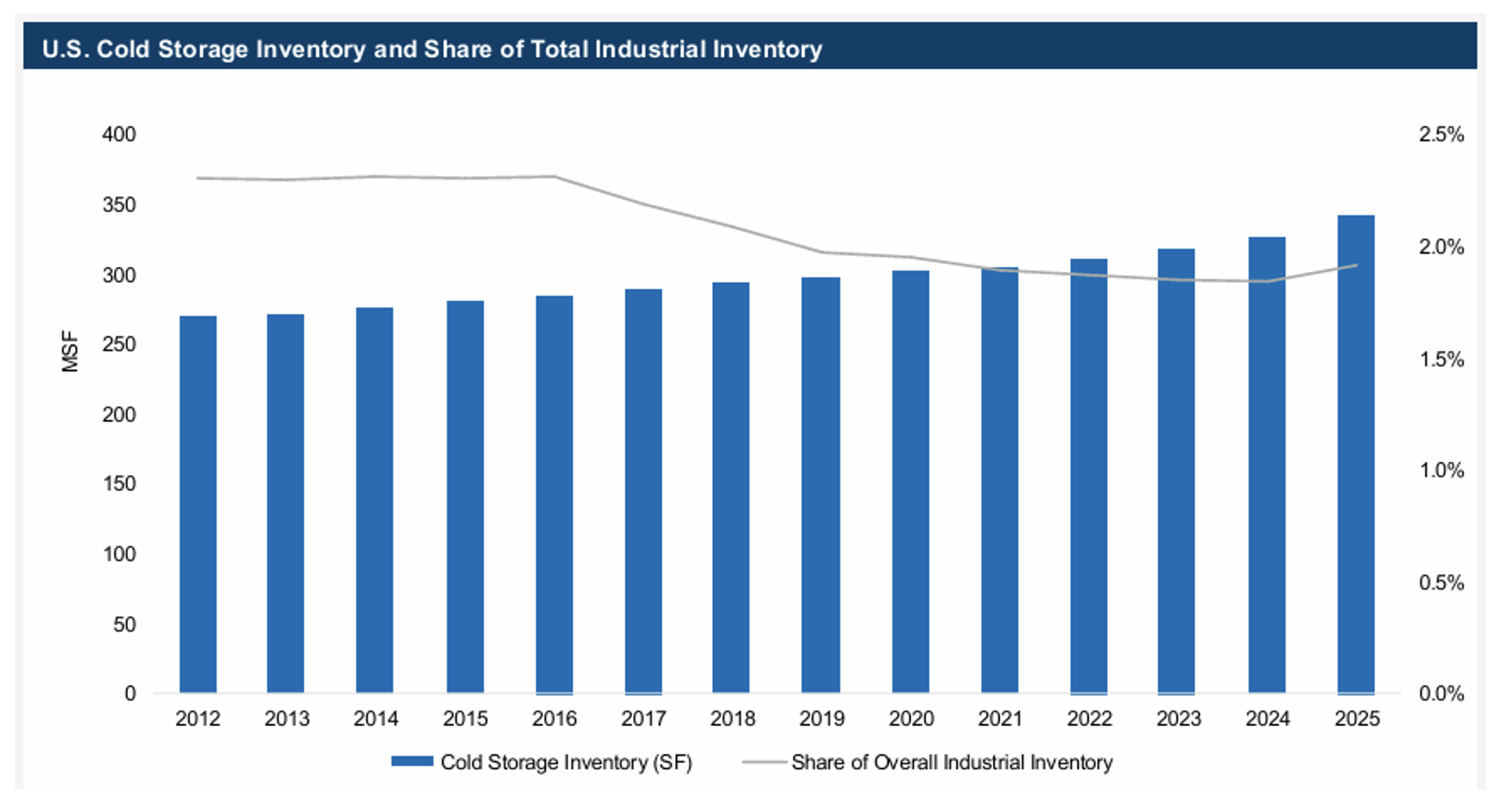

Commercial real estate (“CRE”) developers were already hard at work by then, putting up new facility after new cold-storage facility. By the end of 2025, national inventory had hit 342 million square feet.

Unfortunately for those efforts, as we know now, the predictions of pod living proved inaccurate.

It’s true that restaurants attract fewer customers today than they did in 2019, mind you. But only by 7%, according to Restaurant Business Magazine last year, not the 85%, 90%, or more the doom-and-gloom crowd expected.

And as people got out and about, the pandemic-fueled boom in cold-storage facilities waned.

Between that decreased demand and greater competition, temperature-controlled warehouses are now experiencing a 20-year high in vacancies. At 6.9%, that’s more than double pandemic-era levels.

Source: Newmark

It should come as no surprise then that LINE has fallen around 60% since its IPO. And rival Americold Realty Trust (COLD) has dropped around 60% as well during the same time frame.

The only question is whether those losses are justified… or if we’re witnessing yet another market overreaction worth taking advantage of.

Let’s have a closer look…

The Cold Storage Industry Is Suffering

The cold storage sector fell victim to a common enemy in commercial real estate – overbuilding.

It doesn’t matter how many times it happens to one CRE sector or another… nobody ever seems to learn an actual lesson. Instead, they get caught up in whatever the current craze is, ignoring history and making it repeat – or at least very closely rhyme – all over again.

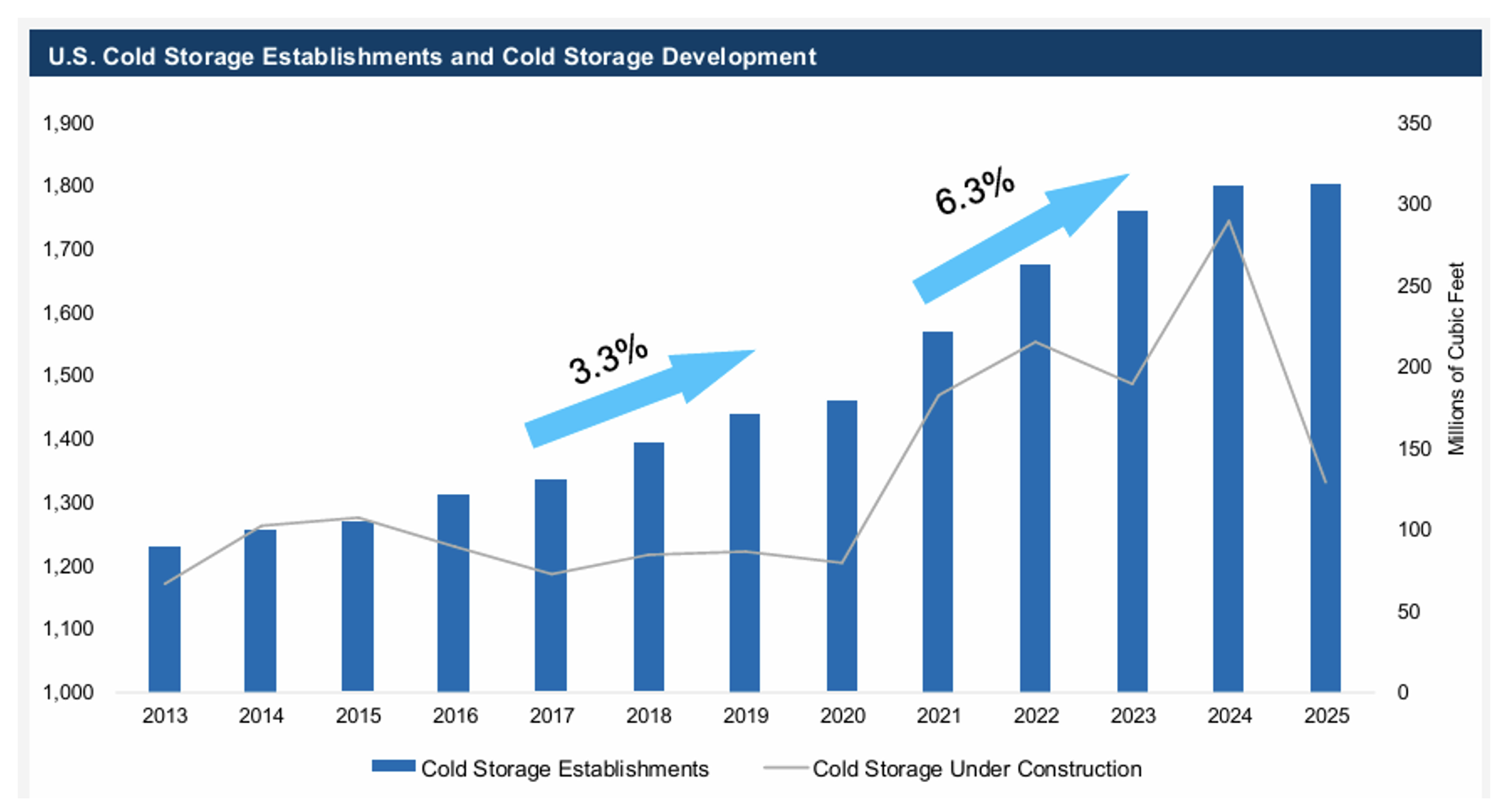

That’s precisely what happened between 2021 and 2023, when new cold-storage firms grew at a 6.3% pace. Compare that with the 2017-2019 period, where the compound annual growth rate (“CAGR”) was only 3.3%.

By 2025, however, they were facing the consequences of that greed. As demand waned, the number of cold-storage firms began contracting modestly.

This year’s pipeline is just 5.9 million square feet.

Source: Newmark

This isn’t to say the entire industry is doomed. It’s still very much necessary for both national and global food distribution.

It’s only that investors at every stage need to be much more particular about where they’re putting their money.

For instance, it’s important to recognize modernization. In today’s era of high tech and artificial intelligence, the newer facilities do stand a better chance of relevancy – and therefore profitability.

That’s a large part of why there is still a construction pipeline: to replace older locations that just can’t cut it anymore as electricity costs keep rising, labor costs remain tight, and automation demands keep mounting.

In short, this is not a passive landlord setup… It’s an operating business wrapped in real estate. And woe to the companies that try to capitalize on it without the proper understanding of what it takes.

Cold storage was always a difficult space to compete in. It comes with automatic barriers in the form of its required specialized infrastructure and high capital costs.

But it’s now proving to be an even more specialized field where only the strong can survive. That means the best of the best with the biggest powers of scale can benefit even more as weaker players fall behind and drop out altogether.

Earnings Should Rebound In the Midterm

Americold and Lineage, for their parts, do know what it takes. That’s why they’re the top players in cold storage with total cubic capacity of over 1.3 billion feet.

As already noted, that isn’t to say they’re not struggling. COLD reported a 1.2% year-over-year drop in fourth-quarter revenue, down to $658 million. And the larger LINE saw a 0.2% decline to $1.3 billion.

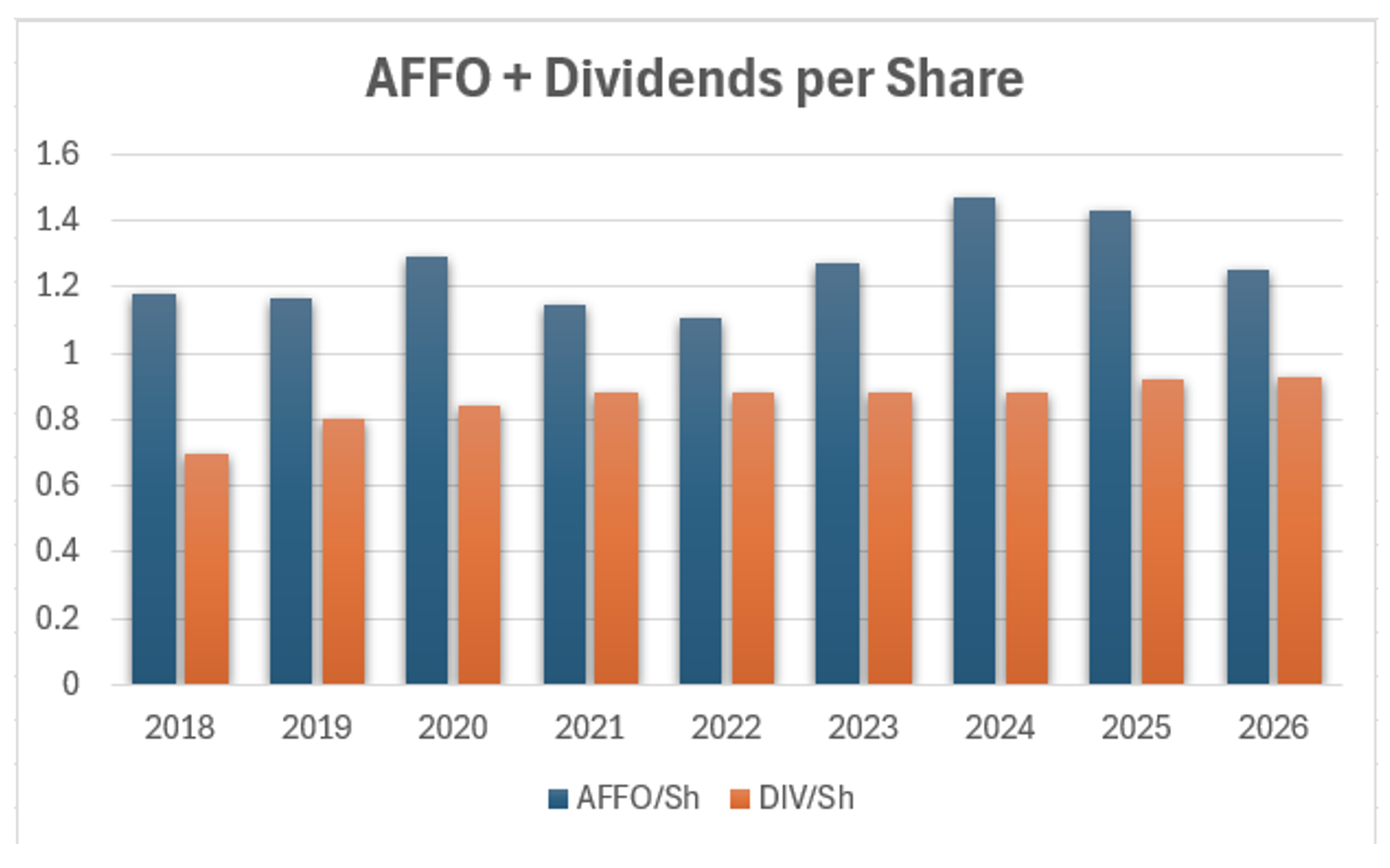

Moreover, COLD’s earnings – in the form of adjusted funds from operations (“AFFO”) per share – will likely decline by 13% in 2026. And LINE’s are equally unimpressive with a 14% decline.

However…

The former’s payout ratio is around 74%, signaling its dividend is safe. Plus, consensus AFFO per share estimates for 2027 are 3% and 9% for 2028.

Source: Wide Moat Research

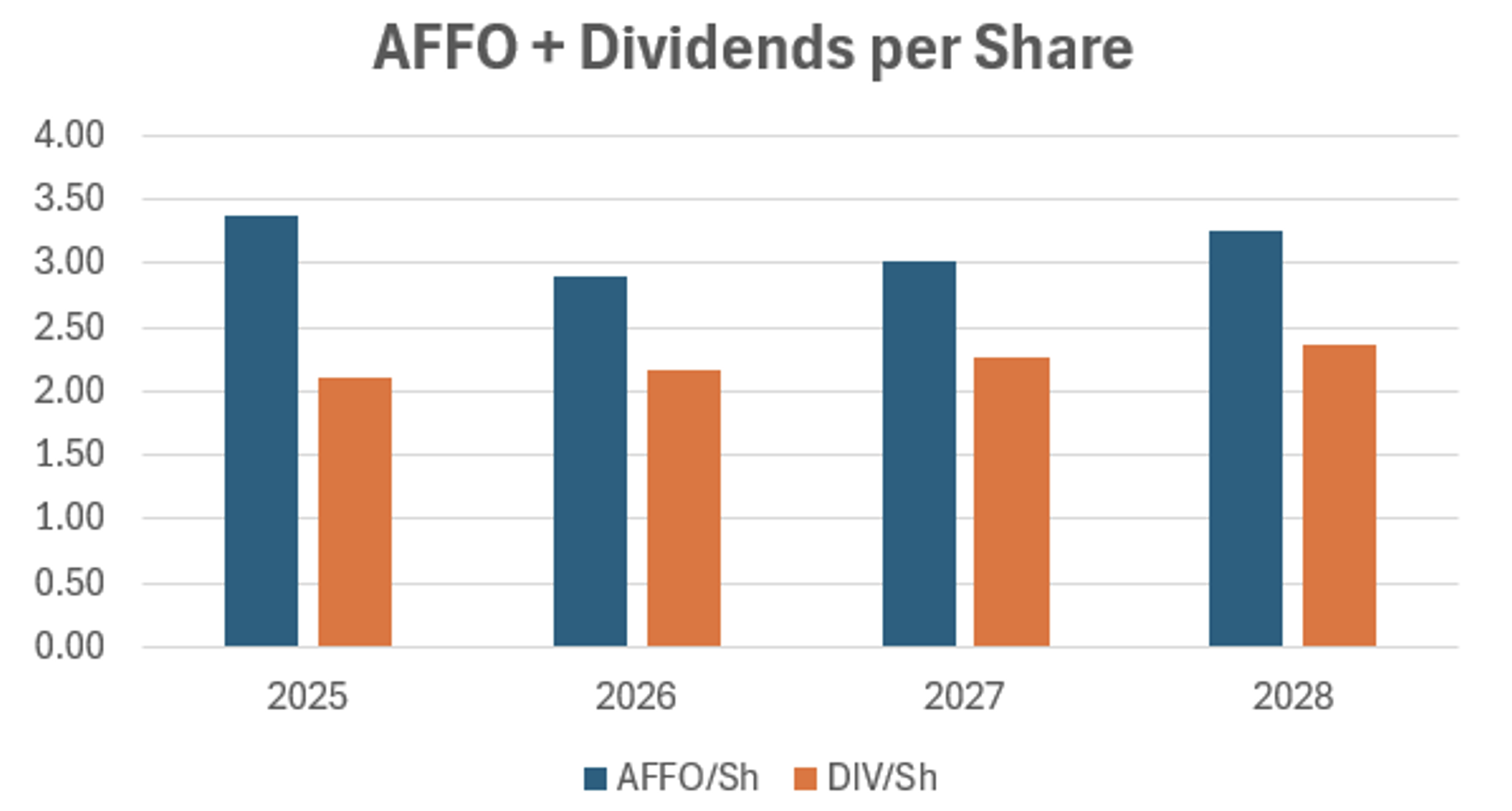

Meanwhile, LINE’s, which features the same payout ratio, should rebound by 5% in both 2027 and 2028.

Source: Wide Moat Research

Looking at those numbers, I just can’t see the justification in their current devaluations.

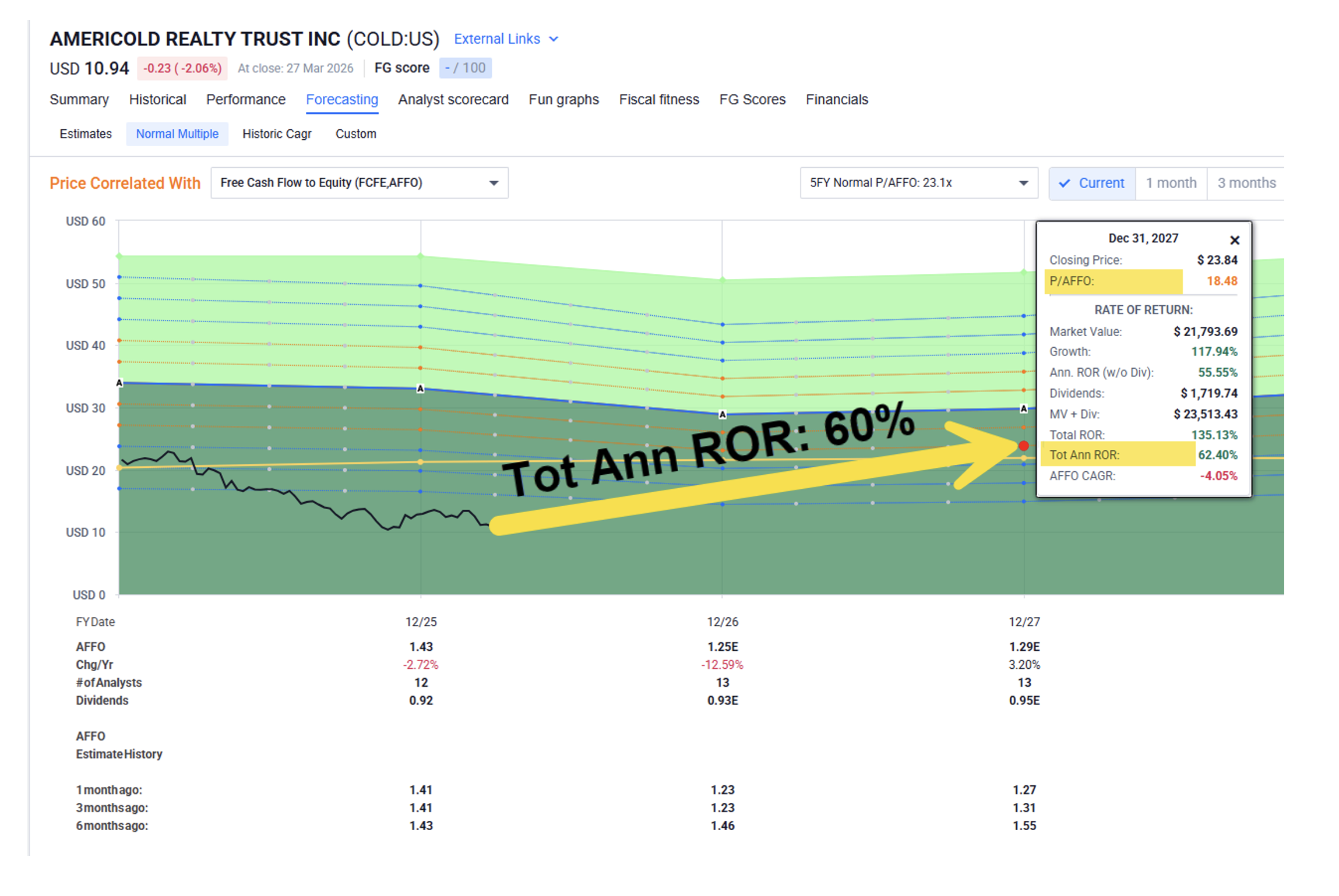

Right now, COLD shares are trading at $10.49 with a P/AFFO multiple of 7.9 times compared to their normal 23.8 times. That reflects a massive 67% discount – complete with an 8.4% dividend yield under a 74% payout ratio.

COLD might take some time to recover. Assuming mean reversion and modest growth in earnings, I could see returns of about 60%. And its dividend yield should keep paying while we wait.

Source: FAST Graphs

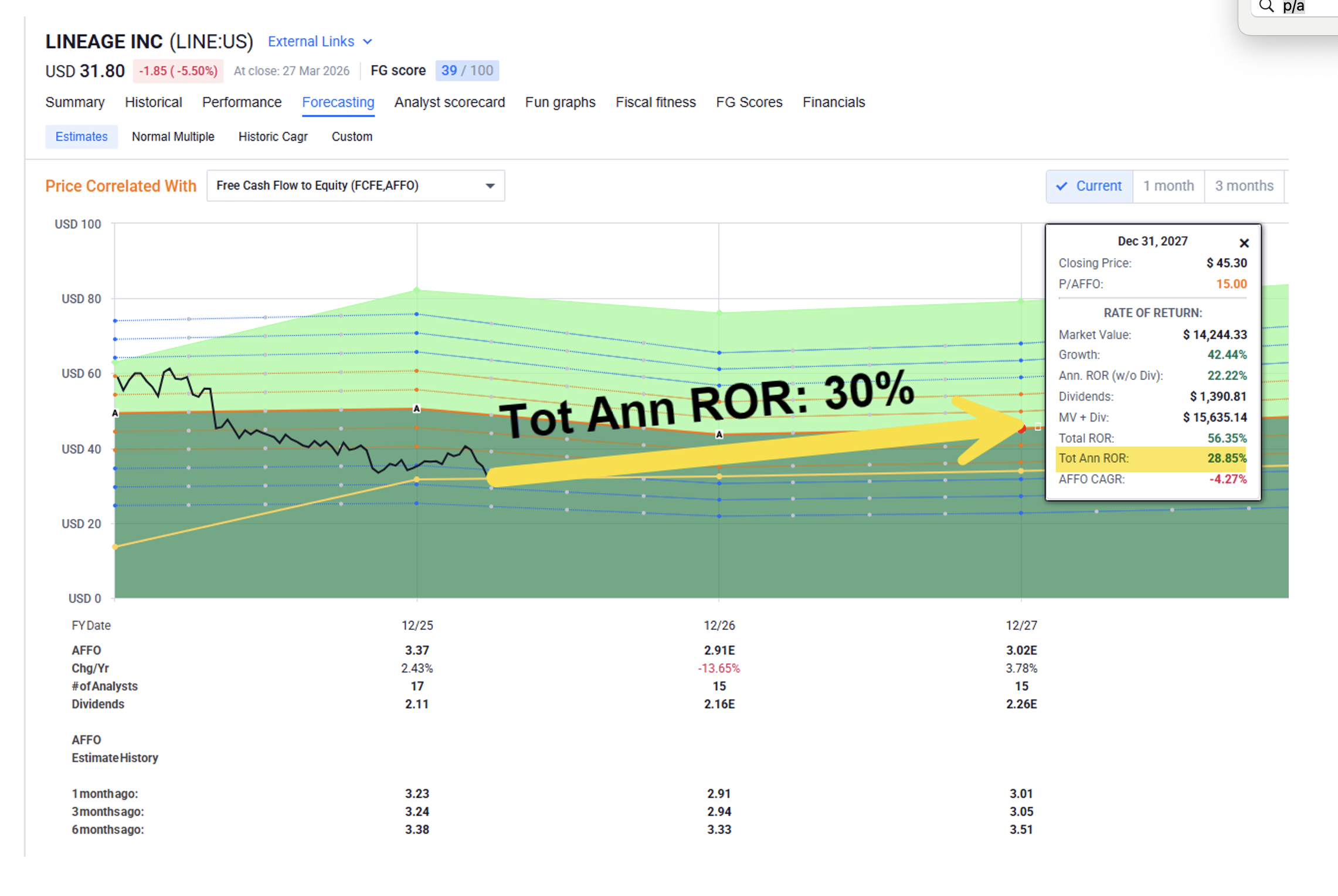

LINE shares, for their part, are trading at $31.80 with a price-to-AFFO (P/AFFO) multiple of 9.8 times – despite trading as high as 18 times after their IPO. Their current dividend yield is 6.7% with a 74% payout ratio.

As shown below, a return to 15 times would generate returns of around 30%.

Source: FAST Graphs

My Final Thoughts on the Cold-Storage Debate

Cold-storage REITs sit squarely at the intersection of logistics, food security, and temperature-controlled infrastructure. They own real, specialized, hard-to-come-by, hard-to-maintain assets that are critical to global existence as we know it.

Better yet, there are high costs for tenants to switch to competitors, making their operations extra sticky.

These barriers to entry should only grow stronger as e-commerce and grocery chains modernize supply networks even further over the coming years.

It’s rough going right now, I know, and investors are punishing even the most durable players. But cold-storage companies like Americold and Lineage that know how to survive both cooled-down and heated-up conditions?

I expect they’ll reward savvy shareholders who know a good thing before everyone else sees it.

Regards,

Brad Thomas

Editor, Wide Moat Daily

|